Wind turbine manufacturers may be facing another tough year. How long will headwinds persist in the wake of COP26 and how will this impact project prices in 2022? Arup’s James Theobalds, transaction director, Meltem Duran, senior offshore wind consultant and Amy Johnstone, renewable energy consultant, explore the factors affecting the outlook for the industry.

Orders are up, countries are setting ambitious targets, and long-term projections for market growth are encouraging. Why, then, are some of the leading manufacturers of wind turbines – including Vestas and Siemens Gamesa (SGRE) – warning investors of reduced earnings and challenging times ahead?

With wind turbines accounting for around 60% (including foundations) of the capex cost for developing offshore wind projects globally, the cost of offshore wind is affected by both long-term and short-term factors. Over the last 10 years the industry has managed to drive astonishing cost savings from a combination of technological development, industry cooperation, market competition and targeted support.

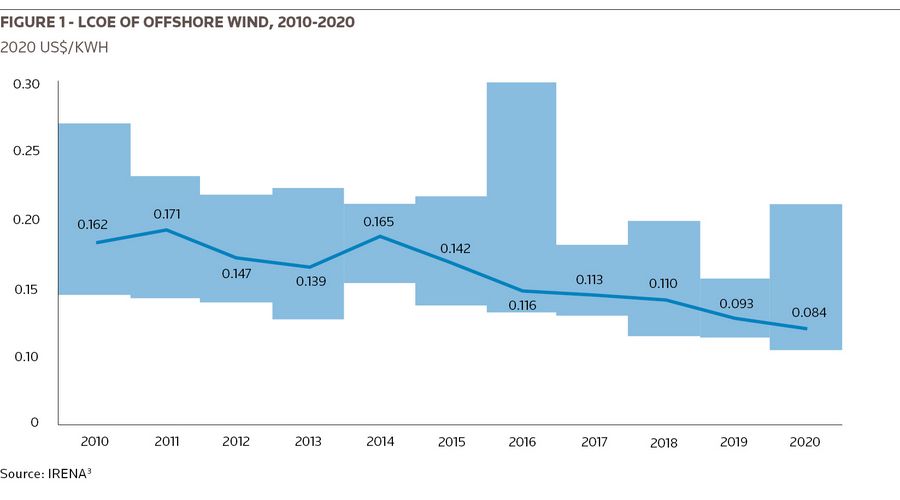

For example, the levelised cost of energy fell from around £140/MWh1 in 2011 to below £40/MWh in 20192 for projects with an expected life span of about 30 years. These trends have been driven by incredibly rapid advancements in technology, the introduction of competitive markets for support mechanisms, and targeted support from governments.

This article explores some of the factors feeding into this complex picture and considers how these factors may affect projects being delivered over the next few years. We have characterised headwinds that could make project delivery more difficult and projects more expensive to deliver, and tailwinds that are creating a more dynamic market and encouraging the growth of offshore wind.

Supply chain headwinds

* Covid-19 labour shortages and disruption caused some delays on projects in construction (such as Formosa 2 in Taiwan)4 but overall in 2020 the International Energy Agency reported relatively little disruption to projects already in construction or later stages of development. However, it did advise that some delays to site selection and permitting could have medium-term impacts.5 As well as these specific difficulties, the sector has been affected by widespread disruption to manufacturing and shipping, which may have a staggered impact on component manufacturing in the next few years.

There were some short-term impacts on availability of skilled personnel and equipment such as vessels when more stringent social-distancing rules were required. Overall, though, the impact of Covid on the delivery of projects has been well managed, and short-term increases in costs have been minimal.

* Raw commodity and logistics price surges have had a negative impact on earnings for some of the largest turbine manufacturers, including SGRE6 and Vestas7, in Q3 2021. Longer-term impacts will depend on future trends in commodity prices and what strategies companies employ to cope with high and volatile prices. Some of this cost is beginning to be passed through to developers. Dominion Energy recently cited commodity prices as one factor contributing to an increase in cost on the Coastal Virginia Offshore Wind project.8

Recent data from BNEF9 illustrate the impact of some of the key commodity price increases, including steel costs peaking at around 1.5x pre-pandemic levels. Historically, manufacturers have been relatively adept at hedging against these costs and limiting the extent to which they are passed through to customers.

Additionally, the BNEF data show that transport and logistics costs have increased significantly in the wake of Covid-19, with the price of 40-foot containers – to ship components from America to Asia, for example – increasing from a fairly consistent US$2,000 to over US$8,000. Analysis from McKinsey10 indicates that this increase is being driven not by an overall rise in the volume of materials transported but by a combination of the changing nature of materials transported, the impact of Covid-19 – particularly on ports – and one-off events, including the blockage of the Suez Canal in March.

It is not uncommon to see economic factors (including commodity prices) built into supply agreements for major component delivery. In fact, manufacturers increasingly pass through such costs. On some projects costs are starting to flow through and affect project contingency budgets, though these risks are typically well managed.

Elevated commodity pricing does not seem to be affecting assumptions for the development of future projects and, while the supply chain may take time to adjust to the effects of the pandemic, costs could return to more normal levels in time. In the context of developing an offshore wind project, which typically takes around 10 years, these risks are manageable. It is also important to note that other competing industries and the wider economy are similarly exposed to commodity price variation.

* Local content requirements are a growing challenge for offshore wind developers and the wider supply chain. This has been reflected in higher costs in countries such as Taiwan and France that take a more prescriptive approach to localising the supply chain. The rapid increase in shipping costs since July 202011 and the disruption caused by Covid-19 have fuelled conversations about how localisation could make supply chains more resilient, and the offshore wind industry is no exception.

However, manufacturing capabilities in many countries that are developing offshore wind are not yet a practical option for developers. Additionally, while some countries may be able to produce components locally, production of raw commodities is much more inflexible. For example, China is a key producer of steel used in wind farms worldwide. Ultimately, anything that affects raw commodities markets has a knock-on effect throughout the supply chain, and companies further up the chain must be able to cope with this.

Supply chain tailwinds

* Political support for offshore wind in existing and new markets was evident at COP26, with many countries setting new or more ambitious targets for building offshore wind capacity. However, it is the strategic actions governments are taking to support these targets that are perhaps the most positive sign for the industry. Government funding for emerging technologies such as floating wind12 will help the first generation of commercial projects get off the ground.

Meanwhile, the message from the industry is clear: government-led processes such as leasing and permitting need to be improved if projects are going to be delivered at the pace required. To help turn political will into effective action, the Energy Sector Management Assistance Program (ESMAP) has been supporting non-OECD countries to produce roadmaps for establishing an offshore wind industry that draw on lessons learnt from the results of different policies and frameworks.13

* Exportable expertise of experienced offshore wind developers has helped them partner with local companies in emerging markets and be successful in early auction processes around the world. International collaboration also offers ways of meeting the demand for local content in the supply chain that fit with other demands such as affordability and managing delivery risk.

Arup has looked at this balance in a report on Key Factors for Successful Development of Offshore Wind in Emerging Markets14, prepared in associated with BVG Associates for the World Bank. Following examples such as the collaboration between Century Wind Power (Taiwan) and Bladt Industries (Denmark) to manufacture offshore foundations in Taiwan, demand for local content can strengthen the supply chain and contribute to the successful build-up of offshore wind capacity globally. As well as developers and companies in the supply chain, policy and strategic expertise can also be exported. RVO, the Netherlands Enterprise Agency, has recognised international advisory work as a major growth opportunity for the next decade.15

* Technology and standardisation continue to drive cost savings, improve yield and prepare the industry for changes to the wider energy mix that will be required to meet net zero. The growth of offshore wind, in newer markets across Asia and America, and also in more established markets such as Europe and China, provides opportunities for economies of scale. The move that some developers are making from a project-based to a portfolio-based strategy will make it easier to predict demand throughout the supply chain.

While floating wind costs are currently high, developers such as Equinor predict that it will become cost-competitive by the end of the decade, and new developments in offshore transmission networks, battery storage and hydrogen multiply the options for using electricity generated from offshore wind. These developments provide a technical basis for ensuring that offshore wind projects remain bankable as more projects come online. Meanwhile, as turbines continue to grow and the depth of fixed foundations increases, we expect to see further reductions in the levelised cost of energy as new projects generate at higher powers and access areas with more favourable wind conditions.

Future projects

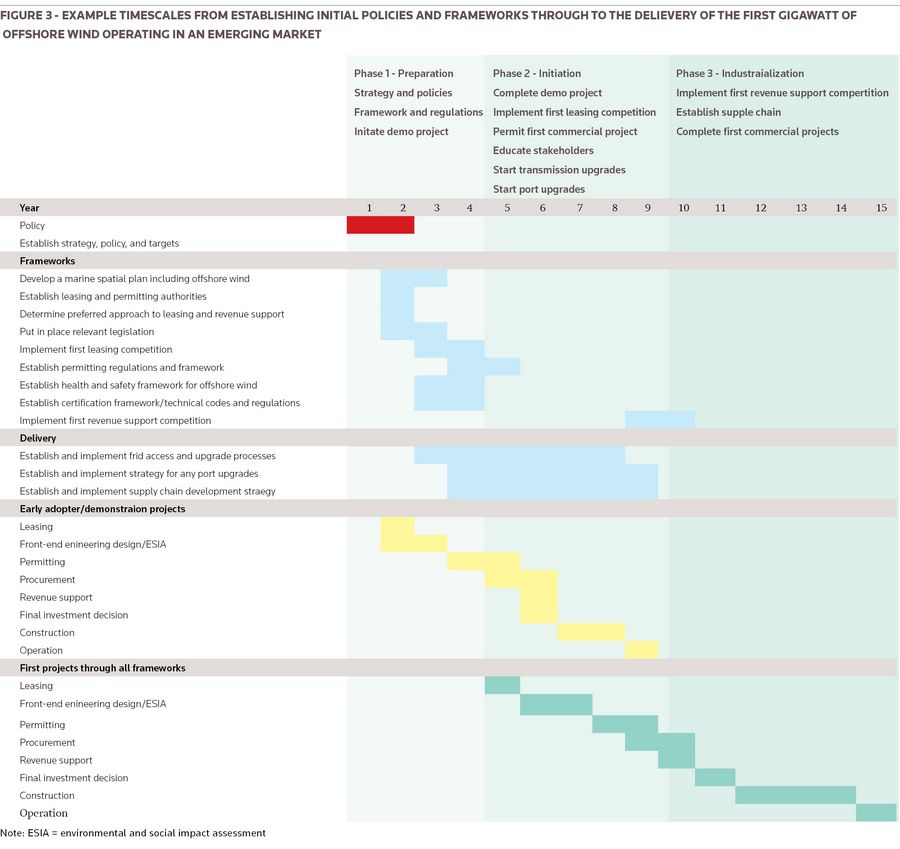

In most markets, developing an offshore wind project takes around 10 years – although this varies between markets and a number of countries are working on reducing it. This means that developers and industry need to take a long view on project economics.

The majority of factors increasing supply chain costs appear to be short-term – Covid-19, oil prices, supply chain constraints and commodity prices. How these factors flow through to projects depends on how the supply chain manages the risks commercially. Orders for large supply contracts typically have significant lead times. Contracts normally contain provisions for managing key delivery risks, such as commodity prices, to ensure that the parties that are best placed to manage risk can do so effectively.

For manufacture of relatively low-complexity components – monopiles, for example – the extent to which suppliers can manage factors such as commodity prices is very limited. As a result, these costs tend to be passed through. For manufacturers of complex assemblies with many components, it is often harder to separate out commodity costs. These manufacturers also manage significant value in their supply chains. This can leave them more exposed to factors such as Covid-19 and supply chain logistics.

While increased supply chain costs are being passed through to a limited extent on some projects, the industry is coping well with short-term factors that are expected to ease.

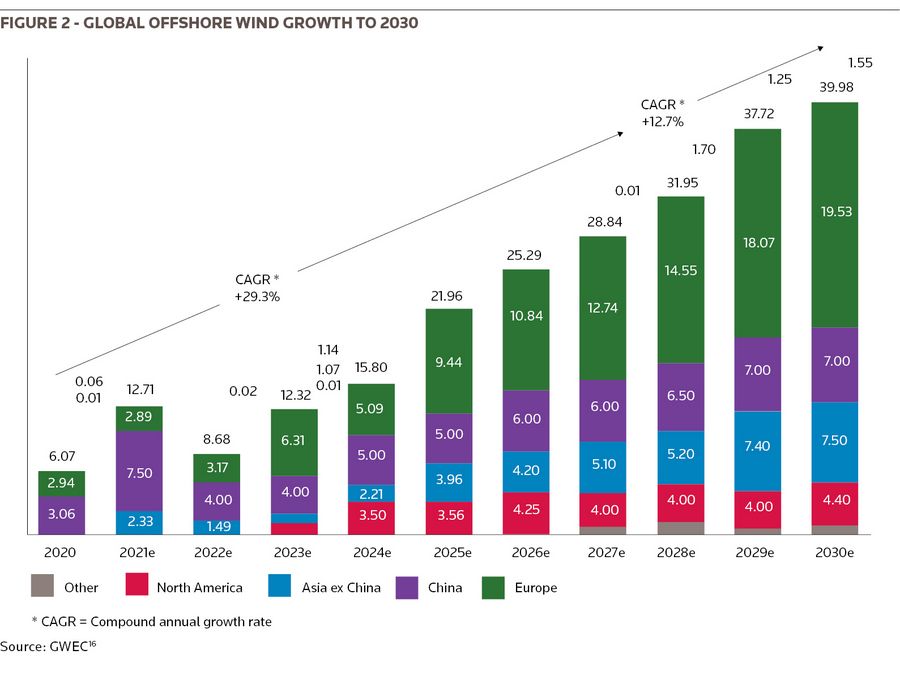

It is important for the supply chain that momentum generated over the last decade continues to build and, looking ahead, we see positive signs that it will. There are plans in the UK to deliver 40GW by 2030 backed by clear targets and government support to invest in supply chain growth. There is a strong appetite to stake a claim for developing the global supply chain needed to service the next generation of floating offshore wind – with ambitious plans not just in established markets, but in emerging markets. In addition, innovation and learning continues to drive down project costs and reduce risk in delivery and operation.

The industry may have to weather a storm in the short term, but with healthy long-term prospects it is well placed to do so and to look ahead to a bright future.

References

1 - BNEF - https://www.bnef.com/news/979939

2 - Prysmian quarterly results - https://www.prysmiangroup.com/sites/default/files/atoms/files/Prysmian_1Q21_Presentation_def.pdf

3 ABB Quarterly results: https://search.abb.com/library/Download.aspx?DocumentID=9AKK108466A0273&LanguageCode=en&DocumentPartId=&Action=Launch&_ga=2.39181411.1970274661.1636406074-1019899793.1636406074

4 - Sif Q3 2021 Trading Update: https://www.marketscreener.com/quote/stock/SIF-GROUP-N-V-26223618/news/Sif-Holding-N-V-Trading-update-Q3-2021-36912764/

Footnotes

1 - Crown Estate, “Offshore Wind Cost Reduction Pathways Study,” [Online]. Available: https://www.thecrownestate.co.uk/media/1770/ei-offshore-wind-cost-reduction-pathways-study.pdf.

2 - UK Government, “Contracts for Difference (CfD) Allocation Round 3: results – published 20 September 2019, revised 11 October 2019,” [Online]. Available: https://www.gov.uk/government/publications/contracts-for-difference-cfd-allocation-round-3-results/contracts-for-difference-cfd-allocation-round-3-results.

3 - IRENA, “Offshore Renewables: An Action Agenda for Development” (2021) [Online]. Available: https://www.irena.org/publications/2021/Jul/Offshore-Renewables-An-Action-Agenda-for-Deployment

4 - Taipei Times, “Offshore wind farm goal threatened by pandemic,” (6 June 2021) [Online]. Available: https://www.taipeitimes.com/News/front/archives/2021/07/06/2003760365.

5 - IEA, “Tracking Offshore Wind 2020” [Online]. Available: Tracking Offshore Wind 2020 – Analysis - IEA

6 - SGRE quarterly results, [Online] Available: https://press.siemens-energy.com/global/en/pressrelease/earnings-release-q3-2021-gas-and-power-track-sgre-impacted-onshore-wind-business.

7 - Vestas quarterly results, [Online]. Available: https://www.vestas.com/en/media/company-news/2021/vestas---interim-financial-report--third-quarter-2021-c3445958.

8 - S&P Global Market Intelligence, (5 November 2021) [Online]. Available: https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/dominion-increases-cost-of-offshore-wind-project-to-nearly-10b-67485135.

9 - BNEF, “1H 2021 Wind Turbine Price Index” [Online]. Available: 1H 2021 Wind Turbine Price Index (WTPI): New Costs Stress | Full Report | BloombergNEF (bnef.com)

10 - McKinsey, “What’s going on with shipping rates?” (20 August 2021) [Online]. Available: https://www.mckinsey.com/industries/travel-logistics-and-infrastructure/our-insights/whats-going-on-with-shipping-rates.

11 - Bloomberg New Energy Finance BNEF.

12 - 4COffshore News, “The Crown Estate plans 4 GW floating wind leases in the Celtic Sea,” (11 November 2021) [Online]. Available: https://www.4coffshore.com/news/the-crown-estate-plans-4-gw-floating-wind-leases-in-the-celtic-sea-nid24500.html.

13 - ESMAP, “Offshore wind,” [Online]. Available: https://www.esmap.org/esmap_offshore-wind.

14 - World Bank Group, “Key Factors for Successful Development of Offshore Wind in Emerging Markets” [Online]. Available: https://www.arup.com/news-and-events/new-report-from-arup-and-the-world-bank-supports-emerging-markets-to-develop-offshore-wind.

15 - Netherlands Enterprise Agency (RVM), “Offshore wind energy will be an export gem,” [Online]. Available: https://english.rvo.nl/news/business-cases/offshore-wind-energy-will-be-export-gem.

16 - GWEC, “Global Offshore Wind Report 2020” [Online]. Available: Global Offshore Wind Report 2020 - Global Wind Energy Council (gwec.net)

To see the digital version of this report, please click here

To purchase printed copies or a PDF of this report, please email gloria.balbastro@lseg.com