The Japanese government, under the leadership of Prime Minister Fumio Kishida, has recognised the importance of battery energy storage system projects. By Joseph Kim, Yuko Ino and Jared Raleigh, with contributions from Stephanie Li, Motohiro Matsumura, Shuhei Mikiya and Sari Sakurai, Greenberg Traurig in Singapore and Tokyo.

Since the introduction of feed-in tariffs (FITs), Japan has experienced significant growth in the renewable energy market as it pursues its goal of achieving a mix including 36%–38% from renewable energy sources by 2030. A natural consequence of this growth is the challenge of maintaining grid stability and reliability, considering the intermittent nature of predominant solar and onshore wind that comprise most of Japan’s renewable energy sources. Battery energy storage system (BESS) projects offer a critical solution to the intermittency issue, enhancing grid stability and bolstering the resilience and reliability of the electricity supply system.

In August 2022, Prime Minister Fumio Kishida advocated for an acceleration of standalone BESS projects. In the same year, legislative amendments were enacted, enabling standalone BESS developers to apply for grid connections. More recently, in July 2023, the Agency for Natural Resources & Energy (ANRE) issued guidelines on the long-term decarbonisation power source auctions, with the first long-term auction to be held in the first quarter of 2024. These auctions, accessible to standalone BESS projects, offer long-term stable revenue opportunities, hence drawing significant interest from local and international developers, and the growth of this market seems imminent.

This article is designed to provide a general overview of the regulatory environment in Japan, a guide to the upcoming auction, and insights into the development and bankability considerations for BESS projects in Japan.

Evolving regulatory environment

The regulatory landscape for the BESS market is still in its early days, marked by ongoing reforms and evolving adjustments. This environment may create uncertainty for stakeholders, but legal and regulatory changes seem to be moving in a positive direction.

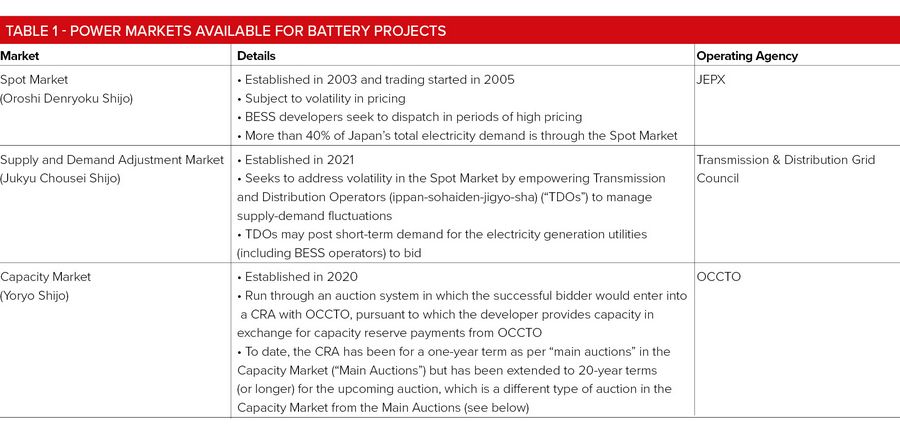

In May 2022, the Electricity Business Act (EBA) was amended to introduce regulations for the BESS market. Under the EBA, standalone BESS projects are classified as independent power generation facilities, eligible for grid connection permits. By connecting to the grid, these standalone BESS projects can generate revenues through energy sales in the market operated by Japan Electric Power Exchange (JEPX) or by entering into capacity reserve agreements (CRAs) with the Organization for Cross-regional Coordination of Transmission Operators (OCCTO).

Standalone BESS projects must also adhere to additional regulations typical of power generation facilities. For example, developers must notify the Ministry of Economy, Trade, and Industry (METI) about their construction plans, as the battery energy storage system is categorised as Electric Facilities for Business Use (jigyo-yo-denki-kousakubutsu), necessitating notification before commencing business operations.

Separately, standalone BESS projects are exempt from the requirements of the Environmental Assessment Act, unlike solar and wind projects, but local laws regarding environmental assessment may apply to standalone BESS projects.

Power market overview

This section offers a general summary of the power markets available to BESS project developers in Japan

Long-term decarbonisation power auctions

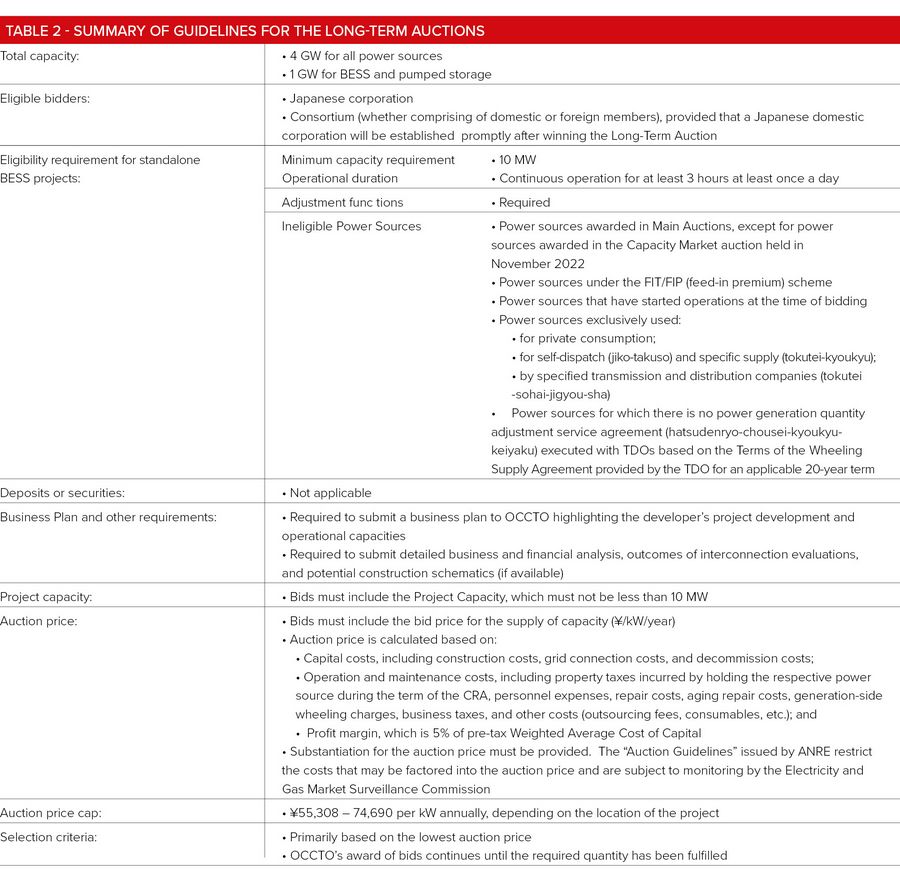

OCCTO announced the auctions for long-term decarbonisation power sources (long-term auctions) in July 2023, one of which covers standalone BESS projects. This is a significant market development as it eliminates merchant risks by offering a long-term contracted market for stakeholders, ensuring non-recourse financing for these projects, and promoting the sustained long-term growth of this sector.

The proposed framework for successful bidders includes entering into 20-year CRAs with OCCTO. Some of the key features are:

* A 20-year term, as a general rule, for CRAs;

* Fixed capacity reserve payments, calculated and paid monthly;

* The capacity reserve payment will be calculated by multiplying the auction price (JPY/kW/yr) by the contracted capacity (kW), with adjustments for Consumer Price Index, less certain penalty amounts under Article 18 (model general terms and conditions) of CRAs; and

* Successful bidders are obligated to pay OCCTO approximately 90% of its net total profit from other transactions during the CRA term. The net profit (shuueki) calculation encompasses (a) total revenues (shuunyu) from certain electricity sales and environmental attributes (from bilateral transactions or market participation) minus (b) associated power generation costs, ie fuel, waste disposal, consumables, Generation Side Tariff, and business tax.

* Current status of the first Long Term Auction –The process for the inaugural long-term auction commenced in October, with bidders having already submitted preliminary business and power source information to OCCTO. In December 2023, bidders will submit their expected project capacity (kitai-yoryo) information. In January 2024, bidders will submit (a) their auctioned capacity and auction price and (b) the expected capacity and other specifications for calculating the auctioned capacity to OCCTO, which will then review the respective bids and select and announce the winning bids approximately three months later.

Development risks for BESS projects

Given the infancy of Japan’s standalone BESS market, stakeholders should consider the following, non-exhaustive, list of risks: :

* Cost of critical materials – The cost of critical metals, such as nickel, cobalt, and lithium, significantly influences BESS project costs. Limited sourcing options of these critical metals and the potential geopolitical situation surrounding metal producing countries add to cost uncertainty.

·* Manufacturing – China’s dominance in the rare earth metal market and its production of more than 35% of BESS battery packs highlights a lack of supply chain diversification in battery production, leading to potential supply chain constraints in the coming years.

* Technology – BESS technology is rapidly evolving, exposing developers to technology obsolescence risk. This results in the investment horizon for developers needing to be appropriately considered.

* Licensing and approval process – The evolving regulatory framework in Japan creates some uncertainty regarding the permitting and approval process for standalone BESS projects. The applicable licensing may vary depending on factors such as site location, land status, construction requirements, construction plan, and investment structure.

* Interconnection – While the EBA permits standalone BESS projects connection to the grid, the interconnection costs are borne by the project company. Proximity of the project site and the costs associated with the permitting, design, and construction of the interconnection line remain a key concern.

* Land – Sourcing an appropriate project site for the BESS project is critical. Seeking a site located near the grid connection point (to minimise interconnection costs) and avoiding being near residential or public building areas are important factors. Additionally, it is important to determine if re-zoning – eg conversion of agricultural land (nochi-tenyo) – or forestry development permits are required, as these can increase costs and cause significant delays.

* Energy management system – A critical aspect of the BESS project is its ability to connect to the grid in accordance with the grid requirements. It is important to ensure that the EPC contractor will be warranting the performance of the energy management system with appropriate performance guarantees and potential damages in the event of a failure.

* Multi-contract vs wrap structure – Given the added complexity of BESS projects, it has been common for the construction phase to be covered by up to four separate contracts, covering i) BESS and battery management system, ii) the power conversion system and inverters; iii) the civil construction and electrical installation; and iv) the energy management system. While a full EPC wrap is preferred, if the multi-contract structure is adopted, it will be important to ensure that there are no gaps or overlaps in scope and that interface risks are appropriately addressed.

Project financing market

While the fundamental principles of project finance that apply to the financing of solar and wind projects also apply to BESS projects, a significant challenge for standalone BESS projects in attracting project finance has been their inability to generate long-term, consistent, and reliable cashflows. While lenders may have been willing to provide financing for merchant-based BESS projects, this would typically involve smaller debt sizing together with conservative cash sweep conditions. However, the long-term auctions have enhanced the bankability of standalone BESS projects by guaranteeing fixed revenues over a 20-year period.

The key bankability issues for lenders to provide financing for a BESS project will include the following:

* Security – Lenders, financing a winning standalone BESS project under the long term auction, will seek security over the project company’s right to receive capacity reserve payments from OCCTO. This usually involves a pledge or assignment of collateral rights (joto-tanpo), subject to OCCTO’s consent required under the terms of the CRA. Although OCCTO’s consent is possible, OCCTO will likely require the project company and the lenders to provide certain documents for it to consider granting such consent.

* Technology risks – Lenders’ technical advisers, when preparing the due diligence report, will usually examine the project’s ability to satisfy the commissioning test requirements and the minimum performance requirements under the offtake agreements. For a BESS using lithium-ion batteries, lenders will expect a robust review from the technical adviser on capacity degradation and safety issues tied to overheating. For a BESS using newer technologies, such as hydrogen and compressed air, lenders generally view all these newer technologies as having increased risks due to a lack of historical data.

Project companies can mitigate degradation issues by securing a performance guarantee and/or equipment warranties to ensure that equipment will be replaced or otherwise maintained at a minimum capacity. Some technology risks will then be shifted from the project companies to the technology suppliers, and the project companies can then provide assurances to the lenders that the applicable equipment will perform at the levels set forth in the lenders’ financial model.

Lenders will assess the value of performance guarantees and equipment warranties based on a couple factors, such as the creditworthiness of the performance guarantee/equipment warranty providers. The equipment providers and service providers in the BESS market might be new entrants, and therefore, may not have strong financial credentials. This risk may be mitigated by providers offering letters of credit and/or parent company guarantees.

* Construction risks – Lenders typically prefer fixed-price turnkey engineering, procurement, and construction (EPC) contracts rather than a split EPC structure because a turnkey EPC contract will shift more construction risks from the project company to the single EPC contractor. However, it is common for BESS projects to utilise multi-contract schemes for the EPC procurement as mentioned above. This means that lenders will generally conduct more diligence to address additional risk exposure. For example, given the volatility in the battery markets in recent years in terms of supply and cost, which is expected to continue in the near future, lenders will usually undertake additional diligence of a BESS project to ensure that there are sufficient reserves for potential cost increases and an adequate timeline to address delays.

* Operating risks – Lenders will conduct diligence to understand the BESS project’s operating limitations and operations and maintenance (O&M) costs. An O&M agreement with an experienced operator will be helpful in giving lenders confidence that the project will be operated based on good operating practices that are the norm for this type of project. To the extent that there are project degradation issues or other expected major maintenance costs such as costs for augmentation of battery systems, lenders may require the project company to establish O&M reserves to ensure that there will be sufficient funds to cover the significant future O&M costs.

Lenders will also require the project company to confirm that they have sufficient rights to the system’s software and any other intellectual property rights critical to the BESS operations. The project company needs to ensure that it and lenders (under an enforcement event) can still access the system’s software when the original operator is replaced.

As an alternative to non-recourse financing, project companies might consider hybrid financing models, as this approach reduces dependency on any single project’s performance and cashflow.

Final thoughts

While Japan is only in the early stages of developing its standalone BESS market, it appears to be on the right track for achieving the investment and growth that it desires. For developers coming in at this early stage, it presents a tremendous opportunity, but one that requires a diligent approach in order to maximise the potential benefits.

To see the digital version of this report, please click here.

To purchase printed copies or a PDF of this report, please email leonie.welss@lseg.com