There is a now blueprint for financing utility-scale projects in South Africa for various offtake structures, and lenders and investors are allocating large amounts of capital to fund these projects – bringing much needed energy online. And it is just the icing on the top that these are carbon-neutral generation technologies. By Wickaum Smith, Green Giraffe.

The Renewable Energy Independent Power Producer Procurement Programme (REIPPPP) is an initiative created by the South African government aimed at increasing private-sector electricity generation and investment with the use of renewable energy technologies, which over the past years has consisted of solar PV, concentrated solar, onshore wind, hydro-electric, landfill gas, biomass, and biogas. It was first announced at COP 17 and there have been six auction windows to-date, with the projects from the first four windows being fully operational and bringing online 6.3GW of power.

The projects from Bid Window 4 achieved preferred bidder status in 2015 and it was six long years later that Bid Window 5’s auction date was announced. Growing up in South Africa and experiencing rolling black-outs – or loadshedding as it’s colloquially referred to – since 2008, I would have suspected that any opportunity to bring online new generation capacity would be prioritised and streamlined, but instead we have seen severe bottlenecks from the South African government, the energy regulator and the country’s state-owned electricity utility.

When Green Giraffe first opened its office in Cape Town in 2017, we didn’t expect to wait as long as we did before the next government auction but since then, we have been involved in three tender processes, namely REIPPPP Bid Windows 5 and 6 as well as the Risk Mitigation Independent Power Producer Procurement Programme (RMIPPPP). We have seen the projects from Bid Window 5 reach financial close with the RMIPPPP tentatively expected to follow suit in Q2/Q3 2023. We believe that utility-scale renewable energy projects are the fastest and cheapest way to bring online generation capacity in South Africa, and we believe that Bid Window 5 is the case study that will hopefully pave the way and lead to an acceleration in future projects coming online.

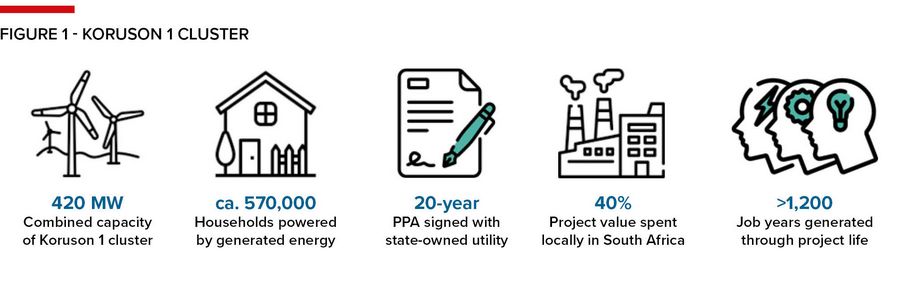

In October 2021, EDF Renewables (EDF R), together with its partners H1 Holdings and Gibb-Crede – the EDF R consortium – were awarded preferred bidder status on three projects – the Koruson 1 Cluster – as part of the REIPPPP Bid Window 5. Financial close for the first two projects, the San Kraal Wind Energy Facilities (SK) and Phezukoymoya Wind Energy Facilities (PHE), was reached in November 2022 and in January 2023 financial close was reached on the third project, Coleskop Wind Energy Facilities (COL).

Each project consists of an onshore wind farm of 140MW, located on the border between the Northern and Eastern Cape Provinces, in the municipality of Umsobomvu. In total, out of the 25 projects that were awarded preferred bidder status, only six have reached financial close, making it all the more impressive that the EDF R consortium was the first to reach financial close on three of those projects.

The initial target financial close date for all Bid Window 5 projects was scheduled for April 2022, a mere six months after preferred bidder status was awarded; however, with unclear delays from the South Africa government, together with the state-owned electricity utility’s slow decision-making, the financial close date slipped from April, first to July, then September, with the EDF R consortium finally closing in November 2022.

EDF R’s commitment to investing in renewables in South Africa over the past decade, coupled with its long-standing relationships with local stakeholders and suppliers, ensured that it was able to mitigate the supply chain delays and reach financial close, despite the delays, thereby achieving an important milestone in de-risking projects and securing the necessary capital to proceed with construction.

The Koruson 1 cluster has a combined capacity of 420MW and will eventually meet the electricity needs of approximately 570,000 households once operational. Each site will comprise of 26 wind turbine generators, each standing over 120m tall with a blade length of around 80m. The total capital cost for the three projects is in the region of R11bn and they are expected to be commissioned in late 2024. The three plants will connect to the Koruson Main Transmission Substation, which is being constructed by the EDF R consortium.

The asset will be transferred to South Africa’s electricity parastatal upon completion. The construction of these wind farms will lead to more than 300 full-time jobs during the construction period, with the operations leading to more than 30 full time jobs for the entire duration of the 20-year operating period. Some 40% of the project value will be spent locally in South Africa, with 1.2% of revenues generated going to socio-economic development initiatives for nearby communities.

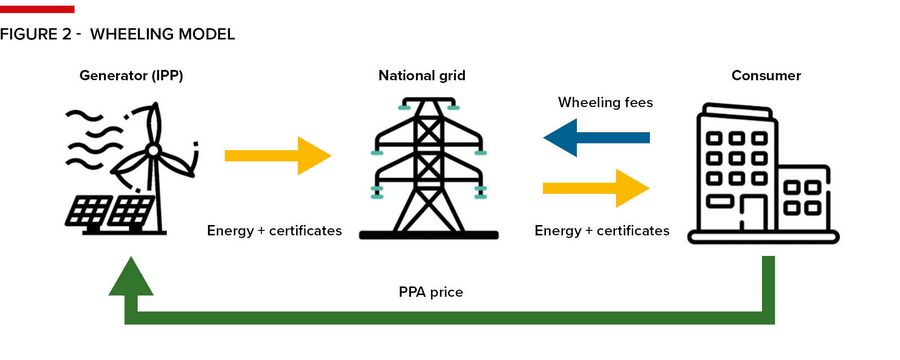

A trust has also been formed for the local community under the terms of which they will own a 2.5% stake in all three projects and receive pro rata distributions from each SPV. The power generated by the Koruson 1 cluster will be supplied to the national grid under a 20-year power purchase agreement (PPA). Financing came from a bank club comprising three commercial lenders and a debt fund, namely Standard Bank, Absa Bank, Investec and Momentum Metropolitan. The lenders provided two senior debt facilities, in the form of CPI-linked debt and JIBAR-linked debt, a subordinated quasi-equity facility, a Debt Service Reserve Facility (DSRF) and a VAT facility.

Green Giraffe acted as sole financial adviser to EDF R, supporting it on all financing aspects, testing the market and engaging in conversations with various commercial lenders and debt funds active in the South African infrastructure sector and in renewable energy in particular. Our experience from these discussions is that there is a large allocation of debt dedicated purely to renewables projects, with commercial lenders even deciding to split out resources from their greater infrastructure teams to focus purely on opportunities in the energy sector. In addition to the debt allocation and focus, we see lenders becoming more sophisticated with their offerings and providing more competitive terms, which raises the question, why are there not more transactions being financed and why can’t this happen even faster?

It would appear that the private sector has seen what the government has missed: renewable energy is a fast way to bring energy online, and the rise in utility-scale commercial and industrial (C&I) renewables projects will no doubt be a critical component of the energy mix in South Africa in the future. Bottlenecks, delay, and energy management/generation issues in part stemmed from a centralised generation model in South Africa, whereby the country’s energy parastatal was sole provider to residential, C&I and even local municipalities electrical energy needs.

Moving forward, we will most likely see further liberalisation on electricity generation through C&I consumers as well as local municipalities securing offtakes from private-sector generators. The City of Cape Town municipality has announced its request for proposals to procure electricity, with other municipalities expected to follow suit.

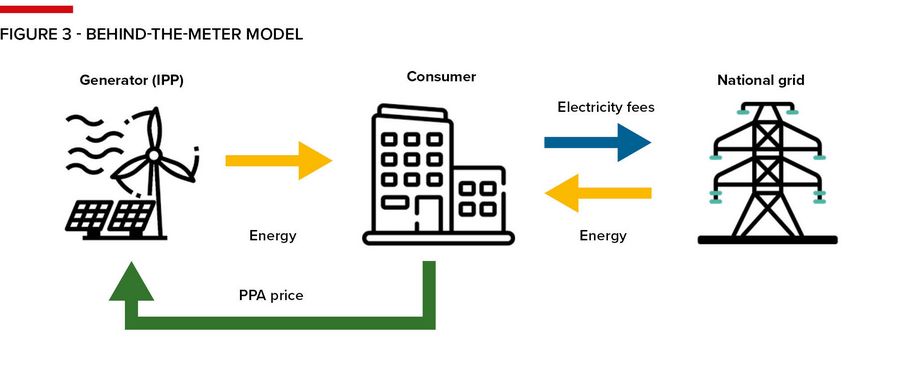

Utility-scale projects are no longer only bankable via national government tenders such REIPPPP or RMIPPP, but they can now secure revenues by generating energy for private and local government municipal offtakers – something that was not possible in South Africa until fairly recently. Local industries can now protect themselves from rapidly increasing costs while also pro-actively reducing their carbon footprint by purchasing energy directly from IPPs.

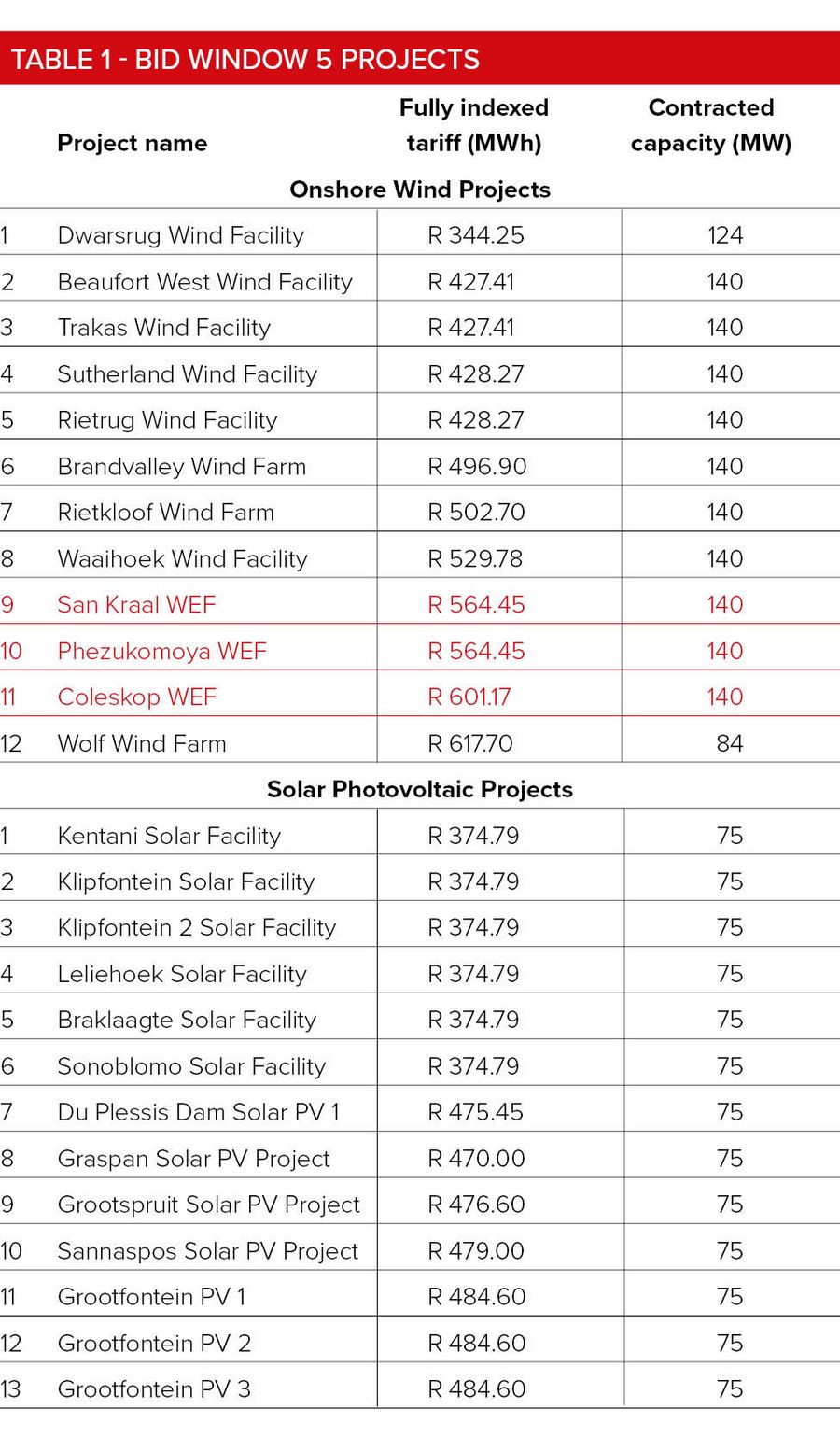

They can make this switch quickly due to the relatively short construction period for new renewables plants. If we look at renewable energy plants: utility-scale solar PV power plants can be constructed within 12–18 months while onshore wind projects take 18–24 months. In comparison, the construction period for coal-powered plants can take upwards of 60 months and nuclear tops the list, taking up to 96 months, eight years, to construct. In addition, the indexed tariff secured for onshore wind projects awarded preferred bidder status were between R344.25 and R617.70/MWh and for solar PV projects between R374.79 and R484.60/MWh, which demonstrates the potential for extremely low levelized costs of energy (LCOEs) from renewables generation when compared with traditional fossil fuel generation.

As a result, we are seeing the first set of projects with corporate power purchase agreements (cPPAs) being constructed in South Africa, which will help to bring more renewables generation online in parallel to the REIPPPP. There are many of lessons to be learnt from these latest Bid Window 5 closings that can be implemented in the South African C&I projects rapidly being developed, financed and constructed.

Many of South Africa’s commercial lenders have taken the view that large-scale C&I deals have a similar characteristic to those financed in the REIPPPP: broadly speaking, they are all utility-scale and they have long-term energy offtake contracts. There are indeed some significant differences in cPPAs compared with REIPPPP PPAs, which lenders will have to pay close attention to when determining their risk, but the barriers to credit approval and appetite for lending are already very favourable, especially considering how new this route to market is in South Africa.

So, what does this mean for the energy sector in South Africa? We know that there are severe and growing issues with grid connection capacity in the country, as highlighted by the Bid Window 6 results, which slow down the speed at which new projects can come online; however, every additional utility-scale project that comes online theoretically alleviates the generation burden on the state-owned electricity utility, and in turn allows it to focus on the planned unbundling into three separate entities – each focused on transmission, distribution and generation. In the short term, we can therefore expect a reduced burden of energy consumption on South Africa's energy parastatal – or increased generation capacity, depending on how you look at it – as well as the fast evolution of financing terms for projects with cPPAs.

In the long term, we would expect this to lead to a liberalised electricity market in which prices are driven down by private sector competition. The development of a steady stream of projects could lead to more original equipment manufacturers (OEMs) setting up manufacturing locally, further driving down capex figures while creating local employment opportunities.

We have also seen the South African government making changes in the proposed amendments to the electricity act to create an environment in which more generation can come online faster and with less red tape. This may seem like an optimistic view on the future of energy security in South Africa and no one will deny that the steps that the South Africa government take in the coming years will be crucial to the country's economic health, but the fact remains: there is a blueprint for financing utility-scale projects in South Africa for various offtake structures, and lenders and investors are allocating large amounts of capital to fund these projects, bringing much needed energy online. And it is just the icing on the top that these are carbon neutral generation technologies.

To see the digital version of this report, please click here.

To purchase printed copies or a PDF of this report, please email leonie.welss@lseg.com