In January 2023, the financing for the 99MW Jeonnam offshore wind project closed in South Korea. With its multi-EPC contracting set up, its full non-recourse status, its bespoke structure to meet South Korean specificities and its good mix of international and local financial institutions, the Jeonnam project financing sets a solid template for future offshore wind projects in the country. By Raphaël Chabrolle, Derrick Tan and Eana Kim, Sumitomo Mitsui Banking Corporation.

The Jeonnam project financing represents a landmark path-finding transaction in the Asia-Pacific offshore wind sector, as offshore wind continues its rapid expansion outside of Taiwan, in one of the most promising Asian markets. It is the first international project financing for offshore wind in South Korea. It confirms the first signs of South Korea as the next place to be for large-scale offshore wind in the region, driven by a favourable legal and regulatory framework, including a new auction regime with 20-year renewable energy certificate (REC) offtake contracts, an experienced local supply chain ready to be scaled up, abundant wind resources and other factors that have created the conditions to combine the strengths of experienced international and local developers, contractors and financiers.

With nine financial institutions involved, including seven international banks and two local financing institutions, the project is evidence of the strong interest from international banks in South Korea offshore wind projects. It also shows the willingness of South Korean financial institutions to bank complex offshore wind projects on a full non-recourse basis. For most of the participating financial institutions, this was their first experience in South Korea non-recourse financing. As might be expected, a range of innovative structures and approaches were used, given the specificities of the South Korean offshore wind market, which are likely to set the benchmark for future financings in the country.

Despite being the first non-recourse offshore wind project to be financed on a full non-recourse multi-EPC basis, deviating from the typical South Korean project finance approach for renewables projects, Jeonnam reached financial close in record time, following the successful auction award announced in late 2022. This article provides a brief overview of how this remarkable success was achieved, starting from a presentation of the key project features, and then discussing some of the key challenges and structuring solutions that were developed for this tailor-made project financing.

Project sponsors

Following Taiwan, the Asian frontrunner in developing an ambitious offshore wind plan, the South Korean government has laid down a comprehensive strategy to attract many international and local developers and to leverage on the strong South Korean industrial base and know-how.

The South Korean government aims to increase the share of renewables in the energy mix from 7% currently to 26% by 2034, with offshore wind targeted to contribute 12GW by 2030. To do so, among other regulatory measures, the government has imposed mandatory obligations on large-scale power generators to source a minimum percentage of their generation through renewable energy certificates. This minimum percentage has been raised from 10% to 25% by 2026, demonstrating strong support for the national renewables agenda. In addition, Shinan County (South Jeolla Province), where the Jeonnam project is located, is one of the six regions identified by the government for the promotion of offshore wind.

These solid regulatory foundations set the scene for SK E&S Company Ltd (SK E&S) with 51% and CI III, a fund managed by Copenhagen Infrastructure Partners (CIP) with 49% to proceed with their 99MW Jeonnam project, located 10km off the shores and with a water depth of 10m– 20m. SK E&S is a leading energy company headquartered in Seoul, South Korea and is active in 37 overseas market such as the US, Australia, and Indonesia. It was founded in 1999 as a holding company for the city gas business and has since expanded into a complete LNG value chain player.

From the late 2010s, SK E&S started to expand its business portfolio to include renewable energy businesses to lead the paradigm shift towards low-carbon, eco-friendly energy. SK E&S is 90% owned by SK Group, a South Korean conglomerate with businesses in telecommunications, chemicals, energy, and construction. SK E&S is a key player in the South Korean renewables market. As of September 2022, the company had successfully brought to operation 293MW of solar and onshore wind energy in South Korea. SK E&S is now developing, constructing and operating 3.8GW of renewable energy projects in both the domestic market and overseas, and plans to expand its renewable energy projects to 7GW by 2025.

CIP is a fund management company founded by senior members of the energy industry in 2012. The senior partners have worked closely together as a team for more than 15 years. CIP’s current investments include a wide range of renewable energy infrastructure assets including offshore wind, onshore wind, offshore power transmission, biomass, waste to energy and solar PV investments.

CIP employs more than 400 dedicated professionals with practical commercial, industrial and project execution experience in the energy sector, able to draw on experience gained from more than 50 large-scale energy infrastructure projects. It has €25bn funds under management across 11 funds. Investors include more than 100 institutional investors, including pension funds, insurance companies, family offices, and asset/fund managers. CIP has successfully brought 2.8GW of offshore wind projects to final investment decision (FID) in the UK, Germany, the US, Taiwan and South Korea. It has a development pipeline of 50GW offshore wind projects globally at various stages of development, comprising both fixed-bottom and floating foundation sites.

Project snapshot

For their debt financing strategy, the project sponsors took into account the tight timeline – completion date targeted in December 2024 – and the relative immaturity of non-recourse financing in South Korea to build up a complementary lending group of international and local financial institutions.

A group of seven international banks and two local financial institutions, the vast majority of them with offshore wind experience, was mandated late 2022. Sumitomo Mitsui Banking Corporation (SMBC) was one of the mandated lead arrangers, deal contingent hedge provider (IRS & FX), hedging bank and documentation bank. The Jeonnam financing drew heavily on recent European and Taiwan offshore wind financing precedent terms, but it was updated to reflect the South Korean environment and the specifics of the project. Debt sizing criteria and absence of export credit agency (ECA) cover were actually closer to recent European offshore wind projects, from a debt to equity, debt service coverage ratio (DSCR) and loan tenor perspective, despite the early development stage of the South Korean offshore wind sector.

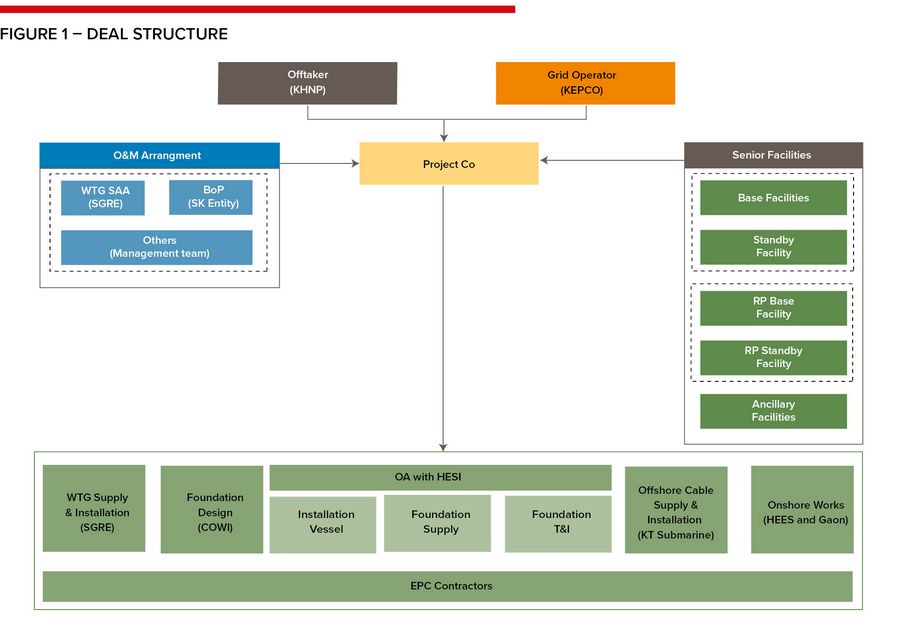

These favourable financing terms reflected the experienced sponsor group, the sound construction and operations and maintenance (O&M) strategy, and the relatively modest project debt size (Won615bn or ~US$470m equivalent) at a time when competition among the international banks was high. International commercial banks were keen to start their offshore wind journey in South Korea, which they’ve identified as a country both with a large project pipeline and an opportunity to diversify their exposure beyond Taiwan. In parallel with the discussions with the commercial banks during the last quarter of 2022, the sponsors had been busy finalising their procurement strategy. The project adopted a multi-contract construction strategy with five key construction packages, as follows:

* Turbine supply and installation with Siemens Gamesa Renewable Energy (SGRE) for DD-200 9.9MW WTGs.

* Foundation design with COWI Korea Co Ltd

* Foundations supply, transportation and installation (inclusive of installation vessel) with Hyundai Engineering and Steel Industries (HESI) under an overarching agreement (OA)

* Offshore cable supply and installation with KT Submarine Co Ltd and

* Onshore works with Hyundai Electric Systems Co Ltd and Gaon Cable Co Ltd.

Lenders got comfortable with this multi-contractor foundation approach thanks to the overarching responsibility of HESI in key foundation packages, robust budgeted cost contingencies, appropriate buffers in the construction schedule and the successful experience of CIP in managing a multi-contractor strategy for the construction of 14GW of operational offshore wind capacity worldwide. As for the operations, the project will benefit from a 15-year service and availability agreement with SGRE, together with a 15-year O&M management agreement with one of the subsidiaries of SK E&S.

On the revenue side, the project will sell (i) electricity into the wholesale Korean Power Exchange (KPX) and (ii) RECs generated via a 20-year fixed price (non-indexed) REC offtake contract. The fixed price mechanism of the REC offtake contract is intended to eliminate the merchant revenue risk from the KPX. To secure the REC offtake contract, the project company has participated in the first offshore wind auction process, the results of which were released in October 2022. Upon auction award, the borrower allocated its full generation capacity to Korea Hydro & Nuclear Power (S&P: AA, Fitch: AA- and locally rated AAA), one of the six subsidiaries of KEPCO.

Challenges and innovations

* South Korean won with international PF structure – With a South Korean won revenue structure and a robust local financing market, financings are largely raised in similar local currency across offshore wind projects. Jeonnam embarked with a similar strategy gathering won liquidity, while also bringing an international flavour to the PF structure – structural considerations, documentation and security structures were based on international precedents. The engagement process with international and local financing institutions started in 2021 with support from key international lenders. This has proven to be pivotal following the credit squeeze in the local debt capital markets triggered by the Legoland default1 in the later part of 2022, shortly before financial close.

* Heightened focus on project delivery – Construction challenges across the portfolio of Taiwanese offshore financings that resulted in delays and cost overruns have exposed several constraints (lack of vessel availability, geotechnical aspects, supply chain constraints) among Asia-Pacific offshore wind projects. With Jeonnam deploying similar monopile foundation structures as some of the earlier Taiwanese projects, it went through an enhanced bank due diligence process into key areas such as geotechnical considerations including an innovative installation method for several of the monopile structures, a newly built vessel, experience of key contractors, possible radar interference, and wake losses, among others.

A key source of comfort for lenders was that CIP brings with it procurement and interface management experience gathered both from European precedents and importantly the Asia-Pacific experience from Taiwan, while SK E&S could leverage on its close relationships with reputable South Korean contractors.

* Resident participation (RP) programme – Introduced under the RE Act, this provides additional REC allocations (which has to be transferred to the local residents through a compensation agreement) in return for specified local participation in the RE generation projects. Although this feature remains as an optional item, Jeonnam secured the requisite funding and put in place a financing structure that is suitably adapted to ensure the RP programme can be implemented around the project’s commercial operation date. This is to be done through RP facilities where the proceeds are extended to local residents to subscribe to a bond issuance by the project company.

* KEPCO’s grid capacity and the 10th Grid Reinforcement Plan – With KEPCO being the transmission and distribution authority, it is responsible for upgrading the local grid capacity to support generation from the project prior to completion. As per local T&D regulations and terms under the grid connection agreement, the project is exposed to curtailment risks due to technical faults. Therefore, lenders had conducted detailed due diligence on the overall progress of KEPCO’s grid reinforcement plan to ensure there are robust contingencies available in the event of delays due to grid availability. KEPCO’s recent financial weakness remains a cause of concern but some comfort was taken based on its track record and government backing.

* Interest rate and FX risks – The impact from the credit crunch also subjected the project to volatility in the interest rate markets, where short-term yields spiked to historical highs in the midst of the financing process. Despite having a proportion of fixed-rate tranches as part of the funding mix, the project was still exposed to interest rate movements as rates are only fixed closer to the timing of the first drawdown. As such, the project entered into a deal contingent hedge arranged by SMBC to mitigate the movements in interest rates prior to financial close. This was the first deal contingent hedge for interest rate swaps arranged in the South Korean market. Similarly, a deal contingent hedge was executed to manage the project’s FX exposure on foreign currency denominated capex.

To promote competition, the government decided not to disclose the ceiling price in 2023. This is the second year that the government has announced an auction for wind projects, which shows that it is trying to control the renewable energy market through auction, inducing a decrease of electricity tariffs. The result of the auction is expected to be announced in December 2023.

Taking into account the favourable regulatory context, and despite its relatively small project size compared with the average 500MW+ size of offshore wind projects, we believe the Jeonnam project is a solid template for the South Korean offshore wind pipeline, for both fixed bottom and floating wind projects. SMBC is proud to be involved in the First International Project Financing for Offshore Wind in South Korea and remains committed to support the renewable energy ambitions of South Korea.

Next steps

In line with the South Korean government’s 10th Basic Energy Plan, the Korea Energy Agency (Renewable energy centre) announced in October 2023 the second auction for wind projects, offering 400MW for onshore and 1,500MW for offshore projects – a pre-requisite being that projects must have obtained an Electrical Business License and Environmental Impact Assessment approvals. This marks a significant increase from 2022 when 374MW of capacity (including both onshore and offshore) was awarded and is in line with the 2030 target of 19.3GW of wind capacity (including 14.3GW offshore wind).

Footnote

1 - How a liquidity crunch in South Korea began at Legoland (ft.com) (https://www.ft.com/content/ba91bee9-b0d1-47cd-9821-81185cacd195)

To see the digital version of this report, please click here.

To purchase printed copies or a PDF of this report, please email leonie.welss@lseg.com