The US government recently introduced multiple incentives for the hydrogen industry in an effort to reduce the substantial carbon emissions associated with existing hydrogen production facilities and to encourage the production of hydrogen in new areas, By Hilary Lefko and Viktoria Vozarova, Norton Rose Fulbright.

First, the US Department of Energy introduced Hydrogen Shot, a programme seeking to reduce the cost of clean hydrogen to US$1 per one kilogram within 10 years, which would represent an 80% reduction in costs.1 Next, in November of 2021, President Biden signed the Bipartisan Infrastructure Law, which included US$9.5bn of funding for hydrogen.

Subsequently, less than a year later, the Inflation Reduction Act (IRA) was enacted. The IRA contains additional hydrogen incentives to help meet the cost reduction goals of Hydrogen Shot. The IRA introduced new Section 45V, a production tax credit for clean hydrogen (45V), and also extended eligibility of qualified property under the Section 48 investment tax credit (ITC) to hydrogen production facilities. The 45V credit is equal to a specified dollar value per kilogram of hydrogen produced, whereas the ITC offers a tax credit equal to a specified fraction of capital expenses. This article explores the mechanics of 45V credit and the ITC as it relates to hydrogen facilities.

Hydrogen production

There are multiple ways of producing hydrogen, and hydrogen production is generally discussed in terms of colours: green hydrogen being the gold standard for clean hydrogen production; blue hydrogen, which is generally produced from steam reformation of natural gas and generally creates carbon dioxide, which means some think of it as it less green than green hydrogen; grey hydrogen, black hydrogen, and brown hydrogen, which are generally produced by refineries or from coal; yellow hydrogen, which is green hydrogen fuelled by solar power; pink hydrogen, which is green hydrogen powered by nuclear power; turquoise hydrogen, which is still in nascent stages and is intended to make blue hydrogen greener by removing the need for carbon capture; and finally, white hydrogen and gold hydrogen, which are generally produced by fracking.

Primary methods for producing cleaner hydrogen are using electrolysis and water and renewable electricity as feedstocks, ie green hydrogen, and using natural gas as a feedstock with carbon capture equipment, ie blue hydrogen. Electrolysis involves the use of electricity to split water molecules into hydrogen and oxygen. While this method does not produce direct greenhouse gas emissions, the large amounts of electricity required for production can lead to high life-cycle emissions and significant costs due to the purchase of electricity. Electrolysis also requires a significant amount of water. The production of blue hydrogen using natural gas uses a series of chemical reactions to release the hydrogen. With blue hydrogen, the remaining carbon atoms are usually released as carbon dioxide and captured using carbon capture equipment.

In order to qualify for a full credit, a facility must emit less than 0.45 kilograms of CO2 equivalent per kilogram of hydrogen produced. As such, a blue hydrogen facility must capture about 95% of its emissions for the full tax break, a rate only few facilities can currently achieve. The production of clean hydrogen has historically been expensive and not competitive, rendering it not very economically viable. The clean hydrogen credit under Section 45V is expected to change this and aims at lowering emissions from carbon-intensive sectors such as aviation, trucking, fertiliser production, shipping, chemical manufacturing, and steelmaking.

Mechanics of the 45V credit

The 45V credit is available for a 10-year period starting from the date when the qualifying clean hydrogen facility is placed in service.2 The tax credit is structured in four tiers and is determined by multiplying US$33 per kilogram (kg) of qualified clean hydrogen produced by an applicable percentage based on the resulting lifecycle greenhouse gas (GHG) emissions rate.4

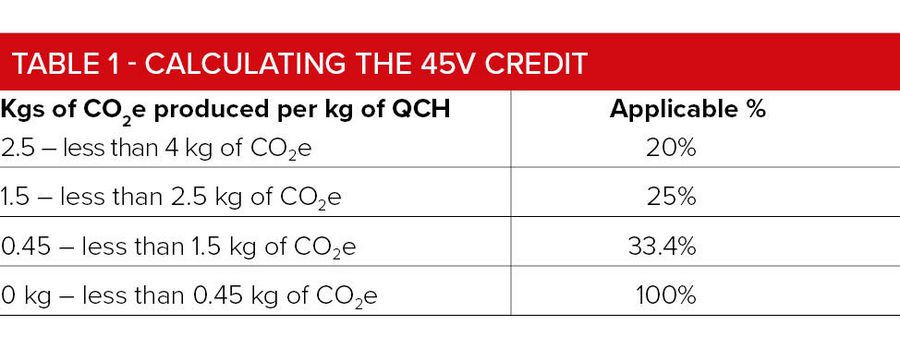

Calculating the amount of the 45V credit

The applicable percentage of the credit is tied to the amount of CO2e emitted during the production. See Table 1 for the breakdown.

Lifecycle greenhouse gas emissions as defined in the IRA refer to the total amount of GHG emissions, including direct emissions and significant indirect emissions such as emissions resulting from land use changes. The determination of these emissions includes fuel and feedstock production. The mass values of all greenhouse gases are adjusted to account for their potential contributions to global warming. Furthermore, the term "lifecycle greenhouse gas emissions" only includes the well-to-gate GHG emissions of hydrogen projects, as determined using the most recent GREET model developed by Argonne National Laboratory, or any successor model.5

After applying an applicable amount, the 45V credit can be multiplied by five if a project satisfies one of the following:

* The construction of the qualified clean hydrogen facility begins prior to January 29 20236, or

* The prevailing wage requirements and apprenticeship requirements as set out in the IRA are satisfied with respect to the construction, alteration or repair of the qualified clean hydrogen facility in question (through to the end of the PTC 10-year period).7

To illustrate, we look at a qualified hydrogen facility that began construction before January 29 2023 and that produces 2.0 kg of CO2e lifecycle greenhouse gas emissions for each kg of hydrogen produced. The taxpayer produces and sells 100,000 kg of hydrogen during the 2023 taxable year. If the taxpayer meets all requirements to qualify for the 45V credit, the tax credit for 2023 is US$3.00 x 100,000 x 25% = US$75,000.

For a facility to constitute a "qualified clean hydrogen production facility" eligible for the clean hydrogen credit, it must meet certain requirements. First, the facility must be under construction before January 1 2033 and be owned by the taxpayer seeking the credit. Additionally, the facility must produce "qualified clean hydrogen", which is hydrogen produced through a process that results in a lifecycle greenhouse gas emissions rate not greater than four kilograms of CO2e per kilogram of hydrogen.8

Further, to be eligible for the 45V credit, the qualified clean hydrogen must also be produced in the US by the taxpayer in its ordinary course of business for sale or use, and the quantity must be verified by an unrelated third party.9 However, the clean hydrogen credit is not available for qualified clean hydrogen produced at a hydrogen facility that includes carbon capture equipment if anyone claimed carbon capture tax credits under Section 45Q in any current or prior taxable year. This means that the 45V credit and the carbon capture credit under Section 45Q are difficult to stack where Section 45Q credits are available.10

Moreover, when tax-exempt bonds are used to finance a clean hydrogen facility, the 45V credit is reduced.11 The reduction is the 45V credit multiplied by the lesser of 15% or the reduction fraction.12 The reduction fraction is calculated by adding up the tax-exempt financing used and dividing by the total amount of money spent on the project.13 The reduction amount is determined as of the close of the year the project is placed in service.

Waiting for guidance

While there are a number of projects seemingly moving forward and obtaining financing, there are questions that the hydrogen market needs answered about the tax incentives before projects will really start to move forward. To name a few of these questions: the definition of the “qualified clean hydrogen production facility”, how the credit will be determined, the eligibility of blue hydrogen processes that produce a syngas that is less than 100% pure hydrogen – ie, how is the credit determined for anything less than pure hydrogen, and for grid-connected projects, the renewable electricity used with the hydrogen output in cases where the hydrogen producer uses grid electricity but buys renewable energy credits to offset the direct grid emissions.

The IRS invited comments in Notice 2022-58 on the clean fuel production credit. Even though, the deadline for written comments has passed, the IRS will still consider comments up until the guidance is issued. The www.regulations.gov inbox is still being monitored, and taxpayers are being encouraged to continue submitting comments. The IRS, Treasury, and Department of Energy have been meeting with taxpayers and trade associations to understand the needs of the industry. The Treasury Secretary is required to issue regulations or other guidance on 45V no later than August 16 2023 – including regulations or other guidance on determining lifecycle greenhouse gas emissions.

Direct pay and transferability rules

The IRA also introduced the ability to claim the value of the 45V tax credit through a tax refund, known as direct pay.14 Such an option is available for five consecutive tax years beginning after 2022. The direct payments will not continue beyond 2032. Under this option, a taxpayer is eligible to receive a direct payment for any amount paid in excess of its tax liability for the clean hydrogen credits. For most credits, direct pay is only available for tax-exempt entities but in the case of the 45V credit, it is also available for five tax years for privately-owned projects.

Further, under the IRA, hydrogen-related credits are also eligible, in the alternative, for transferability. Transferability allows taxpayers to sell all or part of their tax credits to an unrelated party15. Starting in 202316, companies with taxable income can sell clean hydrogen credits for cash to unrelated parties.17 However, tax-exempt entities are not eligible to sell their credits. A taxpayer can elect direct pay for the first five years of the credit period and transferability for the remaining credit period.

Section 48 ITC for clean hydrogen

In addition to the 45V credit, the IRA also gives an option of claiming an ITC for clean hydrogen by allowing taxpayers to treat clean hydrogen production facilities as energy property under Section 48.18 Taxpayers can make irrevocable elections to choose the ITC in lieu of 45V credits as long as they have not claimed 45Q credits for carbon sequestration. The ITC follows similar rules as for the 45V credit with regards to the reduced amount for tax-exempt bonds.

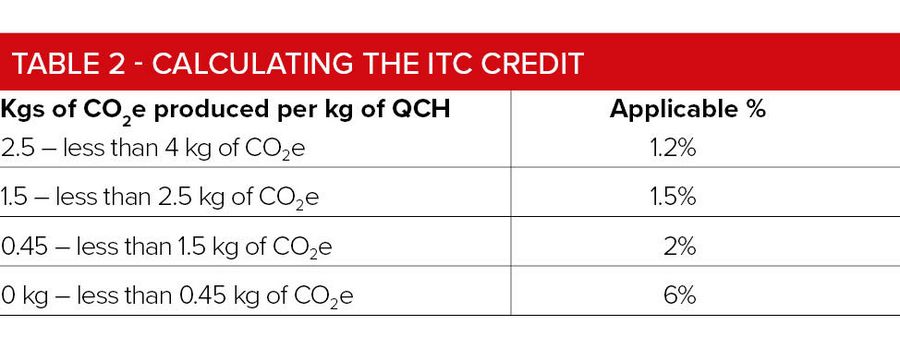

The four-tiered incentive in any taxable year is equal to the energy percentage of the cost basis of each specified clean hydrogen production facility placed in service during such taxable year. See Table 2 for the applicable percentages.19

The amount of the credit is multiplied by five in the event (1) the construction of the energy project begins before January 29 2023, or (2) the prevailing wage and apprenticeship requirements are satisfied.20 Additionally, an unrelated third party needs to verify that the hydrogen facility produces hydrogen through a process that results in lifecycle greenhouse gas emissions that it claims.21

The hydrogen energy projects are also eligible for a 2% or 10% increase, depending on whether the prevailing wage and apprenticeship requirements are met, for meeting domestic content requirements and for a 2% or 10% increase for being located in an energy community.22

To illustrate the calculation of the ITC, we consider a similar scenario as under the 45V credit. Suppose a qualified hydrogen facility that began construction before January 29 2023 produces 2.0 kg of CO2e of lifecycle greenhouse gas emissions for each kg of hydrogen produced and has a cost basis of US$70m. If the taxpayer meets all other requirements to qualify for the ITC, the ITC for 2023 is US$70,000,000 x 7.5% (1.5% x 5) = US$5,250,000. Whether to choose the ITC or the 45V credit will require weighing the cost to build the project against its efficiency in producing hydrogen. The more expensive the plant, the better an ITC looks. The more efficient the plant, the better 45V looks.

Lastly, similar to the 45V credit, the ITC is also eligible for direct payments, but only for projects owned by tax-exempt and state or local government entities, the Tennessee Valley Authority, rural electric coops or Indian tribes. The transferability regime, on the other hand, is only available to privately-owned projects.

Going forward

Facilities that produce green hydrogen can benefit from either an ITC or 45V credits. The future of blue hydrogen facilities and their potential eligibility remain contingent on guidance to be issued by the Treasury because of uncertainty over whether tax credits can be claimed where production of hydrogen is only an intermediate chemical step in a process to produce a different end-product. Nevertheless, the clean hydrogen incentives in the IRA represent a commendable initial effort towards promoting production of clean hydrogen. In anticipation for the Treasury's forthcoming guidance, the supply of clean hydrogen should grow, provided there is enough demand to justify the output.

Footnotes

1 - US Department of Energy, Hydrogen Shot, Office of Energy Efficiency & Renewable Energy, accessed on March 10 2023. The Hydrogen Shot establishes a framework and foundation for clean hydrogen deployment in the American Jobs Plan, which includes support for demonstration projects.

2 - See § 45V

3 - US$3 per kg is available for projects that meet prevailing wage and apprenticeship requirements, as explained in more detail below, or if the requirement does not apply. For all the other projects, the amount is US$0.60 per kg.

4 - § 45V(b)(1)-(2)

5 - § 45V(c)(1)(B)

6 - § 45V(e)(2)(A)

7 - § 45V(e)(2)(B)

8 - § 45V(c)(3)

9 - § 45V(c)(2)(B)

10 - § 45(d)(2). In the case of a facility that qualifies for multiple tax credits the cannot be stacked, Treasury or the IRS will need to issue guidance allowing taxpayers to choose the credit the taxpayer wishes to claim.

11 - § 45V(d)(3)

12 - § 45(b)(3)

13 - See id.

14 -See § 6417.

15 - As defined under § 267(b) and § 707(b)(1).

16 - §13801(g) of the IRA provides that § 6418 applies to taxable years beginning after December 31, 2022.

17 - §6418(b)

18 - § 48(a)(15)(A)

19 - § 48(a)(15)(A)(ii)

20 - § 48(a)(9)(B)

21 - § 48(a)(15)(C)(II)

22 - § 48(a)(12)

To see the digital version of this report, please click here.

To purchase printed copies or a PDF of this report, please email leonie.welss@lseg.com