The incentive-laden Inflation Reduction Act could go a long way in propelling the US towards a net-zero future. Aneesh Prabhu, senior director and sector lead, North American Infrastructure, S&P Global Ratings, examines the tailwinds for the power sector and diverging approaches with Europe's decarbonisation plans.

Signed into law in August 2022, the US Inflation Reduction Act aims to lower the cost of clean energy technologies and encourage the adoption of low-carbon alternatives. Yet as federal agencies pass the six-month implementation mark, a real economic divide is emerging between the US and Europe, with growing concerns that the act could favourably position US entities over their EU-based peers.

Certainly, the act has sparked competitiveness fears in the EU, already under pressure from high energy prices and the Russia-Ukraine war. The act's broad-based provisions will incentivise consumers to adopt low-carbon technologies, helping fund green hydrogen, electric vehicles (EVs), renewable energy, and battery storage. But it also aims to protect nuclear and oil and gas base-load generation, underscoring the US focus on energy security.

According to estimates by the Joint Committee on Taxation and the Congressional Budget Office, the act is expected to invest US$437bn over 10 years, while raising US$737bn in new revenues. However, the path ahead is not without obstacles, and the acceleration of new projects could exacerbate existing labour shortages – and lead to higher costs. What’s more, new projects that plan to take advantage of certain tax credits must be compliant with the prevailing wage as determined under the Davis-Bacon Act – a provision that might deter entities from participating.

As such, a concerted effort will be needed to increase the labour supply in affected regions to avoid fuelling inflation and cost overruns, and large-scale reskilling of workers may be necessary to ensure the act’s success.

Tailwinds

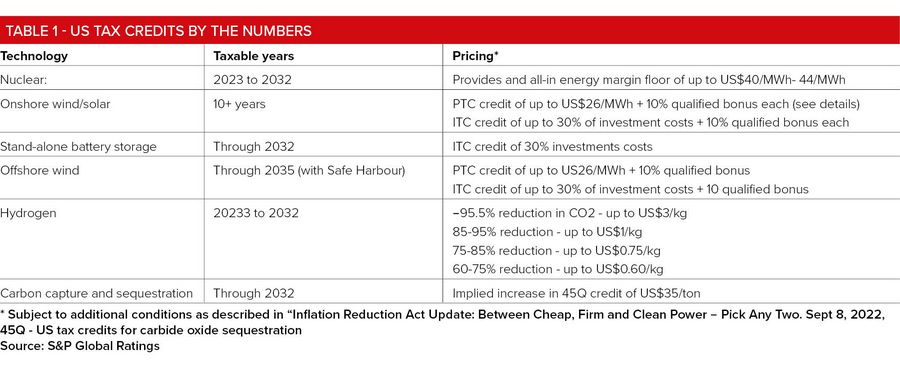

That said, the act is a true gamechanger for certain segments within the power sector. Both onshore and offshore wind, as well as solar generation, are set to benefit from the long-term extension of production tax credits (PTCs) and investment tax credits (ITCs). Indeed, clean energy investments accelerated through October and November last year, Figure 1.

More immediately, however, the act will have a positive impact on the nuclear power generation and carbon capture segments of the energy market. Following their approval, new PTCs will provide floor pricing protection for existing nuclear generation of US$44/MWh for nine years beginning in 2024. Going forward, the IRS is expected to issue guidelines that will define revenues to help determine the size of the credit. Similarly, new PTCs for standalone storage are significant for the sector.

Elsewhere, the act increases the value of dedicated storage of CO2 in the power industry to US$85/ton from US$50/ton, and by lowering capture thresholds to 18,750 tons per year, the act will expand the number of projects eligible for tax credits. However, even though these benefits are robust, the number of entities that can take advantage of credits are likely to be constrained by limited access to caverns capable of storing the captured carbon.

Hydrogen push

Perhaps the most significant provision of the Inflation Reduction Act is its green hydrogen PTC. By accelerating deployment across the US, it could make the technology economical a decade sooner than expected and, in turn, create a substantial market for green hydrogen production.

While, based on general assumptions, we estimate the current average cost of generating hydrogen is about US$3.75/kg, taking into account the PTC benefit, S&P estimates the net cost of generating hydrogen is about US$0.8/Kg – or equivalent to about US$7.25/thousand cubic feet (MCf) of natural gas. With properly located electrolysers, this could see green hydrogen compete with its currently more economical grey counterpart – opening up the existing 10 million tons per annum market to green hydrogen.

In addition, the act allows green hydrogen projects to benefit from a separate wind and solar PTC, further reducing the levelized average cost of hydrogen production. This could also facilitate the pairing of hydrogen with large, base-load generators such as nuclear power stations.

Energy security concerns

With energy security still a key policy priority, the act has been designed to have a limited, near-term credit impact on domestic oil and gas companies. In contrast to the Biden administration’s original platform of restricting oil and gas drilling, the act will open up additional federal land for lease sales, in addition to offshore leases in the Gulf of Mexico. What’s more, act has introduced higher royalty rates for onshore leases and fees on methane emissions, even if the overall cost impact will equate to less than US$3/barrel, according to S&P Commodity Insights.

Long term, however, the acceleration of the energy transition could lead to higher costs for those US oil and gas companies without adequate investment in carbon sequestration and methane-reducing technology. While many midstream companies are already investing in such capabilities, the capital cost of carbon sequestration may be prohibitive for smaller producers. If, over time, they struggle to compete, it will spur a significant increase in M&A activity and create meaningful barriers to entry for new market participants.

Moreover, projects also face permitting challenges. To develop large-scale carbon capture, companies must acquire Environmental Protection Agency (EPA) approval for Class VI wells, which are used to permanently inject CO2 into deep underground geological formations. Such approvals can take several years. So far, only two states, North Dakota and Wyoming, have secured primary jurisdiction to oversee such projects instead of the EPA.

US approach

The US’s subsidy-based approach is somewhat at odds with the more stringent regulations within the EU, in no small part due to the simplicity of its implementation through the corporate tax code. Mechanisms such as the act’s direct pay and transferability features eliminate the need for complex tax equity structuring – substantially increasing cashflows and making it easier for companies to monetise renewables credits. In addition, the act by itself does not layer additional mandates and therefore could be marginally credit-accretive to entities that benefit from its numerous provisions.

By comparison, Europe has much stricter and more complex regulations attached to its transition-based benefits. Grant mechanisms are generally longer and more complex owing to the administrative burden at both EU and country level – and from the perspective of investors, the layers of multisector support are more complicated than those in the US.

The US and the EU also have diverging attitudes towards fossil fuels. Both the EU Green Deal and Fit for 55 target demand for carbon-intensive products and services, with a focus on stronger carbon pricing and binding sector targets. However, these efforts to decarbonise and reduce dependence on fossil fuels come at a cost. This may affect the competitiveness of European industries exporting to the US and further afield.

EU and US on diverging paths

By contrast, the Inflation Reduction Act is clearly structured to ensure energy security – particularly in light of the Russia-Ukraine war. The act provides opportunities for ongoing investment in oil and natural gas supply while facilitating and balancing a smooth transition to cleaner burning fuels.

Another key difference is technology. The European support scheme is technologically biased, adding another layer of complexity to its rules. For example, it limits the type of gas-fired assets and use of nuclear energy that can qualify as part of its clean energy protocol. In comparison, the Inflation Reduction Act is generally technology agnostic, allowing for certain US regions to take advantage of technology that best suits their respective needs and capabilities. This approach leaves room for new technology as it develops and could favour the US in clean technologies development – ultimately leading to a smaller competitive edge for some European companies.

The act favours US-based suppliers over EU-based production, and entities outside the US will consider scaling up their presence and facilities in the country accordingly. While the European approach does not currently require a domestic supply chain, certain tax credits available to the US energy sector demand domestic content. Indeed, by complying with local content requirements, particularly the Federal Transit Authority’s “Buy America” regulations, companies can increase their PTC/ITC credits between 2% and 10%.

Moving forward, broader political imperatives – in the light of the war in Ukraine and strained relations with China – will likely prevent an escalation into a trade conflict between the US and EU. However, the act will remain a key topic on both sides of the Atlantic. So far, the EU has responded to the impact on its competitiveness by initiating some improvements to facilitate state aid rules. Meanwhile, senior European leaders, including French President Emmanuel Macron, German Chancellor Olaf Scholz, and European Commission President Ursula von der Leyen, have visited Washington DC to urge favourable treatment of European businesses, particularly automakers.

Economic hurdles ahead

As the act’s implementation continues to progress, key specifics are yet to be finalised. And, despite the act’s benefits, any forthcoming administrative complexities may dissuade operators from participating. The implementation itself will span several federal agencies – including Treasury, Energy, Agriculture, Interior and the Internal Revenue Service – and only some, such as the EPA, can leverage prior experience implementing grant programs.

Wider economic factors may further limit the impact of the Inflation Reduction Act. Recent data regarding the health of the jobs market and wage growth may signal reduced fears of recession. However, this suggests that the Federal Reserve could implement additional rate hikes, maintaining their peak for longer than previously expected.

As such, higher prices and interest rates would increase costs for infrastructure projects, with softer economic gains from investments. Essentially, infrastructure projects may end up costing more, despite the act’s incentives.

Under current circumstances, it is also unclear how successful the act will be in driving short-term economic gains. Near-term financial benefits are unlikely to dramatically offset gloomy economic forecasts – the Congressional Budget Office estimates that the act may add just between 0.84% and 0.88% in GDP growth by 2030.

Nevertheless, the Inflation Reduction Act is a turning point in the US drive to net-zero. It will be highly consequential for the development of low-carbon technology, while also preserving energy security. Ultimately, the jury is still out on whether the US approach will be more or less successful than that of the EU in achieving decarbonisation. And time will tell whether, in the long-term, these approaches eventually converge.

To see the digital version of this report, please click here.

To purchase printed copies or a PDF of this report, please email leonie.welss@lseg.com