India pledged at the COP26 conference in Glasgow to becoming net-zero by 2070 and achieving 45% lower emissions intensity of GDP by 2030 than 2005 levels. By Arun Kumar Saluru, vice-president, project advisory and structured finance, SBI Capital Markets, Mumbai

To further complement these ongoing efforts, India is prioritising green hydrogen as a potential solution to decarbonise hard-to-abate sectors such as refinery, ammonia, methanol, iron and steel and heavy-duty trucking. In this regard, the Government of India (GoI) announced its National Green Hydrogen Mission in January 2023 with the aim of making India the world’s largest hydrogen hub.

Based on the manufacturing process, hydrogen has been given colour codes – green hydrogen, produced by electrolysis splitting water molecules into hydrogen and oxygen through an electrolyser using renewable energy; and grey hydrogen, produced conventionally from natural gas.

Electrolysers

The electrolyser is the heart of the green hydrogen production unit. There are two types of electrolysers being mainly used at present in the industry: alkaline electrolysis (AE) – this type of electrolyser uses a liquid alkaline electrolyte solution for splitting water into hydrogen and oxygen – and polymer electrolyte membrane (PEM), which uses a solid polymer membrane for splitting water into hydrogen and oxygen

Globally, the market for electrolysers is dominated by alkaline, with a 61% market share, and polymer electrolyte membrane, with a 31% market share. Technologies with advanced electrolysers such as solid oxide and Anion Exchange Membrane (AEM) are also nearing commercial deployment.

PEM components rely on rare earth metals but can better handle variations in power, work at low plant capacity and are compact, whereas alkaline electrolysers rely mostly on nickel, whose supply is more diversified than rare earth metals, and are advantageous when it comes to scale deployment. As electrolyser deployment moves towards a gigawatt-scale market, the lower cost of alkaline electrolysers is advantageous when it comes to scale deployment.

In general, the European Union and US are the global leaders in PEM electrolyser technology and Chinese manufacturers are leaders in alkaline electrolysers. A series of electrolysers are deployed for production of green hydrogen. At present, a 10MW PEM electrolyser produces about 180kg of green hydrogen per hour. Most of the project cost of green hydrogen plants consists of the cost of electrolyser, about 60% to 70% of the project cost. The cost of a 1MW alkaline electrolyser is about US$1m and the cost of a 1MW PEM electrolyser is about US$1.4m.

End-use industries of hydrogen

The present annual consumption of hydrogen in India is about 6MMT (million metric tonnes), derived from fossil fuels, and it is mainly consumed in petroleum refining and manufacturing of ammonia for fertilisers. It is also used in methanol production and in the steel industry. Ammonia manufactured from green hydrogen is called green ammonia. Demand for hydrogen in India is expected to reach about 12MMT by 2030.

At present, the green hydrogen Industry is in the nascent stage of conceptualisation, at the pilot and demonstration plant stage and small scale. Most of the green hydrogen produced is consumed in situ. Indian companies have announced plans to set up electrolyser manufacturing plants and green hydrogen and green ammonia plants in collaboration with foreign entities that have expertise in the area. Reliance Group, NTPC, ONGC, Greenko, Renew Power, Acme Group, etc, have announced projects in a green hydrogen ecosystem coming up in next five to ten years aggregating to investment of billions of US dollars.

Production costs

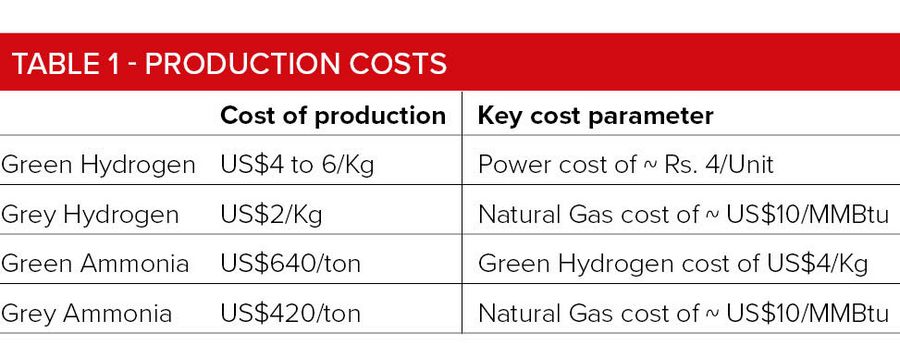

The production cost of green hydrogen and green ammonia at present is more than that of grey hydrogen and grey ammonia.

About 70% of green hydrogen production costs are on power consumption. Depreciation costs are about 18%. Hence, the cost of power and the capital cost of electrolysers are significant factors in production costs. This makes it hard for green hydrogen to compete at present with the cost of grey hydrogen. So, to compete with grey hydrogen, the costs of renewable power and electrolysers need to come down. With technology innovations and domestic production, the cost of electrolysers is expected to progressively come down. The production cost of green hydrogen is being targeted at US$1/kg by 2030.

Government policies and support

The GoI intends that by 2030, 40% of hydrogen consumption should be met by green hydrogen and it aims to make India the global hub for production, usage and export of green hydrogen and its derivatives and progressively reduce the country's reliance on fossil fuels.

* National Green Hydrogen Mission, January 2023 – the GoI approved the National Green Hydrogen Mission in January 2023. The mission's objective is the development of a green hydrogen production capacity of at least 5MMT per annum with an associated renewable energy capacity addition of about 125GW in the country.

The initial outlay for the mission will be Rs19,744 crore. This includes Rs17,490 crore, under the Strategic Interventions for Green Hydrogen Transition Program (SIGHT) wherein two financial incentive mechanisms would be aiding domestic manufacturing of electrolysers and production of green hydrogen. Rs1,466 crore has been allocated to pilot projects in emerging end-use sectors such as steel, long-range heavy-duty mobility and shipping, etc; Rs400 crore has been allocated to research and development (R&D), and Rs388 crore to other mission components. The Ministry of New & Renewable Energy (MNRE) will formulate the scheme guidelines for implementation of the respective components.

The mission aims to produce wide-ranging benefits. Key benefits envisaged are the creation of export opportunities for green hydrogen and its derivatives; decarbonisation of the industrial, mobility and energy sectors; a reduction in dependence on imported fossil fuels and feedstock; development of indigenous manufacturing capabilities; creation of employment opportunities; and development of cutting-edge technologies.

The mission's implementation is envisaged in phases. In the first phase, 2022/23 to 2025/26, the focus will be on deployment of green hydrogen in sectors that are already using hydrogen, and evolving an ecosystem for R&D, regulations, and pilot projects. The focus of Phase I will be on creating demand while enabling adequate supply by increasing the domestic electrolyser manufacturing capacity. The later phase, 2026/27 to 2029/30, of the mission will build on these foundational activities and undertake green hydrogen initiatives in new sectors of the economy.

* Green Hydrogen Policy, February 2022 – A Green Hydrogen Policy has been framed by GoI with its major objective to aid in the reduction in the landed costs of renewal power and to encourage the transition from fossil fuel to green hydrogen/green ammonia. The following are key features of the policy:

i) Waiver of inter-state transmission charges for 25 years for green hydrogen and green ammonia projects commissioned by June 30 2025;

ii) Single portal of MNRE for all statutory clearances in a time-bound manner;

iii) GoI proposes to set up manufacturing zones. Green hydrogen/green ammonia production plants can be set up in any of these zones.

iv) Renewable energy consumed to produce green hydrogen/green ammonia will count towards compliance with the renewable purchase obligations of the consuming entity.

Challenges in the sector

Despite the unique possibilities and advantages, the following challenges are being faced at present by the industry.

* Unfavourable cost economics vis-a-vis hydrogen produced from fossil fuels.

* There are no commercial green hydrogen plants in India as yet – Only some small capacity plants are being put up on balance sheet funding, although plans have been announced by big industrial groups.

Larsen & Toubro (L&T) commissioned in August 2022 a 380kW alkaline electrolyser-based (45kg/day) green hydrogen plant at its engineering complex in Hazira. GAIL is implementing a 4.3 tonnes per day green hydrogen plant in MP expected to be commissioned in FY 2024. IOCL is implementing 5KTPA (1,000 tonnes per annum) and 2KTPA green hydrogen plants at the Mathura & Panipat refineries respectively.

ACME Group, India, has set up the world’s first integrated pilot project for green hydrogen and green ammonia plant at Bikaner in Rajasthan. In this project, green hydrogen is being produced using 5MWp from the solar plant, scalable to 10MWp. The plant will help in saving about 4,400 tonnes per annum of CO2 emissions.

Oil India Ltd (OIL) commissioned a 99.999% pure green hydrogen pilot plant with an installed capacity of 10kg per day at its Jorhat Pump Station in Assam in April 2022. The plant was commissioned in a record time of three months. The plant produces green hydrogen from the electricity generated by the existing 500kW solar plant using a 100kW AEM electrolyser array. AEM technology is being used for the first time in India. The company has initiated a detailed study in collaboration with the Indian Institute of Technology, Guwahati, India, on blending green hydrogen with natural gas and its effect on the existing infrastructure of OIL.

* Consistent demand – At present, demand for green hydrogen is a challenge in view of the higher cost of production vis-à-vis grey hydrogen. A policy push would be required from the GoI to make available consistent demand from fertiliser plants, refineries and for blending green hydrogen in sales by city gas distribution companies. This will provide demand certainty for early green hydrogen projects and encourage market development.

* Electrolyser supply – At present, te global commercial electrolyser manufacturing capacity is estimated to be only about 2GW-4GW per annum, whereas India would need electrolyser capacity of 65GW by 2030 for production of 5MMT per year of green hydrogen. Domestic production of electrolysers is yet to take off meaningfully.

* Nascent infrastructure – Infrastructure for transportation and storage for the utilisation of green hydrogen is to be built, which would involve time and costs. Hydrogen before transportation in containers needs to be compressed or liquefied by cooling to –252℃. The challenge for compressed hydrogen storage is that hydrogen’s low density results in the need for large containers – three times the size used for natural gas. Liquefaction also has higher energy costs – up to 30% of the energy content of the fuel compared with 4%–7% for compressed hydrogen.

* Availability of debt funds – Financing remains a big challenge, especially since the industry is at a nascent stage and until bankability of projects is established. Green hydrogen-specific funding by the GoI for domestic pilot projects would increase industry and lender confidence and help ease this transition.

* Lack of harmonised standards and codes – Since the industry is in a nascent stage in India, standards and codes for manufacture and safety for the entire chain of green hydrogen is required to be put in place.

Support to industry

* Support for the creation of demand for green hydrogen – In order to create bulk demand and scale up production of green hydrogen, the GoI may need to specify a minimum share of consumption of green hydrogen or its derivative products such as green ammonia by designated consumers as energy or feedstock. Long-term offtake agreements with these designated consumers would aid in establishing bankability of green hydrogen projects.

* Mechanism for disbursement of incentive packages under GoI policies – Notification on the eligibility criteria, bidding criteria and rules for availability of incentive packages that have been announced under the National Green Hydrogen Mission and the Green Hydrogen Policy is expected by the GoI shortly.

* Government policy push for exploring lowering the cost of renewable power – A central and state government policy push may be required to explore waiving of charges in renewable power, such as for distribution losses and other taxes and duties, initially for a five-year period in order to lower the cost of renewable power for producing green hydrogen and its derivatives. As the scale of manufacturing of green hydrogen increases, these waivers may be looked at afresh.

* Fiscal incentives to lower the cost of production and attract investments – A reduction in the duty on import of equipment for manufacturing electrolysers and setting up green hydrogen plants for the next five years may be considered, which may then be gradually reassessed; 100% accelerated depreciation benefits on new investments in green hydrogen technologies and plants should be considered; and tax deductions – ie, the deduction of 100% of profits obtained from the businesses of an enterprise involved in developing green hydrogen for specified assessment years after commencement – under Section 80IA of the Income Tax Act, 1961 may be considered.

* Access to low-cost funds – The government should create a fund so that low-cost funds are available to the green hydrogen industry. Long tenors, 10 to 15 years, and lower costs funds for green projects from the banking system needs to be explored.

* Notification of harmonised codes and standards – Any sunrise industry requires robust regulatory architecture, safety codes and relevant quality and performance standards to guide the technology developments. Efforts should be made to harmonise regulations and standards with internationally accepted norms to ensure inter-operability of technologies, and incorporation of global best practices.

References

1 - Report “Harnessing Green Hydrogen – Opportunities for deep decarbonization in India” by Niti Aayog. https://www.niti.gov.in/sites/default/files/2022-06/Harnessing_Green_Hydrogen_V21_DIGITAL_29062022.pdf

2 - https://www.blackridgeresearch.com/reports/global-electrolyzer-market

5 - https://www.iocl.com/NewsDetails/59319

6 - https://www.ammoniaenergy.org/articles/the-cost-of-co2-free-ammonia/

7 - https://renewablesnow.com/news/green-ammonia-costs-double-that-of-grey-ammonia-argus-745643/

8 - https://mnre.gov.in/img/documents/uploads/file_f-1673581748609.pdf

9 - https://powermin.gov.in/sites/default/files/webform/notices/Green_Hydrogen_Policy.pdf

11 - https://www.bseindia.com/xml-data/corpfiling/AttachLive/3d05b702-b9cb-41e2-aa21-a79517dda804.pdf

To see the digital version of this report, please click here.

To purchase printed copies or a PDF of this report, please email leonie.welss@lseg.com