In 2023, Germany's solar sector witnessed a surge in mezzanine financing, including transactions involving independent power producers Sunfarming and Münch Energie Group. By Alexander Enrique Kuhn, managing partner, Bernhard Hofmann, director, and Jose Joaquin Muñoz Osuna, director, Capcora; and Dr Jens Golz, partner, Simmons & Simmons LLP.

Between 2008 and 2011, Germany stood as the epicentre of Europe's solar industry. Fuelled by proactive policies initiated in 2000 under the Renewable Energies Act (Erneuerbare-Energien-Gesetz or EEG), which introduced 20-year guaranteed feed-in tariffs, the German solar market experienced remarkable growth.

This growth led to a diverse array of developers entering the global stage. However, in late February 2012, the German government abruptly accelerated a planned reduction of feed-in tariffs by three months, surpassing the originally intended cut by a substantial margin. This sudden reduction led to numerous insolvencies, causing a significant portion of the industry to exit the market. In the subsequent years, the sector struggled to reclaim its former vigour, focusing on smaller-scale projects in ground-mounted and rooftop installations.

A return to growth

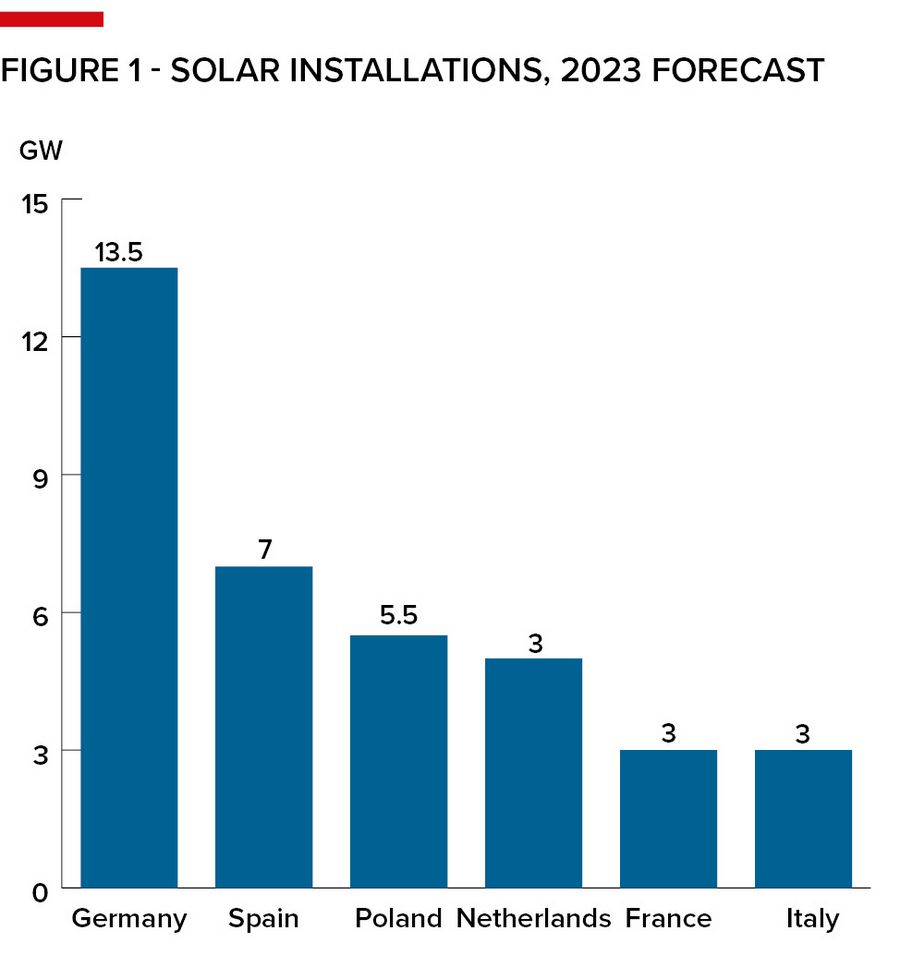

Approximately a decade after this setback, the German solar sector is experiencing an impressive resurgence. In 2022, Germany emerged as the largest market in Europe, boasting 8GW of solar capacity, with expectations soaring to 13GW for 2023.

Simultaneously, the market has witnessed a revival in terms of developer diversity and scale. Many players never entirely left the market; instead, they expanded abroad or continued to grow on a smaller scale. Now that the market is back on track, developers have swiftly returned to their home market or quietly thrived in the domestic market under the radar.

Today, the market is characterised by its heterogeneity, with various business models such as project flipping and selling, as well as market players that have built substantial portfolios over the years, adopting an independent power producer (IPP) strategy.

Two prominent examples of this strategy are companies Sunfarming from the Berlin region and Münch from Bavaria. Both firms have cultivated operating portfolios exceeding 100MWp and have assumed leading roles in developing large-scale projects in their respective regions. Additionally, they boast long company histories, exemplifying the resilience of businesses operating under the radar in recent years.

Both companies recently raised mezzanine financings at their operating portfolio level from a German pension fund, managed by Prime Capital AG in a size of €17.5m in the case of Sunfarming and of €21m in the case of Münch. Both companies were assisted by financial adviser Capcora.

Key past market drivers

The success of these companies can be primarily attributed to three key factors:

* The enduring EEG and feed-in tariff (FIT) system – Germany's EEG and FIT system never completely disappeared from the market landscape. Even when auctions were capped at 10MW, developers could still secure feed-in tariffs through auctions or without auction by realising project expansions or roof-top solar projects in the smaller segment, up to 750kW, later lifted to 1MWp. Compared with several other European countries that entirely abandoned FITs, Germany's 20-year FIT system remained favourable and provided stability for the industry.

* Robust banking environment – Germany's banking environment has continued to provide strong support for solar financing. With the most competitive margins in Europe and backing from KfW, a key German financial institution, this favourable banking landscape has played a pivotal role in the sector's success. As a result, developers have faced minimal equity requirements, making solar projects more accessible and financially viable.

* Declining component prices – Over the past few years, the solar industry has witnessed a significant decrease in component prices. This trend has been particularly beneficial for regions with relatively lower irradiation levels, allowing them to achieve energy independence from subsidies. Lower component costs have driven down the overall cost of solar projects, making them economically attractive even in countries with less favourable sun conditions such as Southern European countries.

The new normal

However, market conditions have undergone significant transformations in the past two to three years. The combination of the global pandemic and the conflict in Ukraine has had a dual impact. On one hand, it disrupted supply chains and introduced volatility to electricity prices. On the other hand, it created a favourable environment for solar expansion. With the German government's ambitious target to boost solar energy capacity to 215GW by 2030, signalling an addition of 20GW in the coming years, the industry is poised for substantial growth. This growth is facilitated by tenders that support companies with feed-in tariffs, serving as a safety net while allowing them to explore power purchase agreements (PPAs) or benefit from merchant prices.

The rise of large-scale solar projects has provided developers such as Sunfarming and Münch with significant opportunities but also new challenges. For example, as of June 30 2023 Sunfarming's project pipeline for the next three years stood at approximately 2.4 GWp, with about 800MWp categorised as late-stage development projects. Developing such extensive pipelines necessitates increased equity, both for feed-in tariff projects and even more for PPA projects.

While traditional bank financing typically covers capital expenditure (capex), accumulating the necessary equity has become a gradual process, largely dependent on the developer's portfolio. Given banks' cautious approach to corporate facilities, the concept of utilising cashflow potential within portfolios through mezzanine structures has gained significant importance.

Navigating complex mezz structures

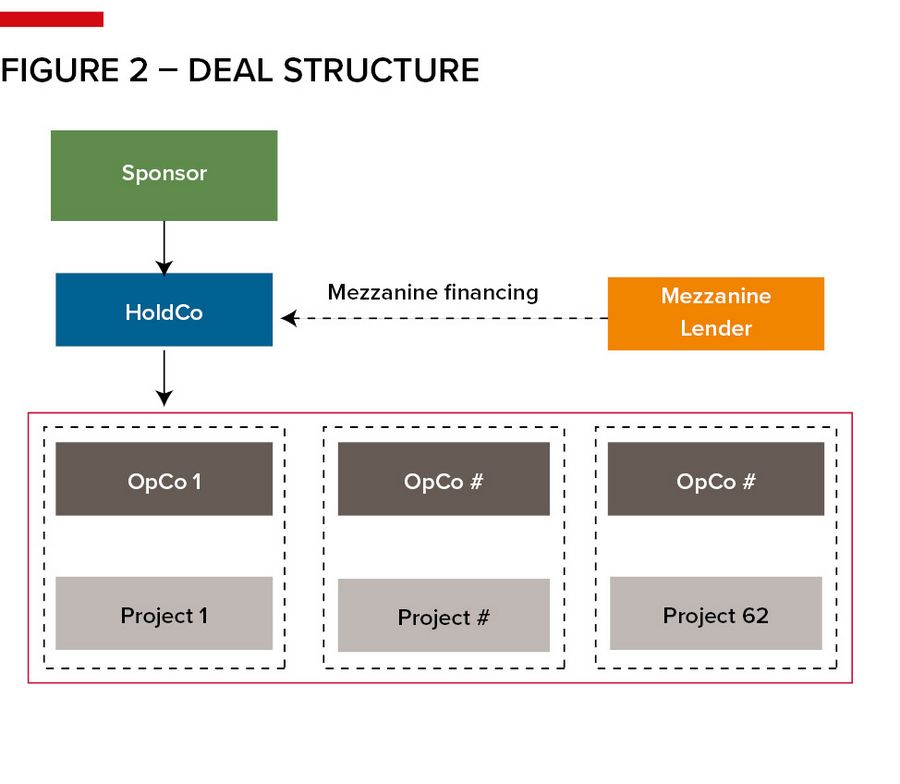

Mezzanine financing involves creating structural subordination at the holding company (HoldCo) level, though implementing it isn't straightforward, especially in well-established structures like those of Sunfarming and Münch. These structures, with intricate intercompany loans and internal EPC contractual relationships, often evolve organically and weren't originally designed for later-stage financing. Thus, careful financial model preparation, often with the guidance of financial advisers, such as Capcora, becomes essential.

In Münch's case, the financial model had to incorporate 62 projects in various stages and with different FIT systems, including battery energy storage system (BESS) projects. These assets resided in different operating companies (OpCos), each with individual bilateral loans and distinct tax histories, adding complexity to the analysis. Additionally, the mezzanine structure offers tax deductibility on the upper level, further complicating documentation required for due diligence.

A tailored approach

Mezzanine lenders wield flexibility, structuring financing based on project-generated cashflow or portfolio equity value. Cashflow-based lending relies on the debt service coverage ratio (DSCR) and targets a mezzanine debt service coverage ratio (MDSCR) typically between 1.1x and 1.4x – ideal for long-term financing or projects with future refinancing plans.

Conversely, equity value-based sizing estimates sizing through portfolio equity value and applies a loan-to-value (LTV) ratio, typically ranging from 50% to 70%, considering market value predictability. This approach is common for short to midterm mezzanine financings, particularly for bridge-to-sales strategies.

Mezzanine financing strategically positions itself between senior lenders and equity investors, offering balanced risk and compensation structures. This intermediary role empowers stakeholders to tailor financing solutions to project nuances, ensuring alignment with objectives. Typically targeting margins between Euribor plus 400bp and 500bp, some lenders may go below this threshold, especially with a high degree of contracted revenues. In practice, contracted cashflows are often retained by banks, leaving mezzanine funders with more merchant-related cashflow-based sizing, especially in Germany, where banks adhere to linear repayment schedules due to KfW refinancing practices.

Due diligence

In the realm of junior debt transactions, structuring the deal is undoubtedly the most essential part, but another cornerstone lies in crafting a tailored due diligence concept. For projects located in Germany an approach has been adopted over the years by German senior banks that differs from those in many other countries. Here, senior banks typically limit their due diligence to internal (own) legal due diligence (LDD), with technical due diligence primarily focusing on yield assessment checks. In comparison, mezzanine debt providers often require external due diligence advice given that they are investing money on trust from pensions funds, insurance companies and the like.

For legal aspects, Simmons & Simmons was chosen as lenders legal adviser acting for the mezzanine provider in both projects, the Münch and Sunfarming transactions. Their adept team boasts extensive experience in similar deals and is proficient in applying a standardised legal due diligence approach tailored to an IPP business model.

What further streamlines the process is that the main project contracts adhere to a standardised format, which is, quite frankly, not comparable to for example FIDIC standard contracts in other jurisdictions. These contracts encompass EPC and O&M agreements with internal group companies, alongside standardised land lease agreements. While the real estate situation is complex in Germany - eg, regarding written form requirement, registration of easements and ownership queries, etc), a market approach has been adopted that is widely accepted in the German market.

Consequently, a concise due diligence process can be executed within a remarkably short timeframe of 4–5 weeks. Additionally, the land register check is, in principle, a straightforward procedure, contributing to the overall efficiency and precision of the process - just depending on how long it takes to retrieve the up to date excerpts from the competent land register.

Security structures

Typically, security structures in junior-type transactions comprise, due to their HoldCo nature, first-ranking pledges over the shares in the HoldCo and first-ranking pledges over the accounts excluding a distribution account of the HoldCo. Share and account pledges are accessory security instruments under German law requiring the existing of a valid claim, ie the repayment claims of the mezzanine lender.

Furthermore, a security assignment of shareholder loans made by the sponsor to the HoldCo is included in the package, to be granted at the signing of the facilities agreement.

Those right in rem security is accompanied by a negative pledge undertaking (which is a contractual obligation to not grant security to any third party) of both HoldCo and the SPVs which usually completes this security framework. This right in rem security is accompanied by a negative pledge undertaking of both the HoldCo and the SPVs, which is a contractual obligation and usually completes this security framework.

Notably, German project financing practices on the OpCo level seldom require SPV pledges and often rely on asset securities. Occasionally, first rank SPV share pledges can be added to the mezzanine security package, but mostly there is no pledge over the shares in the operational companies due to the negative pledge mentioned earlier.

However, it's worth noting that mezzanine lenders often require a kind of consent from the senior banks or at least notification of the senior banks in order to limit the risk of termination of the senior financing due to a change of control. In an event of a default scenario on the mezzanine level, an executed change of control termination right on a senior level could have a knock -on effect on the mezzanine financing and be prevented.

Various forms of “consent” exist, ranging from simply informing the senior bank of the share pledge on the HoldCo level and requesting acknowledgment, up to requiring a pre-emptive confirmation of the change of control (CoC), including know your customer (KYC) checks. The latter is usually less practical (or even impractical), as banks would typically only agree to it with the caveat that they need to conduct KYC at the point of default.

Conclusion

The mezzanine financing market in Germany has experienced significant growth in recent years and is currently experiencing a peak in demand due to market expansion and limited equity resources of the sponsor. It often also takes longer to initially plan to develop and finalise a project, which also increases the need for alternative finance solutions. The emergence of smaller IPPs during the past years, driven by favourable market conditions in terms of policy and the banking environment, presents a valuable opportunity for mezzanine financing, particularly for equity recaps, to fuel further growth. However, these transactions require meticulous preparation and a customised due diligence approach to ensure efficiency.

To see the digital version of this report, please click here.

To purchase printed copies or a PDF of this report, please email leonie.welss@lseg.com