Finergreen discusses the current situation and future outlook of merchant financing of renewable energy projects in Iberia, which, given the high wholesale electricity prices in the region, has become an increasingly relevant topic for sponsors bringing their projects into operation and having to decide on an offtake strategy in the context of construction financing and an environment of increased capex. By Juan José Pérez Fernández CFA, associate, Finergreen Southern Europe.

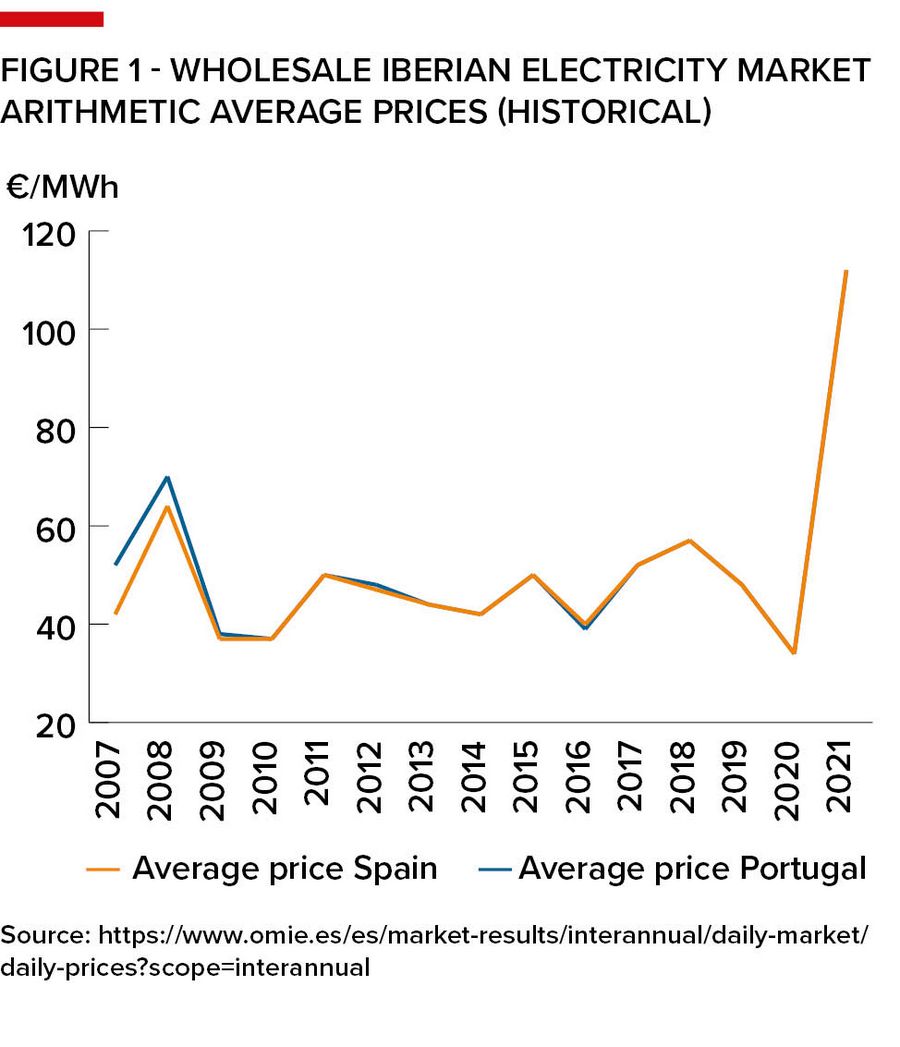

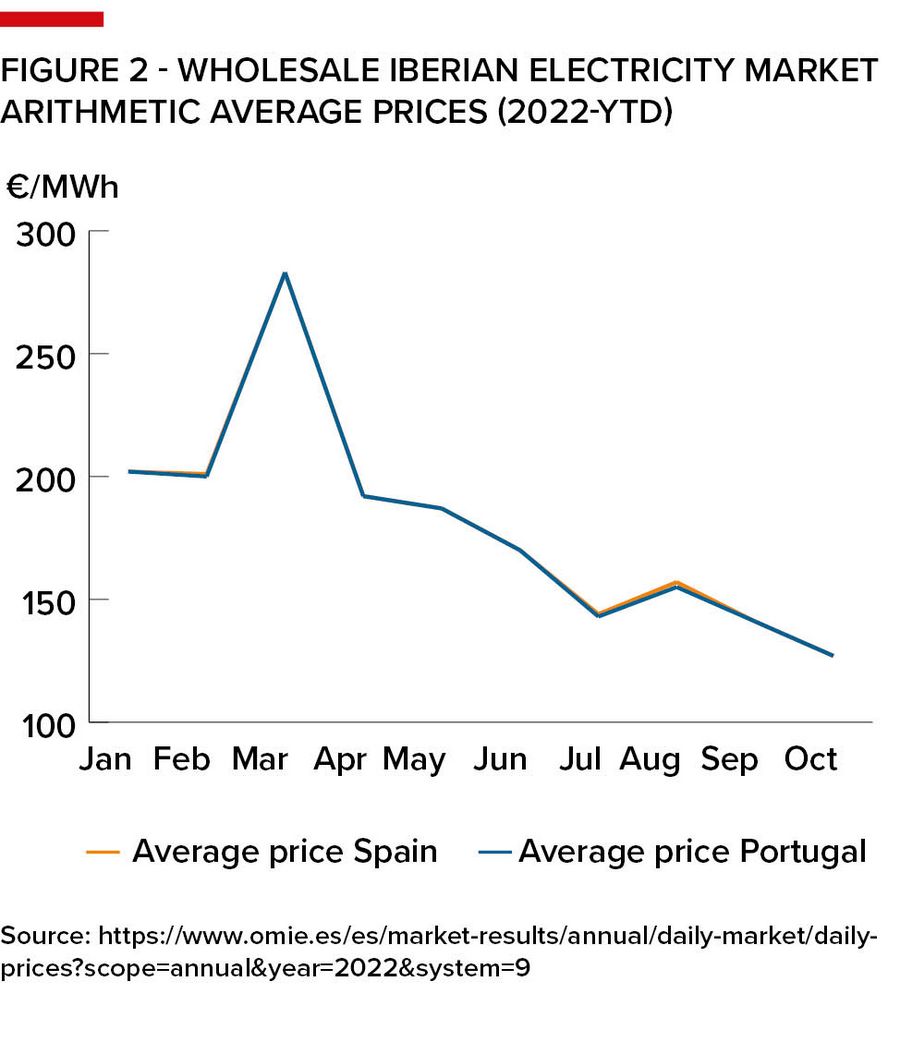

The Iberian wholesale electricity market has been dominated by higher-than-usual prices for the last two years. In the last decade, the average yearly wholesale market for Spain and Portugal had historically ranged between circa €40/MWh and €60/MWh, compared with an average price of circa €112/MWh in 2021 and €180/MWh over the course of 2022 until October.

This upward pressure on electricity prices has mostly been driven by a recent surge in commodities, gas and coal, and carbon prices, which are expected to continue at least in the short to medium term. Typically, gas-fired generation has dominated wholesale electricity prices, given the marginal price-setting mechanism of the European electricity market.

* Gas prices – The already-increasing European gas prices in the context of lower-than-usual Russian gas supply during late 2021 reached record levels in August 2022 €229/MWh1, following the indefinite stop of Nordstream 1 and heavy maintenance works on the Norwegian Continental Shelf.

* Coal prices – In 2021, a sharp increase in coal prices had been driven by increased coal demand and generation across Europe as coal plants’ competitiveness against gas plants improved due to higher gas generation costs. In August 2022, the EU banned Russian coal imports, which together with the limitations of non-Russian producers and stronger demand have further increased the pressure on prices. Coal prices averaged US$341.8/tonne in September 20222, a 94% increase on a yearly basis.

* Carbon prices – Carbon prices have also seen an increase in recent months, due to rising demand for coal-fired generation as well as an expectation that decarbonisation efforts would involve strengthening the European emissions markets. Most recently, these prices have been dropping, due to fears of a recession and the anticipation of EU action on the Emissions Trading System (ETS) to ease pressure on winter 2022/23 power prices. Carbon prices dropped to €70.8/tCO2 in September 2022, a 19% monthly decline3.

Despite numerous EU-level and country-level aid mechanisms put in place recently (short-term gas prices in the Iberian region are affected by the gas price cap for fossil fuel generators bidding into the market), the market sentiment is that Iberian wholesale electricity prices will remain above usual prices in the medium run. Future contracts traded on OMIP and EEX for baseload profiles show the following in Table 1.

Taking all of the above into consideration, the futures market for electricity in Iberia is still perceived as having low depth. A common discussion that we see in the market is that these prices are more a reflection of the "cost to hedge", rather than a consensus market view on the forecast price, where a desire to procure demand at a reasonable price is over-weighted vs the need to secure a selling price. This argument is reinforced by the fact that the average consensus view on the forecast price by bankable market advisers under their reference/base case scenario is more in the range of €280/MWh in 2023, €205/MWh in 2024 and €140/MWh in 2025, as of October 2022.

Offtake vs market

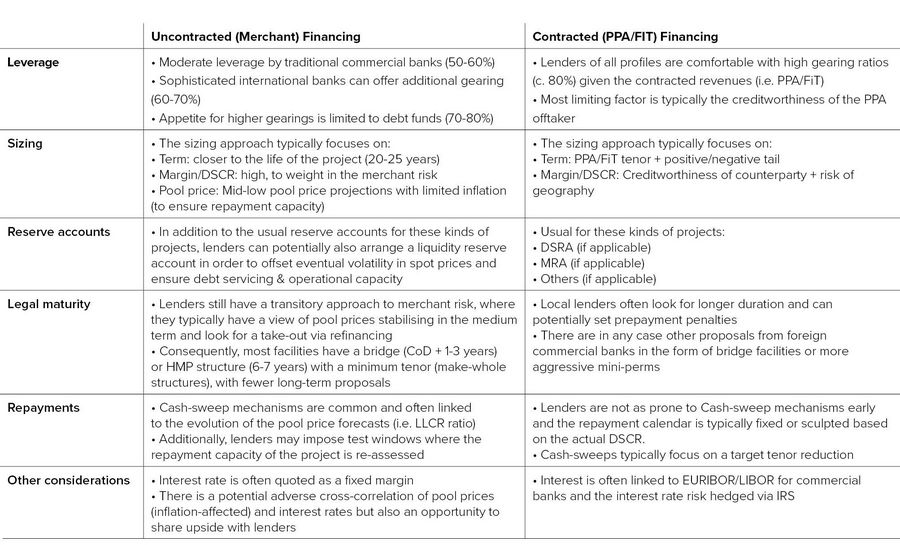

In this environment of volatile wholesale market prices, the offtake strategy decision for sponsors of renewable generation projects with a focus on solar PV and onshore wind plays a crucial role now more than ever before, more so in the context of construction financing, which many sponsors are facing. The typical two offtake approaches seen in the market have historically been: i) to hedge partially or totally future capture prices by securing a power purchase agreement (PPA) for a relevant fraction of the project production and operational life; and ii) to sell electricity completely in the wholesale market, also referred to as merchant. In the last year, there have also been growing moves from investors to adopt a blended approach that sits between fully merchant and fully contracted revenues, with the desire to balance the trade-offs of both.

PPAs have traditionally been the preferred option for many sponsors and lenders, particularly in the context of financings, before merchant financing became a reality. Total PPA announcements in Iberia covered circa 6.6GW in the last 18 months, where Solar PV represented circa 52% of the deals by capacity vs 48% for onshore wind. The most common tenor is 6 to 10 years, covering 4.4GW of the total negotiated capacity. PPAs remain an attractive strategy for sponsors in Iberia, particularly the more sophisticated ones with offtaker sourcing and structuring capacity.4

Higher discounts on longer-dated PPA contracts are pushing sponsors to shorter terms, up to five years, and baseload types of PPAs, to manage the higher uncertainty of renewable revenues under such hedging arrangements.

The largest driver for fair price assessment in PPAs is the development of technology-specific capture prices. In addition, guarantees of origin are also priced into the PPA as well as the optionality effect of the PPA, which reflects the capital at risk and volatility of low and high price scenarios, yet the current wholesale environment generates mispricings and leads to difficulty in reaching agreements between seller and buyers.

PPA negotiations can create further complications, particularly for smaller and/or less sophisticated sponsors, for which developing and building a project is already a large challenge. In addition to finding and negotiating terms with a counterparty, a series of risks need to be considered in PPAs: i) volume/profile/wholesale price risk, ii) counterparty risk; and iii) construction and other operational risks, ie non-performance of the PPA obligations. Additionally, it should be noted that PPA offtakers often require relevant guarantees from the sponsors to the offtakers – more so when wholesale prices increase, as these intend to cover potential supply shortages to procure in the open market.

In Finergreen’s view, sponsors for about a half of the potential new capacity hold aspirations of keeping their projects largely or entirely merchant, at least for the initial years of operation, either selling output directly to the market or under short-term hedging contracts. These highly merchant-focused strategies are also exposed to other risks, such as volatility in wholesale prices and cannibalisation of captured prices. Technology-specific capture prices should decrease as renewable generation grows, particularly for solar PV, given the load profile concentrated in specific hours of the day.

The level of cannibalisation for each technology increases as a result of additional renewable generation throughout the forecast. This is most prominent for solar assets, which are expected to reach an average discount to baseload of 36% in the decade of the 2050s5, due to the high correlation in their production patterns across the peninsula. Sponsors therefore want to capture as much upside as possible before a projected drop in wholesale prices later in the decade as greater volumes of renewables come online and erode capture prices – the so-called cannibalisation effect.

An additional risk of merchant strategies is the risk of future regulation mechanisms to limit the captured price. This is more relevant in the current market environment, since renewables, lignite and nuclear power plants have low marginal costs but are receiving the high market price set by gas-fired power plants.

EU member states are discussing €180/MWh market cap for individual technologies, which can lead to uncertainty for renewables investors and developers as their level of revenues for assets over the coming months are still subject to member state decisions and may differ by country. The cap only applies to realised market revenues, so power producers with existing PPA or futures contracts with a strike price of less than €180/MWh are unlikely to be affected. However, at best, it is likely to complicate merchant offtake decisions and potentially delay or prevent new PPA or future contracts from being concluded.

In any case, our market perception is that sponsors are becoming increasingly keen to limit the degree of hedging and become exposed to current market prices. This needs to also be considered in addition to the inflationary pressures on construction costs and raw material prices, which have also seen capex for utility-scale solar PV and onshore wind projects increasing in the region of 25%–30% since mid-2021.6

Merchant financing

On the basis of the increasing capex mentioned above, taking into consideration that not all sponsors have strong balance sheets, the need to procure debt financing for construction becomes more pertinent. Given that this increased capex also reduces profitability, it is more attractive for sponsors to be exposed to the short-term higher merchant prices, thus creating a natural need for merchant debt structures and associated financing.

The concept of merchant financing in Iberia is relatively new, having begun with some conservative, 50%–55% gearing, proposals from a very small selection of local banks, often pricing in a slightly higher margin. Until very recently it was perceived as a small and illiquid market, where ticket sizes could not be too large. Similarly, the way commercial local banks in Iberia look at these types of financings has not been significantly updated in the current wholesale price environment. More recently, other more sophisticated European lenders have offered terms for Iberian merchant financing that show more aggressive gearing (60%–65%) and structuring capacities.

Nonetheless, in the last 18 months, a new universe of alternative lenders – asset managers, institutional investors, credit funds, etc – has emerged, offering a new range of heterogeneous solutions that can be further extended and adapted to the needs of sponsors. These solutions are commonly referred to as unitranche financings.

Unitranche is a term commonly used to refer to a single-tranche facility that gears in a similar amount to junior plus senior debt with a blend of the usual margins/costs of debt of both types of facility. We currently see these alternative lenders offering gearing of about 70%–90% of total project costs, as opposed to the 50%–55% of local commercial banks and the 60%–65% of other selected European banks.

Pricing becomes an extremely tricky concept when discussing it within the context of current merchant financings. For commercial banks, facilities are typically priced at a fixed margin plus Euribor reference rate, which is hedged by a large percentage. On the margin front, we have seen some repricing by commercial banks, in the context of the current riskier environment – cost of funding, volatility of merchant, Ukraine concerns, etc.

However, the most competitive banking merchant proposal starts at circa 175bp and goes as high as 300bp, some of these with step-ups every circa five years. Given that Euribor has increased dramatically in the context of monetary policy increases in interest rates to combat inflation, the cost of hedging has increased by as much as 300bp for amortising facilities of up to 20 years in the last 18 months. The all-in margin of fully hedged long-term merchant bank facilities can reach circa 500bp–600bp today.

Regarding unitranche facilities provided by alternative lenders, which are often quoted on a fixed margin basis, during early 2021 we saw proposals that started at 4.5%–4.75% and could go as high as 6% or 6.5%. The interesting thing to be aware of here is that, depending on the profile of the lender, there might be more risk of repricing.

We see some asset managers or credit funds that have raised funds from third parties promising a specific return and therefore might not increase the terms that much, whereas others offer returns to their investors or separately managed accounts on the basis of mid-swaps + spread or other similar metrics, so they will effectively price in the current interest rate increases. Most competitive proposals in the last category typically stand at about 300bp + mid-swaps for what we have seen.

While most local commercial banks’ merchant proposals are long-term, other foreign lenders aim for an earlier takeout in the form of a bridge facility or a mini-perm, even being able to price in a lower margin or more aggressive sizing criteria. For unitranche financings, the typical approach is to offer a takeout in the medium term, three to seven years, where fewer proposals are long-term. In addition to this, typically a relevant level of cash sweep is required.

Future outlook

In Finergreen’s opinion, merchant financing in Iberia is a yet-developing topic. Regardless of the short-term situation in the wholesale electricity markets, we see a close future in which many merchant strategies will consist of a combination of sophisticated PPAs – ie, shorter-term, lower-than-usual amount of production hedged, tailor-made profiles, series of future contracts for short tenors, forward initiation of the PPA, etc – with a relevant amount of merchant-exposed production.

We see more and more European IPPs considering these kinds of strategies. In a way, the adoption speed will depend on the appetite of offtakers to secure demand under these kinds of instruments and the acceptance of ordinary lenders to finance such strategies under compelling terms. These kinds of arrangements will allow sponsors to be exposed to the upside in prices with downside protection and access financing in view of more certain cashflows.

Lender appetite for projects facing merchant exposure is also expected to continue increasing, with more commercial banks eventually accepting structured alternatives permitting sponsors to enter sophisticated PPAs as described above through alternative offerings that will adapt to the particularities of the market as it evolves.

Footnotes

1 - Benchmark TTF gas price on August 26 2022

2 - Monthly average of the daily API-2 front-month prices. Last updated on September 28 2022

3 - Based on Aurora Research. Monthly average of the daily EU ETS front-year, December 2022 prices. Last updated on September 28 2022

4 - Source, Aurora Energy Research

5 - Source, Aurora Energy Research

6 - Finergreen estimates

To see the digital version of this report, please click here

To purchase printed copies or a PDF of this report, please email leonie.welss@lseg.com