A highly anticipated piece of the Inflation Reduction Act introduces optionality to US tax equity, a critical investor base that has provided about a third of the capital for US renewable projects over the past 15 years. Previously restricted to a project’s legal owners, credit transferability is set to expand the investor base and further accelerate the transition. Joti Mangat reports.

Taxpayers are arguably the most important driver of renewable energy deployment in the US, given their ability to monetise a pair of George W Bush era federal tax credits – the IRC Section 48 Investment Tax Credit and Section 45 Production Tax Credit – as well as depreciation benefits through legal ownership of qualified real property. Typically, tax equity investors contribute 30% to 40% of project costs (or more for wind projects) via contributions to a special purpose vehicle (SPV) to acquire an asset, post-construction and prior to commercial operation. These investors are a Colossus astride the cashflow waterfall and subordinate all other claims during the five-year credit recapture period with first dibs on all cash coming on.

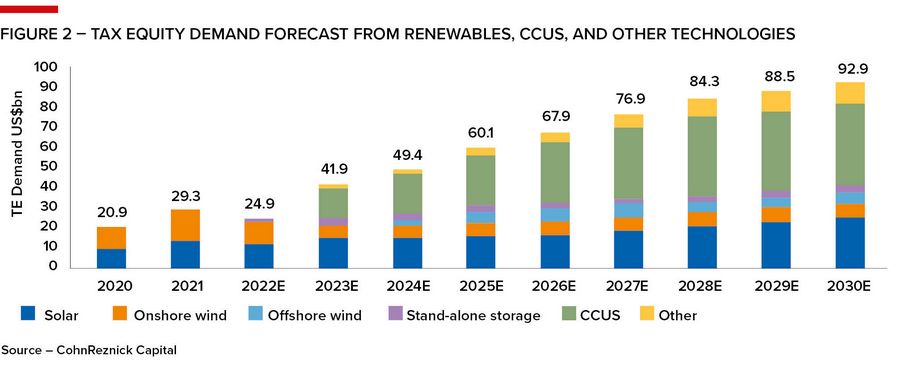

According to proprietary data from investment bank CohnReznick Capital, tax equity investors provided US$20.9bn of project capital in 2020, rising to US$29.3bn in 2021. The bank estimates that annual volumes will need to triple to some US$93bn by 2030 to fund the renewable capacity envisioned by the Biden Administration’s energy planners. Is there even sufficient qualified tax appetite available to meet this challenge? The clean energy components of the IRA are designed to find as many outlets as possible, as fast as possible.

Taken in the context of total individual and corporate tax receipts of US$307bn in 2023, according to the US Treasury, the critical importance of fiscal policy to the US energy transition is clear. Indeed, the existing regime, which has spawned a generation of specialty financial, legal and accounting businesses has crowded out all but the largest, most bankable deals. With participation limited to a shortlist of US taxpayers with sufficient risk appetite, operational sophistication and passive income tax liability, ie "Too Big to Fail" banks, tax equity supply has historically undershot demand from project developers.

Hate the game, not the players

Consultants providing US tax equity-related services have enabled hundreds of gigawatts of renewable capacity, solar 120GW, wind 135GW, over the past 15 years, making the most of financially awkward federal tax code provisions.

“Given the legal framework. tax equity structures can be very complicated, tedious, inflexible, and fickle. But if you were able – and, more importantly, willing – to develop and apply the expertise, you were in a relatively small group … who enjoyed the commensurate opportunity and earning-power tailwinds that come with being a scarce, important resource,” David Riester, founder and managing partner of San Francisco-based investment firm Segue Sustainable Infrastructure, wrote in a recent note titled The End of Tax Equity as You Know It.

“But boy did these structures slow the rate of solar and wind penetration. Not only that, they introduced 'rents' [in the economic sense] in the form of legal, accounting, and consultant bills, as well as 'leakage' of cash to the tax investor that they don’t really pay for,” he quipped.

In the Inflation Reduction Act's (IRA's) novel transferability provision, developers now have for the first time the option of a straight sale of either the ITC or the PTC to a third party, or parties, as an alternative method for monetising incentive value. Effective as law on August 16, public consultation on rule making around transferability closed on November 3 with final rules still pending at the time of writing.

Key questions for participants and service providers focus on the specific approvals and disclosures required for transfer transactions, as well as the responsibilities of both transferer and transferee post-sale. Credit recapture, if a commercially active project is taken out of service, remains a key risk. The developer audience, and its service providers, eagerly await final rules on a rare piece of innovation from the IRS, which typically builds policy reform on the foundations of existing tax law.

Jorge Medina, tax attorney and partner at Pillsbury Winthrop Shaw and Pittman, is excited by the potential for new entrants but says it’s too early to say exactly how the new provision will shake out.

“The ability to sell tax credits to a third party has never really existed in the tax code, so this is very new and as a rule the IRS does not like to innovate. There’s not much precedent to refer to, which is unusual. For example, when the Act says ‘the transferee taxpayer will be deemed the taxpayer for all purposes’, what is that intended to mean? We think we know what it could mean, but on the margins there could well be room for credit limitations or risk allocations that are not immediately clear,” he says.

Nonetheless, Medina notes the level of excitement in the professional services sector for a new source of potentially disruptive capital in the market, and the opportunity to bring new taxpayers into deals that probably wouldn’t have happened under the previous regime.

“Folks are already looking at and starting to plan how to do transfer transactions. New companies are starting to emerge that are looking to serve as central databases for transferability or to help with diligence work to bring more participants into the market. The renewable market is already planning to be getting into this heavily,” he says.

Seniority re-booted

Anticipation for a previously untapped source of credit monetisation, and therefore project leverage, is palpable at both the unit and enterprise levels, with transferability broadly expected to stimulate growth, particularly for distributed generation and a smaller utility-scale market where bankability and closing cost budgets are hard limiting factors.

By removing tax equity from a deal, senior lenders are no longer subordinated to tax interests in the project cashflow waterfall. Traditionally, most solar and wind project financings are back-leveraged, meaning that Cash Flow Available For Distribution (CFADS) to non-tax investors is subordinate to the tax investor's preferred cash.

Tax equity’s dominance of the capital structure has brought a range of risk management features including SNDAs, inter-creditor agreements, cash-traps and buyouts at the expense of other senior lenders and cash equity sponsors. Sans tax equity, developers can now enjoy simpler, front-leveraged transactions with improved seniority, and less encumbered cashflows, other things being equal, should support more attractive interest rates, DSCRs and risk adjusted equity returns at the projectco level.

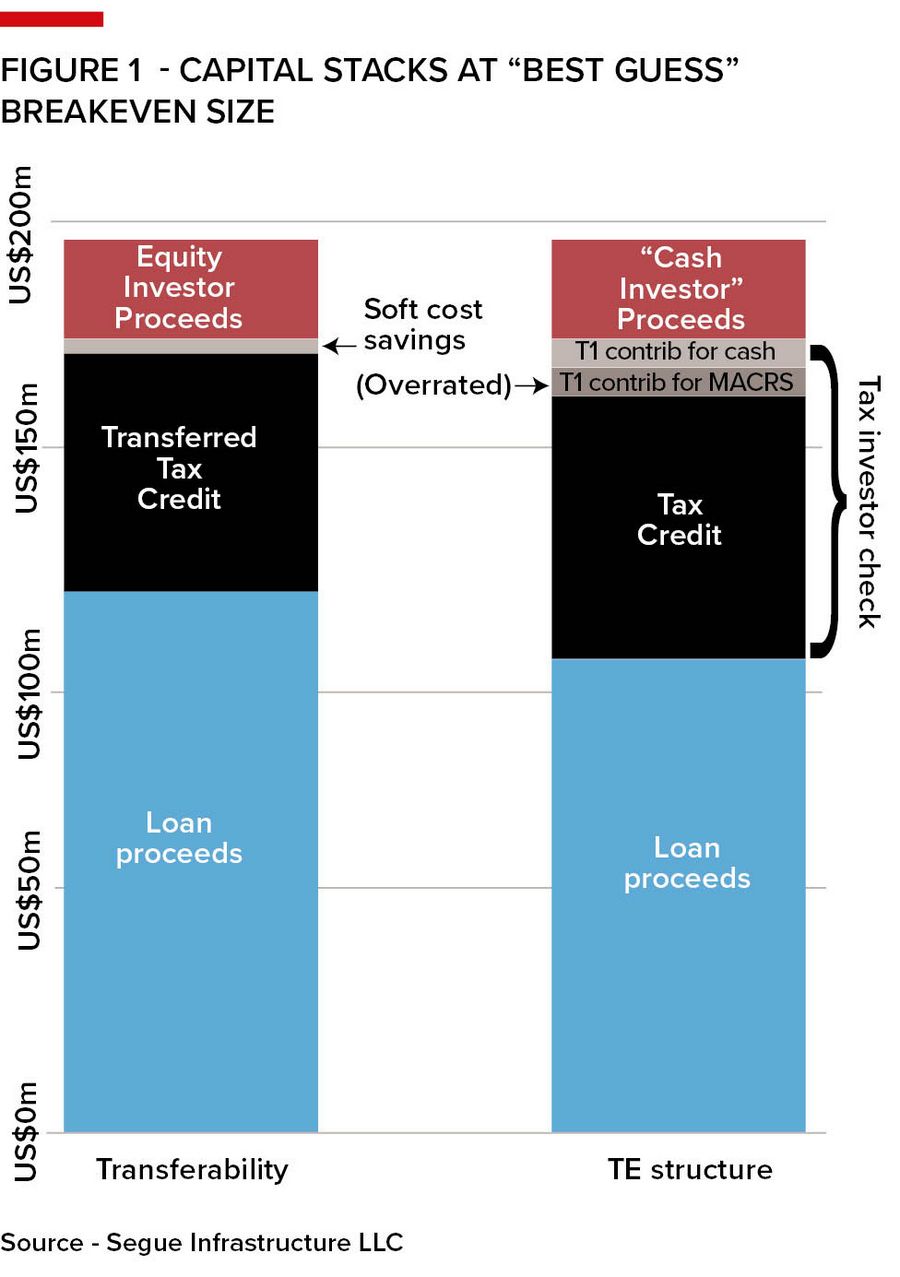

Although a transfer could achieve basic credit monetisation with less fuss and cost, a straight sale has several economic disadvantages that must be considered individually. First, transferees will require a significant discount to the credit’s face value to induce them to buy. The first cohort of transfer deals is likely to see greater discounts as investors build comfort with the new asset class and transaction process, while smaller developers and deals will come at relatively greater discounts to the extent they are perceived as riskier. Unlike traditional tax equity structures that allocate both tax credits and accelerated/bonus depreciation benefits to taxpayers, transfer applies only to the credit itself and leaves depreciation on the table.

Furthermore, it’s not yet clear how ITC transfers will impact developers’ ability to generate profit through basis step-ups. In a typical tax equity transaction, a developer builds a project at "wholesale cost" on balance sheet, and then sells the asset to the tax equity partnership at a grossed-up price to establish a relatively higher cost basis for the purpose of tax credit optimisation. This elegant nuance of the US tax code allows developers to achieve margins of 20%–30% through a related party sale, replete with the full blessing of the IRS, subject to proof of cost eligibility. Clearly, a straight sale of ITC credits based on developers’ cost-to-build alone negates the basis step-up and associated profit opportunity.

Segue’s Riester argues that if the elimination of tax equity from the seniority waterfall can reduce the project’s weighted average cost of capital (WACC) by 40bp–60bp or more, a credit transfer could potentially offset the innate discount, as well as lost depreciation and basis step-up. Although his conclusion rests on key assumptions about the willingness of creditors and investors to improve terms, and the range of discounts likely to emerge in the transfer market, the argument that combined WACC improvements and significant soft cost savings will make the transfer option worthy of serious consideration in solar transaction sizes under 200MW is compelling.

With more than US$15bn of tax equity invested in US solar and wind transactions, US Bank, through its US Bancorp Community Development (USBCDC) entity, is perhaps the leading tax equity player in the market. To-date, USBCDC has financed a total renewable generating capacity of 20.21GW, the equivalent of powering over 3.8m homes.

Jon Peeples, senior vice-president and business development director of Environment Finance with USBCDC, agrees that transferability is potentially a transformative concept for the renewable project finance market, with the caveat that details on the transfer mechanism for now remain uncertain.

“Many aspects with respect to transferability remain to be seen, but the additional options that transferability provides could incentivise some sponsors to consider forgoing tax equity entirely on the premise they can find a buyer for credits at a later date. Guidance for how one can transfer a credit will be very important in the ongoing analysis of traditional tax equity versus a sponsor transfer,’” he says.

Indeed, USBCDC is actively evaluating the transfer regime as a way to expand the investor audience for its renewable energy deals.

“Through our syndications platform, we’ve had great success bringing new, non-traditional investors and more capital to support projects in this sector, and we believe that transferability has the potential to help us continue to expand our efforts to support renewable energy projects and deliver greater impact,” Peeples says.

“Without transferability (and again subject to guidance), if an investor wants to participate in a tax equity investment it needs to be in a partnership, and with all the legal and accounting analysis that comes with that. US Bank intends to continue offering investors the ability to invest alongside us, but we also intend to offer investors a chance to buy credits transferred out of a partnership that US Bank has already invested in. How material transfer becomes versus direct investing remains to be seen,” he says.

Production advantage

With the IRA providing an improved USS0.0275/kWh 10-year production tax credit for wind, solar, geothermal and closed-loop biomass projects placed in service after January 1 2023, Pillsbury’s Medina notes that PTC deals may be relatively more attractive candidates for the transfer approach than cost basis-intensive ITC deals. PTC eligibility is determined by a projects’ verified electricity production, rather than cost-basis, and as such offers an even simpler legal route to monetisation.

“PTC is slightly less complicated and disruptive than ITC with respect to the existing economics of a tax equity transaction. In a PTC transaction a developer can build a facility on balance sheet and sell transferable tax credits as soon as it’s generating commercial power and the basis to build the project is irrelevant,” Medina says.

“For most investors, if they could just buy a credit and earn a yield that is competitive with a tax equity fund, most would prefer to do that. Most tax equity investors don’t take the depreciation benefits associated with the asset and use tax credits to finance further project transactions. Developers may want to keep tax equity investors in a structure in order to monetise depreciation, as most developers do not have the tax capacity to use depreciation,” he adds.

A blended approach with sponsors combining ITC/PTC credit transfer with traditional tax equity structural components to monetise depreciation benefits, especially for deals below the 200MW mark, could well emerge. Indeed, sponsors and investors embraced hybrid structures during the Section 1603 cash grant era, 2009–2011, when the government made direct payments to sponsors to offset the cost of building qualifying projects under the Obama administration’s Recovery Act of 2009. Before its termination, Section 1603 grants contributed US$26bn across more than 100,000 projects equivalent to 8.5 million homes in payments ranging from hundreds to hundreds of millions of dollars, according to the US Treasury.

“As with the 1603 vintage of deals, we are likely to see a blending of financial tools to provide flexibility to developers that have been priced out by the largest players. For example, a smaller solar deal could involve a tax equity partner to monetise depreciation, combined with a credit transfer to a third party. Depending on how the rules around selling to a related party shake out, this blend could be used to both monetise depreciation and achieve basis step-up by selling into a new partnership,” Medina says.

While we wait for more detailed guidance from the IRS on the transfer process, specifically what information is required and which parties are on the audit/recapture hook, the broader significance of transferability will be felt to the extent that it can equalises the financial power of non-tax equity investors in the capital structure.

Although tax equity investors have driven US renewable penetration to date, sponsor access has been limited and exclusive. Indeed, with appetite for development risk and availability of construction financing both entirely dependent on the take-out financing function provided by tax equity partnerships, many smaller projects with clear value propositions never progress beyond feasibility.

“Transferability will allow the renewable energy and energy storage industries to reach a velocity not yet experienced. For most projects, transferability will lead to margin expansion, and even where a full TE structure still makes sense, the transferability option will embolden developers and their investors in ways that go far beyond project profitability,” Riester concludes.

To see the digital version of this report, please click here

To purchase printed copies or a PDF of this report, please email leonie.welss@lseg.com