Higher interest rates have pushed investors toward green platforms rather than assets investments. By Alberto Cei, partner and co-founder, Ivan Aloi, partner and co-founder and Davide Petraroli, director, at SURE – Sustainable Revolution.

There is a growing trend for international players to invest in companies active in the field of energy and green transition. They are currently shifting their focus from assets investments toward corporates, targeting either well-established companies or even greenfield platforms well-equipped with a team and a promising development pipeline. This is the consequence of unprecedented global money flow into the renewable and green transition from almost the entire investors’ spectrum that occurred over the last years, especially after the pandemic. Several new players from the PE world started approaching this market too. As such, European M&A transactions’ value in renewables grew by 61% from 2018 to 2022, from €28bn to €45bn.

Initially, infra funds were investing in renewables as a means of diversification and to get a decent yield in a negative-rates market. Later on, the market opened to PE funds, which started approaching the green transition in a more structured way and with completely different logics. Deal sizes increased, investment horizons shrank in line with PE standard parameters, and growth aspects of investments became a key investment consideration. On the other side, direct assets investments – mostly based on regulated tariffs – started losing their appeal with the rise in interest rates.

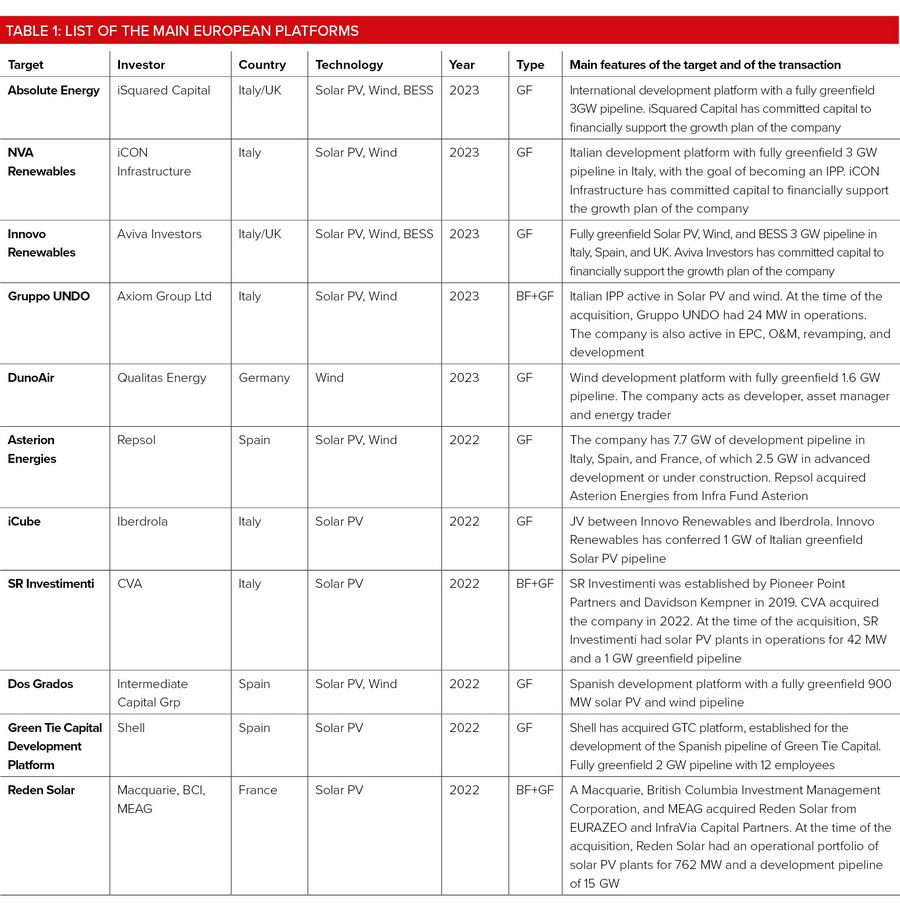

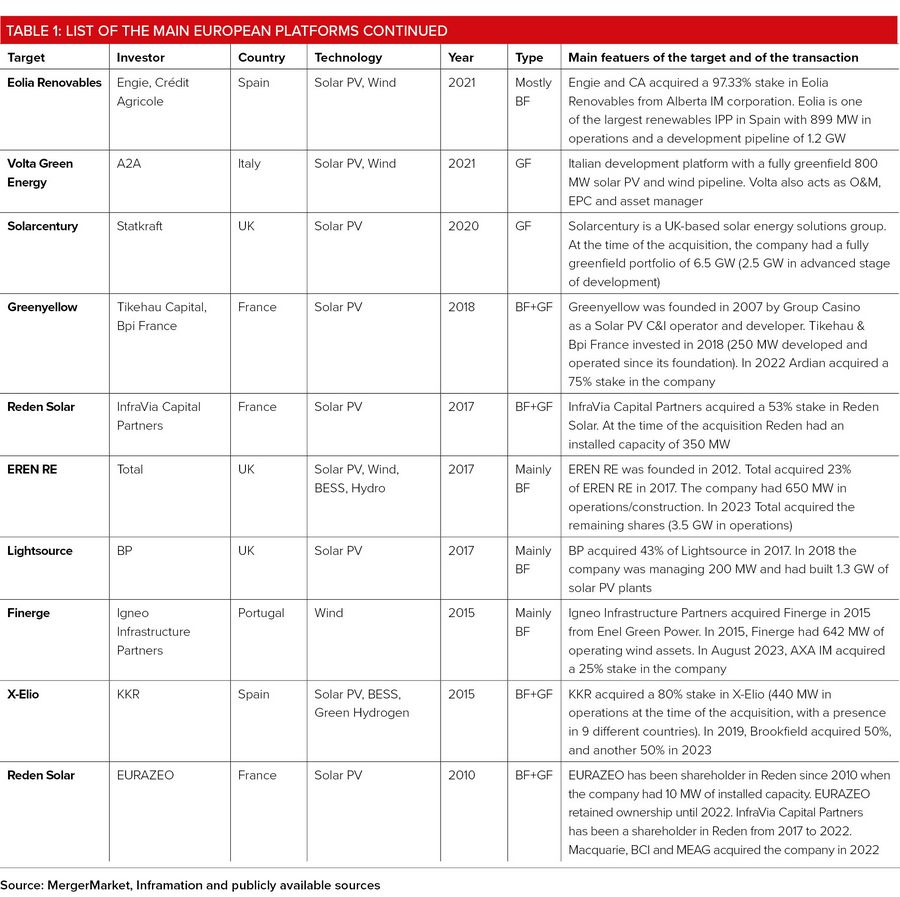

Generally, all investments that are not direct asset deals are referred to as green platforms, although there are a multitude of different forms of platforms. While initially investors started acquiring well-established utilities with a green footprint or operating platforms with a very limited greenfield pipeline, lately platforms’ transactions have started incorporating more and more a greenfield portion and development pipelines. Currently, renewables M&A transactions on purely greenfield platforms are dominating the market, as seen in Table 1. As a matter of fact, while PE and infra funds are willing to take more risk in the development chain in exchange for more juicy returns, local developers and renewable companies are becoming more sophisticated both technologically and financially, giving investors interesting opportunities to target purely greenfield platforms. In this way, investors can also overcome the brownfield part of their investments, which in a high-inflation market has become not very attractive.

In summary, the main elements that contributed to the boost of M&A transactions in green platforms are:

* Rises in interest rates – In the past, in a negative rates environment investors were desperately looking for some yield and renewable infrastructure assets were a good option for them to get a pick-up from treasuries. Now that we live in a high-rates/high-inflation market, such investments are less attractive for investors;

* Global green transition – Today, green investments are not an option anymore but a must. Investing in platforms rather than assets will have the double benefit of i) a greater expected return, ii) speeding up on the growth in a sector that will last for several years;

* Entrance of PE funds to the sector – Today, investments in renewables and energy transition are not a prerogative of just infra funds and utilities, as PE funds need to deploy money in this sector too;

* Creation of global green utilities – The ultimate deal for any investor is transforming a cheap developer into a global green IPP that could be a leader in the future energy market. Green platforms could be a viable option for it.

Today, we are experiencing a peculiar convergence between PE and infra funds, both interested in playing their part in the green transition buying and setting up green platforms. While PE funds are now anxious to put their foot in this sector too – as they remained sceptical on this sector for years – infra funds are willing to raise their IRR, as in a high-rates/high-inflation market they had to drastically review their IRR targets.

This change in the market also contributed to a switch in the skills necessary to assess a platform rather than a pure asset deal. In fact, platforms include elements typical of pure infra deals – ie permitting, construction, non-recourse debt, assessment of technology, etc – combined with more standard corporate elements – ie, team integration, potential growth and internationalisation, governance, management, etc. These new IPPs would also need to carefully balance the international and local involvement, as this will be a key factor in the success of a platform in the long run.

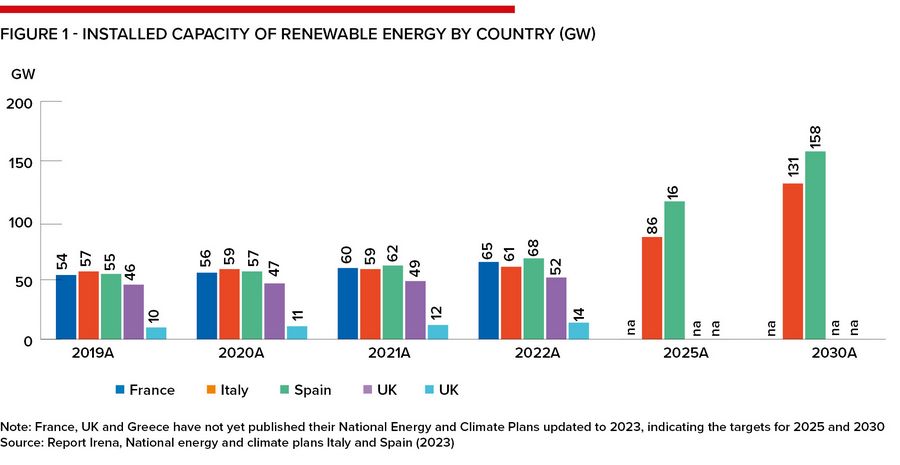

Another important element to consider in setting up a platform is the local context and specifically how various governments are supporting the projects’ development through their legal and regulatory frameworks. Over the last 10 years, the UK and Greece have shown the highest growth rates in renewables – CAGR 2013–2022 of 11.4% and 6.9% and an installed capacity of 52GW and 14GW at year-end 2022 respectively – followed by France and Spain – CAGR 2013–2022 of 5.9% and 4.2%, and installed capacity of 65GW and 68GW at year-end 2022 respectively – while Italy is catching up with CAGR of 1.4%, despite a relevant nominal installed capacity of 61GW.

While the UK and France opted for a simplified authorisation process for projects with a capacity below 50MW, speeding up the overall development process, Italy put a lower threshold at 20MW for the fast-permitting, with the other projects taking much longer to reach the ready-to-build status, more than 20 months on average. Moreover, the more successful countries have stuck to clear incentive schemes such as the CfD, giving a strong message of reliability to the market, which in turns has established a liquid and mature corporate PPA market.

Spain is a clear example where a flexible regulatory framework coupled with a liquid PPA market resulted in constant renewables growth. On the other side, countries like Italy still show strong growth potential – also considering high sun irradiation, advanced agriculture and a strong technological and industrial background – which could give a valid alternative to countries where today returns are compressed by fierce competition.

This market transformation has a strong impact on debt-financing too. In the past, we have experienced the “old-style” single asset project finance moving toward portfolio and HoldCo financings (in the form of loans or project bonds). We have also seen private debt funds aggressively approaching the market with new products focused on construction and even development financing, competing with commercial banks structures. Now, the increase of new green platforms in the market is forcing lenders to push toward even more flexible and hybrid structures, encompassing a combination of PF with corporate finance elements. The financing package could include a combination of HoldCo financing, asset financing and warehousing facilities.

The growing of green platforms can be seen as the natural evolution of energy transition and the renewable market from pure generation toward a fully interconnected green energy system, where BESS will play a crucial role in balancing the network. By investing in platforms, rather than assets, investors are putting their first stone into this new energy market. Playing a leading role in it would mean much greater value for investors than living on dividends’ flows.

To see the digital version of this report, please click here.

To purchase printed copies or a PDF of this report, please email leonie.welss@lseg.com