Pulau Indah Power Plant Sdn Bhd (PIPP) has been incorporated as a single-purpose company to undertake the development of a greenfield 2x600MW combined-cycle gas-fired power plant in Pulau Indah, Selangor, Malaysia. By Audrey Chew, Christopher Ang, Danny Lim and Eric Yap, UOB, Jerry Tiew Wei Hsiang and Leong Yew Seng, Adnan Sundra & Low, and Nasri Mohd Jamal, Worldwide.

On October 11 2021, the Prime Minister of Malaysia, Datuk Seri Ismail Sabri Yaakob, announced that the country hoped to reduce the intensity of greenhouse gas emissions across the economy by 45% based on gross domestic product (GDP) in 2030, and highlighted the nation’s aspiration to achieve net-zero GHG emissions as early as 2050. This would be the stand of the country, which was also tabled at the United Nations Framework Convention on Climate Change (UNFCCC) COP 26 (COP 26) in Glasgow, Scotland from October 31 to November 13 2021.

According to the Report on Peninsular Malaysia Generation Development Plan 2020 (2021 – 2039) published by the Policy & Planning of Electricity Supply Division under the Ministry of Energy & Natural Resources, the Peninsular Malaysia power sector is set to reduce its emission intensity against GDP by 45% in 2030. The supply mix in Peninsular Malaysia will see an increase in the renewable energy (RE) share from 17% to 31%, while the thermal capacity share will be reduced from 82% to 69% by the end of the horizon. Malaysia’s commitment to its sustainable energy pathway will continue with new RE and combined-cycle gas turbine (CCGT) plants coming into the system post-2030.

The Pulau Indah Power Plant project forms part of the national development agenda based on the approved Generation Development Plan, and is in line with the "Smart Selangor Blueprint", the roadmap towards more sustainable economic growth in Selangor, by enabling and supporting the state’s socio-economic ecosystem.

Project overview

Pulau Indah Power Plant Sdn Bhd (PIPP) was incorporated as a single-purpose company to undertake the development of a greenfield 2x600MW combined-cycle gas-fired power plant in Pulau Indah, Selangor, Malaysia. It is a natural gas powered CCGT with efficiency of more than 60%, much higher than its coal or oil equivalents. Costing an estimated M$3.35bn to build, PIPP will go through five phases of construction, namely (i) design, (ii) engineering, (iii) procurement, (iv) construction, and (v) commissioning, and will be fully tested in accordance with the terms of the power purchase agreement before commencing its scheduled commercial operation on January 1 2024.

The Central Region, Klang Valley, is the largest load centre and accounts for 43% of total electricity demand in Peninsular Malaysia. Currently with a deficit of power supply in the region, the Central Region relies heavily on long-distance transmission of power from the Northern and Southern regions.

Located in the Central Region, upon commissioning in January 2024, the Pulau plant is expected to support increasing power demand in the Klang Valley and boost baseload supply for the region due to its higher plant efficiency and closer proximity to the load centre. With substantial capacity retirement from 2021 to 2024 – Perak, Melaka, Johor, Penang, Perlis – and higher electricity demand, the plant will become more important in ensuring the continuity of electricity supply and stability of the grid for overall system security.

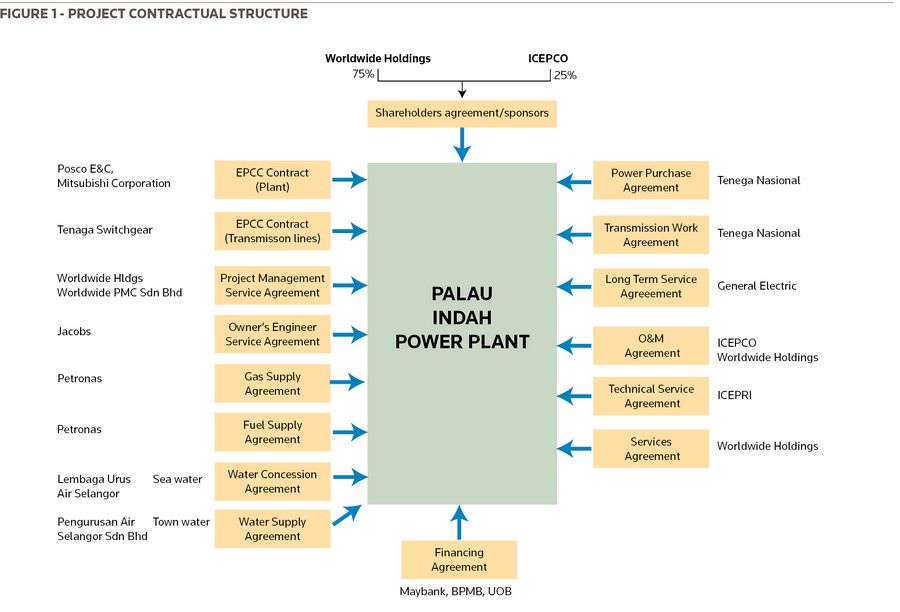

* Sponsors – PIPP is currently jointly owned by Worldwide Holdings Berhad (75%) and Korea Electric Power Corporation (25%). Maxim Global Berhad (Maxim), previously known as Tadmax Resources Berhad, was initially one of the sponsors prior to the disposal of its entire 40% equity stake in PIPP to Worldwide upon receipt of approval from the Energy Commission of Malaysia (Commission) on November 26 2020.

Worldwide is a state-linked company and a wholly owned subsidiary of the Selangor State Development Corporation, which is mainly involved in property development, environment management, medical device manufacturing, renewable energy and investments.

KEPCO is principally an electric utility company that is involved in the generation, transmission and distribution of electricity in the Republic of Korea. With its major shareholders being the South Korean government (18.2%) and Korea Development Bank (32.9%) and listed on the Korea Exchange and New York Stock Exchange, KEPCO is a dominant player in the South Korean power sector, owning and operating nuclear, coal-fired, gas-fired combined-cycle, hydro, solar and wind power plants with a total installed capacity of more than 100,000MW. The company is also active in many international markets in the power sector across Asia-Pacific, Europe, Africa and the Middle East.

* Timeline – PIPP received a letter of award from the Commission on September 10 2019 to undertake development of the project. On August 7 2020, PIPP signed the power purchase agreement (PPA) with national electricity utility company Tenaga Nasional Berhad (TNB), pursuant to which the plant’s entire daily available capacity and net electrical output will be sold to TNB for a period of 21 years from the start of the commercial operation of the first generating block.

* Implementation arrangement – On March 13 2020, PIPP entered into a fixed-price lump-sum contract with a consortium of companies comprising POSCO Engineering & Construction Co. Ltd (POSCO E&C), PEC Powercon Sdn Bhd (the local unit of POSCO E&C for onshore works) and Mitsubishi Corporation (collectively the EPCC contractor) to undertake the design, engineering, procurement, construction, completion, testing and commissioning of the plant.

The plant is designed to operate using natural gas supplied via a new lateral pipeline from Petroliam Nasional Berhad, Malaysia’s integrated international oil and gas company, in which it also uses distillate as the back-up fuel, under a 21-year gas supply agreement (GSA) entered into with Petronas Energy & Gas Trading Sdn Bhd.

PIPP has also inked a long term service agreement (LTSA) with General Electric Company (GE) via a consortium comprising GE Global Parts & Products Gmbh and GE Power Solutions (Malaysia) Sdn Bhd, and an operations and maintenance agreement (OMA) with Pulau Indah O&M Sdn Bhd, the O&M contractor, for the entire tenure of the PPA. The plant will be operated by the O&M contractor, a joint venture by the sponsors, capitalising on KEPCO’s extensive experience in operation and maintenance of plants of a similar nature.

Financing structure

Costing an estimated M$3.35bn to build, PIPP achieved financial close on March 10 2021, a few days before the final extended financial closing date of March 15 2021 granted by the Commission, when it secured a five-year Islamic syndicated bridging financing facility, the financing facility, granted by Bank Pembangunan Malaysia Berhad, Maybank Islamic Berhad and United Overseas Bank (Malaysia) Bhd, collectively the financiers.

The financing facility is secured by among others a first ranking legal assignment of all of PIPP’s rights, interests, titles and benefits under the material project documents, the Takaful contracts/insurance policies and all performance and/or maintenance bonds issued or to be issued to PIPP in relation to the project and the proceeds therefrom, a first ranking fixed and floating charge over all of the assets of PIPP as well as a first ranking fixed charge over the project land.

Further, the payment obligations of PIPP under the financing facility is guaranteed by Worldwide in addition to Worldwide’s undertaking to, among others, cover any shortfall in PIPP’s payment obligations, cover any cost overruns of the project and ensure the successful completion of the project. Along with the financing facility, the project also requires equity funding, whereby the sponsors via an equity contribution agreement would provide their respective proportion of capital contribution of no less than 20% of the total project cost to PIPP in accordance with the terms and conditions thereof.

Throughout the tenure of the financing facility, PIPP is obliged to ensure that the finance to equity ratio does not exceed 80:20 and the finance service cover ratio must be at least 1.25x.

Key challenges

* Stressed timeline – One of the key challenges faced by all project finance related transactions is to meet various project milestones and the timeline in order to achieve financial close. This was further exacerbated by the Covid-19 situation in Malaysia and the ensuing movement control orders imposed by the Government of Malaysia from March 2020 in an effort to curb the spread of the coronavirus. These lockdowns presented logistics challenges in terms of interactions between the stakeholders, which were critical to the successful financial closure of such a large and complex project financing.

At the same time, PIPP was also undergoing a corporate restructuring exercise whereby Worldwide acquired a 40% equity stake in PIPP from Maxim. This restructuring exercise involved lengthy negotiations and an additional documentation process, which put further stress on the timeline to achieve financial close.

While PIPP, the sponsors, the financiers and the legal counsels worked arduously to ensure that all documentations were completed to the satisfaction of all stakeholders, PIPP together with Worldwide were tasked to seek the extension of time to meet financial close from the Commission, knowing that the Commission does not view such request for extension of time lightly. Nevertheless, Worldwide was able to convince the Commission to approve the extensions, given that it was already reaching the tail-end of the financing process, and also in view of the Covid-19 pandemic situation.

In the meantime, the deadline to meet the first payment to the EPCC contractor was due and, with the extension of financial close, PIPP was able to meet the initial conditions precedent for drawdown under the financing facility in order to make the first payment to the contractor.

* Market volatility – Another key and overarching challenge faced by PIPP, was the unfavourable bond market conditions at the end of 2020 and the beginning of 2021.

The project was initially intended to be funded via a project finance Sukuk issue of up to 18 years, premised on an AA3 rating from RAM Rating Services Berhad. Work had already been undertaken/commenced with domestic rating agencies in order to provide potential investors with indications of the project rating and investor appetite was initially gauged to have been sufficient, particularly given the strong contractual framework for the project. Interest rates were at a record low following a cumulative 125bp point cut in the Overnight Policy Rate (OPR) by Bank Negara Malaysia (BNM) between January and July 2020.

However, the bond market turned volatile towards the end of 2020 and early in 2021, largely fuelled by inflation fears on the back of US stimulus hopes, vaccines progress and Federal Reserve’s policy stance. Investor demand for longer-dated paper were low and investors either preferred to stay on the sidelines or demanded higher compensation in yields to offset the uncertainties in the market. Several issuers that tapped the market during the period, including government-guaranteed issuers, were not able to garner sufficient liquidity for longer-dated bonds without paying steep premiums.

Given the following, as customary for project financings, (i) the tariff structure already agreed with TNB; (ii) the project company had already provided its customary assurances provided to various stakeholders on costs-to-complete; (iii) internal project budgeting, which already included heads of terms signed with long-lead time equipment providers and the EPCC contractor; (iv) financing cost expectations (which had an upper bound);); and (v) the sponsors’ and EPCC contractor’s expected rates of returns, there was an urgent need to pivot to an alternative financing plan in order to ensure the project would be able to be delivered as promised without reopening any new commercial discussions with all parties.

As such, amid the volatility in the market and mounting pressure to achieve financial close, financiers were required to quickly pivot and look for alternative solutions and work with PIPP to re-craft the financing plan. The natural alternative was the loan/project financing market, where it was gauged that there would be sufficient liquidity from lenders that appreciated the structure, the sponsors and the risks, in order to secure the five-year bridge financing facility, which also resulted in interest cost savings for PIPP against the planned Sukuk offering. This enabled the sponsors to carry on with the scheduled construction of the project, with a limited initial amortisation profile, while providing some respite for PIPP to chart its refinancing strategies prior to the maturity of the financing facility.

This quick pivot was due in no small measure to the rapid reaction and diligence by the financiers group, which ensured financial close was achieved on time, to sponsors’ satisfaction. Furthermore, as the covenants and conditions for the financing were already pre-negotiated with the client earlier in anticipation of the previous proposed Sukuk solution, coupled with partial engagement with project finance lenders, the eventual credit assessment process by the financiers was able to be expedited given the shorter period required for negotiation.

To see the digital version of this report, please click here

To purchase printed copies or a PDF of this report, please email gloria.balbastro@lseg.com