In line with the global decarbonisation agenda, hydrogen atoms are now in focus and ammonia, which carries three hydrogen atoms per compound, is poised to change the world once again – towards a carbon-neutral future. By Arthur Tay, Eiko Yamamoto and Jerald Foo, project finance, Singapore; and Andrew Bedford, sector coverage, energy transition technology lead and Tetsuo Kagaya, project finance, Tokyo, MUFG.

Ammonia has been dubbed one of the “four pillars of modern civilisation” alongside cement, steel and plastics1 as key technologies for the world we live in today. Ammonia has been critical in feeding our growing population of 8bn, which is projected to peak at 10.4bn. It enables the restoration of nitrogen to soil for bountiful harvests. Today, approximately 85% of ammonia synthesised globally is used as feedstock for fertiliser production2.

Excitement is mounting for a newfound purpose for ammonia as a hydrogen carrier. Historically, ammonia has been valued for its nitrogen content and its use as the precursor for fertiliser production. Ammonia compounds are composed of one nitrogen atom covalently bonded to three hydrogen atoms. The hydrogen atoms carried in ammonia are now in focus and ammonia is poised to change the world once again – towards a carbon-neutral future.

A hydrogen future

Following the Paris Agreement, which was established during the 2015 United Nations Climate Change Conference, COP21, signatory states have conceived forward-looking ambitions for implementing hydrogen economies to deliver the goal of limiting global warming to well below 2°C, and ideally no more than 1.5°C compared with average temperatures in the late 1800s. Limiting global warming to 1.5°C entails greenhouse gas emissions peaking before 2025 at the latest and declining by 43% by 20303. This requires a fundamental transformation of the global energy mix, 82% of which was accounted for by gas, coal and fossil fuels in 20224.

The four pillars of modern civilisation that have shaped our quality of life are all carbon-emitting. Ammonia is mainly produced from the cracking of methane, a component of natural gas. Cement production involves carbon-intensive chemical processes and high heat energy. Steel production is energy-intensive and requires coal to improve production quality. Plastics are produced predominately with oil and gas as feedstock. It is clear that technological changes are necessary for abating carbon emissions resulting from human activity.

With the potential to abate emission from the four sources above, hydrogen is an ideal energy solution to accomplish international climate ambitions. When comparing mass, hydrogen has nearly three times the energy content of gasoline5. It also burns clean, producing only water when combusted. These key properties are driving the adoption of hydrogen for emissions abatement worldwide.

Hydrogen, however, has customarily been produced through steam reforming, a process that utilises natural gas as feedstock and releases carbon dioxide. This is the most common and environmentally damaging method of producing hydrogen, and hydrogen derived from this process is known as grey hydrogen.

As opposed to grey hydrogen, green hydrogen is the goal for our carbon-neutral future. Green hydrogen is carbon-free as it is produced via electrolysis powered by renewable energy. Achieving zero emissions globally through hydrogen entails the use of green hydrogen exclusively. However, green hydrogen production costs two to four times that of grey hydrogen at current prices.

New uses of ammonia

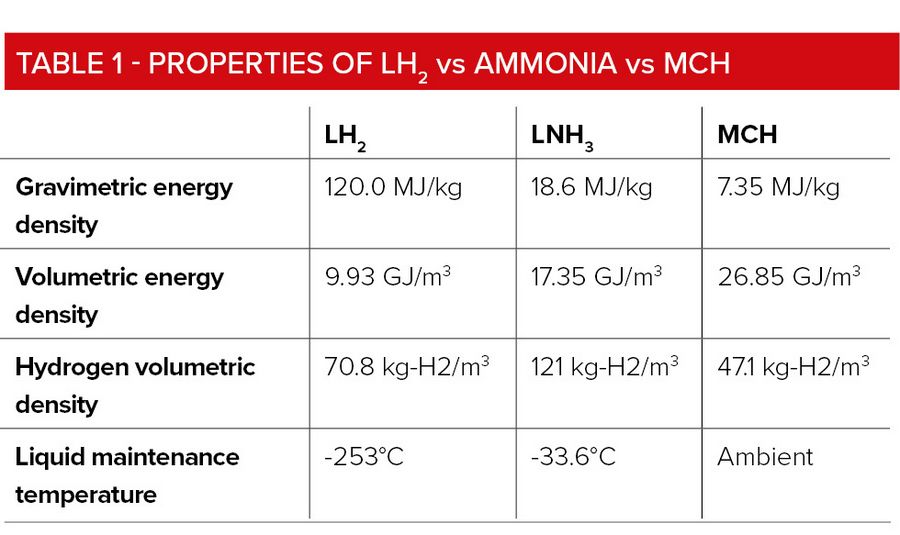

Developing the capacity to produce green hydrogen is only the first hurdle to global decarbonisation. The next challenge is in handling and using hydrogen, as it is gaseous at atmospheric conditions. Transportation solutions must be developed before hydrogen can fully displace fossil fuels. For example, Asia will require hydrogen imports as a net importer of energy that it is unable to source for sufficient supplies within its borders. Hydrogen may be transported in its liquefied form (LH2), in the form of liquefied ammonia (LNH3), or in the form of a liquid organic hydrogen carrier such as methylcyclohexane (MCH). Each form of hydrogen has its physical, safety and economic advantages and drawbacks, depending on key factors such as energy density, hydrogen volumetric density and liquid maintenance temperature.

Each form of hydrogen is also valued beyond its inherent properties. For example, LH2 offers minimal energy loss during liquefaction before transport and regasification after delivery, and MCH produces relatively pure hydrogen when dehydrogenated. As such, each form of hydrogen has slightly different target markets and applications.

Ammonia, the second most widely produced chemical on Earth, is favoured as a medium for hydrogen based on technological and commercial reasons. Ammonia has high hydrogen volumetric density, packing hydrogen approximately 70% more efficiently than LH2 and more than 2.5 times more efficiently than MCH. Maintaining ammonia in its liquid state at –33.6°C is also relatively simple and affordable compared with LH2 which must be transported and stored at –253°C. Additionally, ammonia production, typically through the Haber-Bosch process, is already industrialised with established technologies. However, the Haber-Bosch process is emissions-intensive, accounting for approximately 1.8% of global carbon dioxide emissions as of 2020. Capacity for producing green ammonia via carbon-free processes must be further developed to align ammonia use with the decarbonisation agenda.

Apart from transporting hydrogen, ammonia has direct applications in power generation and as an alternative fuel for ships. Directly combusting ammonia avoids energy losses from ammonia cracking, the process of liberating hydrogen from ammonia.

It is not feasible for coal-reliant Asia to phase out the fossil fuel industry immediately and adopt renewable energy without a gradual transition. Burgeoning demand from rapidly growing economies supported by younger fleets of coal-fired power require co-firing solutions as a means of energy transition. Japan is pioneering the technology required to co-fire ammonia with coal and has plans to retrofit its existing coal-fired power plants with said technology. The implementation of such technologies ensure that energy security is not jeopardised as emissions are being reduced.

JERA's Hekinan thermal power project in Japan will substitute coal with ammonia. It will be the world’s first large-scale commercial plant to combust 20% ammonia alongside 80% coal at its 1GW No 4 unit, starting in March 20246. Ammonia combustion is carbon-free and this reduces emissions by up to 20% insofar that green ammonia is used. Associated nitrogen oxides (NOx) emissions are also expected to be no higher than when coal is burnt and can be managed utilising existing exhaust scrubbers. In a bid to trigger the creation of a global ammonia supply chain, JERA has sent requests for proposal to more than 30 companies, seeking long-term ammonia supply contracts from April 2027 to the 2040s, to be used as a substitute fuel in its thermal power plants.

Referring to Table 1, ammonia is about 75% more energy-dense than LH2 in terms of volume. This makes its feasible for ammonia to be used as carbon neutral fuel for vessels. The combustion of ammonia is carbon-free given that ammonia has no carbon content. As of January 2023, orders have reportedly already been placed for 90 ammonia-ready vessels worldwide7 and ammonia looks set to be the backbone for decarbonising international shipping in the medium and long term.

Green ammonia outlook

Green ammonia has been gaining positive attention following the successful financial close of the NEOM green hydrogen project in Saudi Arabia by MUFG and a syndicate of banks. NEOM is the world’s largest green hydrogen plant with a first of its kind 1.25mtpa green ammonia production facility powered solely by renewable energy.

Looking ahead, IRENA projects that market growth for ammonia is likely to stem from the maritime sector and international trade of ammonia as a hydrogen carrier, representing new demand of 197m tonnes and 127m tonnes respectively by 20502. These new demand segments are sizable considering that global demand for ammonia stands at approximately 200m tonnes in 2022, of which only approximately 18m tonnes is traded on the open seas. Many more projects like the NEOM green hydrogen project are needed to meet the forecast demand for green ammonia.

Green ammonia is currently two to four times more costly than grey ammonia, which dominates ammonia supply today. Widespread adoption of green ammonia will require time and regulatory support. The shift from fossil fuels to hydrogen will require strong drivers to overcome the prohibitive costs of green hydrogen.

While it is expected that heightened production of green ammonia will aid in achieving economies of scale, green ammonia is still costly and its adoption cannot be expected to be driven by market forces alone. In Asia, Japan is leading support for the development of green hydrogen and ammonia supply chains. Japan is also open to blue hydrogen and ammonia production, which entails carbon emission but employs carbon capture if costs are more practical.

The Japanese government and its associated industries are working toward harmonised goals for the deployment of hydrogen and ammonia mono-firing and co-firing technologies. The government's Basic Strategy for Hydrogen includes plans to support the development of these technologies through a ¥2trn (US$13.4bn) Green Innovation Fund. A contract for difference will also be introduced for hydrogen and ammonia production, making upstream manufacturing projects more bankable and allowing expected users in the electric utility industry, steel industry and chemical industry, etc, to purchase hydrogen and ammonia at prices that are comparable to that of conventional fossil fuels. On the demand side, the government intends to regulate electricity retailers into supplying electricity that is ≥44% non-fossil generated by 2030, under the Advanced Electricity Utilities Act.

On the bigger picture, Japan has established a comprehensive plan to transform its economic and social system from being fossil fuel dependent to clean energy driven. Japan’s Green Transformation (GX) policy targets to bring about ¥150trn (US$1trn) of private-public investments in 10 years, and it envisages a two-pillar strategy for implementing low-carbon technologies while controlling costs.

Of the intended ¥150trn investment under GX, planned investments that are relevant to green ammonia include:

* Investment support for decarbonisation in the form of GX Economy Transition Bonds which will be first backed by ¥20trn (US$133bn) in issuance of sovereign bonds, then subsequently backed by financial resources generated from the introduction of a carbon pricing scheme;

* Renewable energy feed-in tariff and feed-in premium frameworks amounting to ¥2.0trn (US$13,333m) per annum for 10 years;

* Hydrogen and ammonia infrastructure development with ¥0.3trn (US$2,000m) per annum for 10 years

* Automobile infrastructure development, including hydrogen stations with ¥0.2trn (US$1,333m) per annum for 10 years

* The development of carbon neutral manufacturing processes, such as hydrogen reduction steelmaking, with ¥0.1trn (US$667m) per annum for 10 years

Within the two-pillar strategy, Pillar 1 comprises renewables, mainly solar and wind, which is to be expanded to make up 50%–60% of Japan’s energy mix by 2050. This will be accompanied by thermal energy paired with carbon capture and nuclear energy, which would make up 30%–40% of the energy mix. The remaining 10% will be accounted for by Pillar 2, which encompasses hydrogen-based and biogenic fuels, particularly hydrogen and ammonia.

Pillar 2 is necessary to support Japan’s energy demand growth given the country’s lack of fossil-fuel resources. Furthermore, replacing fossil fuels with hydrogen-based and biogenic fuels will serve to decarbonise backup power – enabling energy stability and maximising renewable deployment. This is especially relevant for Japan, an industrialised nation, as it greatly mitigates the critical issue of power shortages.

Japan’s Ammonia Strategy and Policy by the Ministry of Economy, Trade & Industry (METI) outlines that Japan’s demand for ammonia is expected to increase 10-fold from 3mt in 2030 to 30mt in 2050. It also states Japan’s intentions for ports and other ancillary facilities for ammonia transport to be developed, in line with the delivery needs of local companies.

Financing

In support of the global decarbonisation agenda, MUFG published the MUFG Transition Whitepaper 2022 (Whitepaper 1.0) in October 2022, which emphasised the importance of regional characteristics and interdependencies between energy and industry to push the transition forward. As a follow-up, MUFG published the MUFG Transition Whitepaper 2023 (Whitepaper 2.0) in September 2023, which takes the perspective of enhancing the transparency of Japan’s transition plan in the eyes of the global community, based on the international landscape and views received through dialogue with various stakeholders after the publication of Whitepaper 1.0.

Whitepaper 2.0 details MUFG’s philosophy to encourage and enable clients’ transition with our deep understanding of clients and their industries. This contributes to the creation of new markets for innovative technologies to accelerate further transition in the real economy. Japan’s seven positive technologies are also discussed, including hydrogen-based and biogenic fuels, which encompasses ammonia. The importance of mono-firing and co-firing ammonia is highlighted as Japan is not connected to an international grid and being able to import ammonia for power generation provides access to global renewable energy sources.

2022 was the sixth warmest year on record globally with global temperatures reaching ≥1°C above pre-industrial levels8. This is attributed to ever-rising greenhouse gas concentrations and accumulated heat. The need for climate action is apparent and investing in green ammonia is a key step in the right direction. Commercial production of green ammonia remains costly relative to grey ammonia and financing its value chain will prove challenging. There is a lack of large-scale willingness to pay significant premiums for green ammonia, standards associated with carbon intensity and certification, and a need for operational expenditure support in addition to upfront capital expenditure support to close the cost gap between grey and green ammonia.

Parallels can be drawn between hydrogen, green ammonia and liquefied natural gas (LNG) as emerging energy value chains. Just as in the case of adopting LNG in past decades, it is reasonable to expect green ammonia to become increasingly bankable as demand for it grows, relevant technologies advance, understanding of the industry improves, and favourable policies are implemented.

Financial institutions, especially banks, have the critical role of supporting the energy transition through the provision of financial solutions. MUFG’s philosophy to facilitate a whole-of-economy transition positions us to support companies with a genuine commitment and ability to deliver transition solutions, and this includes projects relevant to the blue and green ammonia value chain.

Footnotes:

1 - V Smil (2022, May). The Modern World Can’t Exist Without These Four Ingredients. They All Require Fossil Fuels. TIME. Retrieved on 9 November, 2023, from https://time.com/6175734/reliance-on-fossil-fuels/

2 - IRENA (2022, May). Innovation Outlook: Renewable Ammonia. 11, 25. Retrieved on 9 November, 2023, from https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2022/May/IRENA_Innovation_Outlook_Ammonia_2022.pdf?rev=50e91f792d3442279fca0d4ee24757ea

3 - United Nations (2022, November). Maintaining a clear intention to keep 1.5°C within reach. Retrieved on 22 November, 2023, from https://unfccc.int/maintaining-a-clear-intention-to-keep-15degc-within-reach

4 - H Edwardes-Evans and R Perkins (June 2023). Fossil fuels stubbornly dominating global energy despite surge in renewables: Energy Institute. S&P Global Commodity Insights. Retrieved on 22 November, 2023, from https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/oil/062623-fossil-fuels-stubbornly-dominating-global-energy-despite-surge-in-renewables-energy-institute

5 - US Department of Energy (nd). Hydrogen Storage. Retrieved on 22 November, 2023, from https://www.energy.gov/eere/fuelcells/hydrogen-storage

6 - T Kumagai (May 2022). Japan’s JERA to advance 20% ammonia co-firing at Hekinan by a year to FY 2023-24. S&P Global Commodity Insights. Retrieved on 22 November, 2023, from https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/energy-transition/053122-japans-jera-to-advance-20-ammonia-co-firing-at-hekinan-by-a-year-to-fy-2023-24

7 - L Hine (October 2023). Hydrogen at sea | World’s first ammonia-powered ships ordered by international liquid-fuels carrier. Hydrogeninsight. Retrieved on 22 November, 2023, from https://www.hydrogeninsight.com/transport/hydrogen-at-sea-worlds-first-ammonia-powered-ships-ordered-by-international-liquid-fuels-carrier/2-1-1536736

8 - United Nations (2023, January). 2022 confirmed as one of warmest years on record: WMO. Retrieved on 22 November, 2023, from https://news.un.org/en/story/2023/01/1132387

To see the digital version of this report, please click here.

To purchase printed copies or a PDF of this report, please email leonie.welss@lseg.com