The share of total CO2 emissions from the electricity and heat sector is currently around 50% of the EU-ETS emissions. Extensive efforts have been made over the years to reduce this share and thus reduce carbon intensity – CO2 emissions per produced kWh – in the power sector. By Ole Tom Djupskaas, market expert Nordic power, Gabriele Martinelli, head of European power, and Nathalie Gerl, lead analyst for European power markets, LSEG Power Research.

The latest efforts include the FitFor55 package and the RePowerEU initiatives, both adopted by the EU Council in 2023, aiming to reach the target of 55% lower greenhouse gas emissions in 2030 than in 1990. Both wind and solar capacities will increase; however, with a particular emphasis on solar where the aim is to increase installed capacity to 600GW in 2030. To achieve the aim of a 55% reduction in greenhouse gases by 2030, the FitFor55 working papers show that the carbon intensity of power needs to be reduced from 250 grams of carbon dioxide equivalents per kilowatt-hour in 2022 to around 115 grams in 2030.

Electricity numbers for 2023

First, the installed capacity of wind and solar in EU countries has increased rapidly the last year. Installed wind capacity was about 217GW on November 1, up from 200GW a year earlier, and is expected to reach 370GW in 2030. Similarly, solar capacity was at 215GW on November 1, up from 180GW twelve months earlier, and expected to reach 493GW in 2030. Future capacity figures are from internal research at LSEG Data & Analytics, based on official targets from individual countries.

If we first look at Germany, we see higher renewable output in 2023 than in the previous year. Wind and solar output is expected to reach 191TWh, up from 181TWh in 2022. This accounts for a 41% share of demand, up from 37.3% in 2022. If we also include other renewable sources, such as hydro, biomass and waste, the renewable share rises to 55%.

Despite there being no nuclear production from May this year in Germany due to decommissioning of the last remaining plants, thermal electricity production from fossil energy sources such as coal, gas and lignite has decreased from 219TWh in 2022 to 171TWh in 2023. In addition to higher wind and solar output, higher imports and demand destruction are important reasons for the decline.

We have seen demand destruction in countries such as Germany and France lingering at about 7% of total demand this year. This is a consequence of the energy crisis in 2022, when high energy prices forced industries to reduce their production and households to be more careful with their electricity use. Despite lower energy prices this year, they have not been low enough to trigger increased electricity consumption in the manufacturing industries.

In Germany, we expect power demand for 2023 of about 460TWh, substantially lower than 483TWh in 2022, a year when parts of Q3 and Q4 were already heavily affected by demand destruction. This means that demand destruction persisted during all of 2023, despite gas prices returning to lower levels. This is particularly relevant in Germany, since a large portion of demand destruction seems to happen in industrial sectors especially sensitive to electricity prices. In France, demand for 2023 is expected of 425TWh, again lower than 443TWh of 2022, and substantially lower than 466TWh in 2021. However, 2021 was considerably colder than 2023. In France, the demand destruction component also plays a major role, and weather variability explains just a minor portion of the significant demand decrease observed in the last two years.

While gas was outcompeted by coal for electricity production in 2022 due to record high gas prices, we saw lower gas prices in 2023, leading to coal-to-gas switching. Thermal electricity generation using coal or lignite as fuels dropped almost 30% year-on-year in Germany. This was particularly true in the summer of 2023 (Q2 and Q3), where coal and lignite generation amounted to just above 45TWh across six months. By comparison, in the same period in 2022, coal and lignite contributed to 79TWh of power.

In April, falling gas prices caused a lower marginal cost for electricity produced in thermal power plants using gas as fuel than in those using coal. The marginal cost for a gas-fired power plants with 50% efficiency fell to €82/MWh in the financial market on June 1 for the July period, €20/MWh lower than coal. This is one important reason for the low coal and lignite generation in Q2 and Q3. In Q4, like in the first two months of the year, we saw gas becoming more expensive than coal, resulting in increased coal burn.

The lower electricity production from fossil fuels was accounted for by lower demand, higher renewables, and higher imports from neighbouring countries, especially France, which experienced a substantially improved hydro and nuclear situation. Across the entire year, imports to Germany rose by 44.3TWh.

In France, the opposite happened, as exports increased by 66.7TWh across the entire year. This was made possible by substantially higher nuclear generation, which is expected to increase by 42TWh, from 278TWh in 2022 to 320TWh in 2023. This is even on the high side of the 300TWh–330TWh forecast that French utility EDF estimated at the beginning of 2023.

At the same time, hydro generation increased by 8.5TWh, and wind and solar increased by a further 13.5TWh, bringing a total of more than 60TWh of additional clean energy to the French power balance with respect to the year before. This made possible a further decarbonisation of the French power sector – minus 1.8TWh of coal generation, and minus 13.2TWh of gas-fired generation – and a wider decarbonisation of the European power sector through the exchanges mentioned above.

In Southern Europe, we observed similar trends, with increased hydro and renewable generation both in Italy and in Spain. Hydro generation increased by 10TWh in Italy and 7TWh in Spain, year-on-year, and wind and solar increased by 7TWh in Italy and 12TWh in Spain. This made possible a substantial replacement of gas-fired generation in both countries, with 15.5TWh and 22TWh of lower gas-fired generation in Italy and Spain, respectively. Spanish solar generation made a particularly impressive leap forward of 8.7TWh, from 27TWh in 2022 to 35.7TWh in 2023, increasing by more than 30% year-on-year.

Europe as a whole

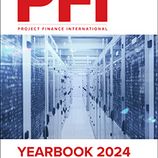

On the European level, we see much the same stories, on a larger scale. Electricity production from coal and lignite is expected to drop by an impressive 24% from 381TWh in 2022 to 288TWh in 2023, while gas-fired generation is falling by 19% from 499TWh to 405TWh. The reduction in thermal generation by fossil fuels is offset by lower demand and increased renewable production: Demand declined by 73TWh due to increased demand destruction, while wind and solar production gained 62TWh and hydro improved by 50TWh.

Hydro production was low in 2022 due to drought both on the Continent and in the Nordics. The hydro situation, including snow, soil water and water reservoirs, bottomed out at 60TWh below normal in May 2022 and averaged 40TWh below normal for the year. In 2023, the hydro situation saw a slight improvement until July, before a significant rise took place in the second half of the year, averaging 22TWh below normal for the year.

The reduced nuclear output in Germany and Belgium is almost entirely outweighed by higher production in France and stays constant at 585TWh. Never before in Europe has fossil generation – coal, lignite and gas – settled below 700TWh across an entire year. In 2020, when demand figures were rather similar to 2023 because of the Covid 19 pandemic, fossil generation in Europe settled at just below 800TWh.

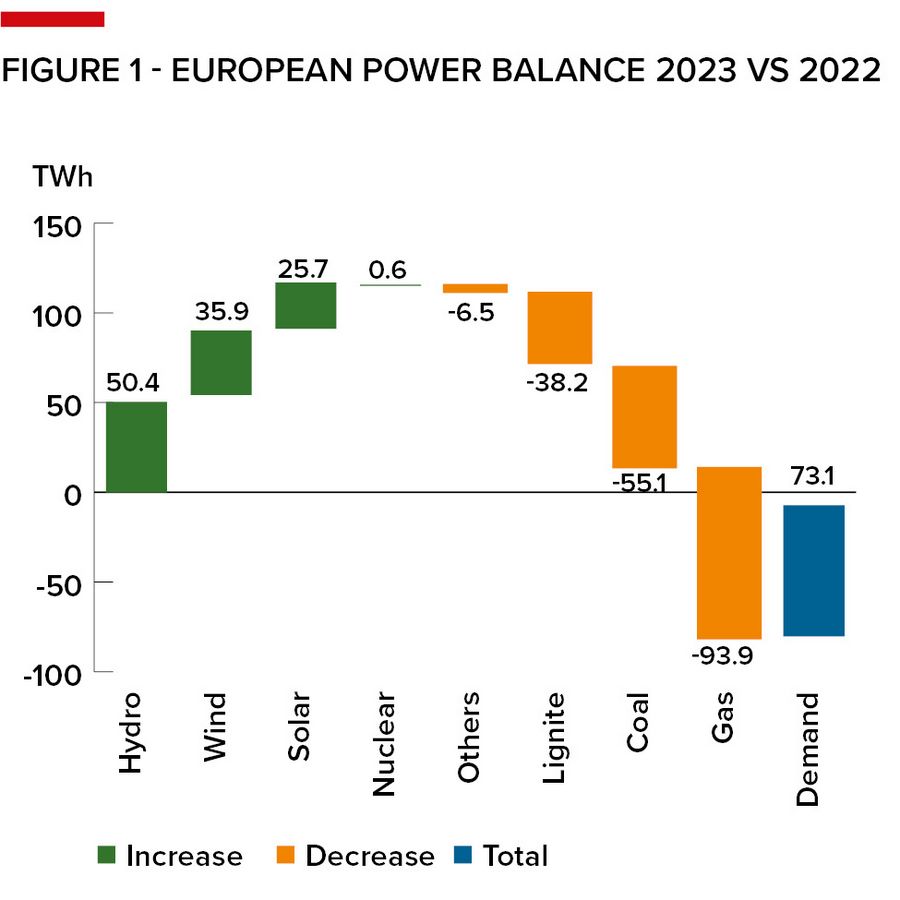

The share of renewable energy sources in the European electricity generation mix was 45% in 2022. In 2023, our preliminary figures indicate an increase to 50%. In 2024 and 2025, based on results from our mid-term price model for Europe, we expect a further rise to 52% and 53%, respectively. The decrease in the power sector’s emissions is substantial from 2022 to 2023: We approximate a 22% year-on-year drop for Europe. Despite growing power consumption and further nuclear decommissioning in the future, we expect power sector emissions to continue declining, though not at this year’s pace. By 2035 we expect power emissions in Europe to have dropped by more than 80% compared with 2005.

To see the digital version of this report, please click here.

To purchase printed copies or a PDF of this report, please email leonie.welss@lseg.com