Water, being a basic human need, is at the centre of economic and social development, and proper planning and management of water resources is critical to managing the environment and sustaining economic growth. By Ali Tahir Jaffery, executive director, project and export finance, AME, at Standard Chartered, and Mohamed Hamdouch, director, project finance, and Sirine Taheri, manager, project finance, at ACWA Power.

The Middle East is regarded as one of the most water-scarce regions on the planet with limited reserves of non-renewable groundwater resources. Not only are these reserves being rapidly depleted, but the region also faces serious challenges due to unsustainable use of water resources. Arid climate conditions, increasing urbanisation, and high demand from the agriculture sector are further exacerbating the water scarcity situation. Water management strategies, therefore, continue to be at the top of the agenda for every country in the region, and desalination is at the heart of each strategy.

According to a recent industry report, investment in desalination projects in the Middle East and North Africa has increased substantially in recent years and accounts for 48% of global investments in desalination projects, with further investment expected to spur the market to US$4.3bn by 20221. With these ongoing investments, seawater desalination now contributes to more than 90% of all daily water requirements in the GCC region. Desalination capacity of GCC countries is expected to grow further by approximately 37% during the next five years, with investments of up to US$100bn, according to reports, while the global desalination market is predicted to grow from US$17.7bn in 2020 to US$32.1bn by 2027.

The Kingdom of Saudi Arabia is at the forefront of this investment drive into the water sector. The Kingdom’s population is expected to grow from 35m in 2021 to around 40m by 2026. This growth will continue to put pressure on water resources and supporting infrastructure. According to the Ministry of Environment, Water, and Agriculture (MEWA), a demand supply gap of 4.5M m3/d is expected by 2026 if firm policy measures are not implemented. Accordingly, more than 60 water projects were announced in 2022 worth US$9.3bn.

KSA has adopted public-private partnerships as the preferred procurement strategy, with 70% of its water processing infrastructure projects procured on this basis. Saudi Water Partnership Company (SWPC) has been entrusted with the overall procurement process of the new capacity. SWPC plans to increase the desalination capacity of the Kingdom from 1.5M m3/d in 2019 to 8.5M m3/d by 2025, which is a nearly six times increase merely six years.

In addition to the new projects, several other strategies for water resource management are also being implemented under the “National Water Strategy 2030” that was announced in 2017. These include curbing the national urban water per capita requirement by encouraging demand-side management, minimising network losses, and improving cost competitiveness and promoting environmental sustainability by phasing out the older and relatively inefficient thermal desalination capacity.

Pursuant to the stated strategy, SWPC initiated discussions in 2020 with the existing shareholders of Shuaibah Water & Electricity Company (SWEC) to dismantle the existing oil-fired power capacity and reconfigure the existing energy intensive multi-stage flash (MSF) based thermal desalination facility into a far more energy-efficient greenfield, sea water reverse osmosis (SWRO) desalination plant. The parties agreed to implement the overall programme in three steps:

1 – Procurement and development of a new 600,000 m3/day SWRO-based desalination project;

2 – Refinancing the existing debt originally procured to finance the development of SWEC – the 900MW and 880,000 m3/day IWPP – in 2005; and

3 – Dismantling the existing SWEC facilities when the new project (Shuaibah 3) is operational in Q2 2025, saving nearly 45 million tons of carbon dioxide emissions and 22 million barrels of light crude oil annually.

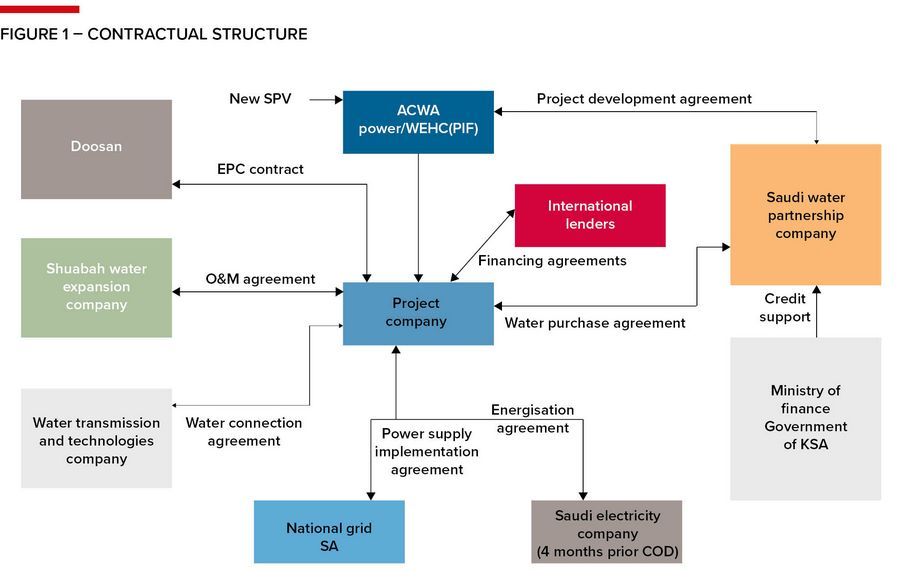

Shuaibah 3 IWP procurement

SWPC invited ACWA Power to submit a proposal to develop Shuaibah 3 as a standalone independent water project in the vicinity of SWEC at the Shuaibah industrial complex, located in the town of Shuaibah in the Western Province of KSA. The project will primarily cater to the water demand of Jeddah and Makkah, especially during peak demand periods such as the Holy Month of Ramadan and the Hajj seasons.

ACWA Power submitted a fully funded proposal to develop the project to SWPC in August 2021. After a detailed clarification process, the project was formally awarded to ACWA Power in 2022 and the water purchase agreement for the project was executed in June 2022. As contemplated during the bilateral discussions during the clarification round, Water & Electricity Holding Company joined ACWA Power as a co-investor prior to signing of financing documentation in September 2022.

Shubaiah 3 will be developed based on SWPC’s well established framework that is structured on the following principles:

* A 25-year water purchase agreement commencing from the project commercial operation date based on an availability-based tariff structure;

* 100% ownership of the project company by the private/commercial investors with no direct government shareholding;

* Credit support provided by the Ministry of Finance covering all payments due under the water purchase agreement, the SWPC credit support; and

* Development of certain electrical special facilities including a sub-station and overhead lines connecting to the grid, which are to be transferred to National Grid SA ahead of the project commercial operation date.

Shuaibah 3 is testament to SWPC’s strong commitment towards a clear shift to more energy-efficient initiatives for cleaner desalination solutions, in line with the Kingdom’s National Water Strategy 2030. In addition to the adoption of RO technology, which is considered to be more energy-efficient than traditional thermal desalination technologies, the introduction of renewable energy in the recent desalination projects further reduces the carbon intensity of these projects when compared with traditional technologies.

Shuaibah 3 will also be partially energised by an integrated 60MW photovoltaic solar plant, which will reduce electricity consumption from the grid by 45% and minimise the carbon footprint of the project. The switch from thermal to RO will reduce the power needed to desalinate seawater by 70%. The financing for the project has accordingly been certified as a green financing by S&P Global, with Standard Chartered Bank acting as the Green Loan Coordinator.

Another important feature of the project is the firm localisation expectation set by SWPC to promote local industry and human resource development. Local content of the project will amount to 40% in the construction phase; 50% in the operation and maintenance phase for the first five years; and will eventually increase to 70%.

* Shareholding – Shuaibah 3B will be implemented through a standalone Special Purpose Vehicle, Al Jubail International Water Company. The SPV is owned 68% by ACWA Power and 32% by Water and Electricity Holding Company (Badeel).

ACWA Power is the largest private developer of water desalination plants in the world, with a production capacity of 6.4m3 of desalinated water a day. The company has a portfolio of 10 SWRO projects in the Kingdom of Saudi Arabia and GCC. ACWA is also the leader in integration of clean energy to fuel water desalination and has installed several regional mega projects, such as the Rabigh 3, Red Sea development project, Jubail 3A, Umm Al Quwain IWP, and Taweelah IWP. ACWA Power currently produces enough water to meet the needs of 24 million people daily.

Water & Electricity Holding Company (Badeel or WEHC) is a wholly owned subsidiary of the Public Investment Fund (PIF). It is engaged in investing in water and electricity production projects owned, or co-owned, by PIF, managing these investments, and carrying out all activities related to its purposes. The main investments of WEHC are desalination and renewable projects, water purification, sewage water treatment and co-generation for the private sector, water storage tank projects, purchase and sale of water (desalinated, purification, treated and untreated) and electricity.

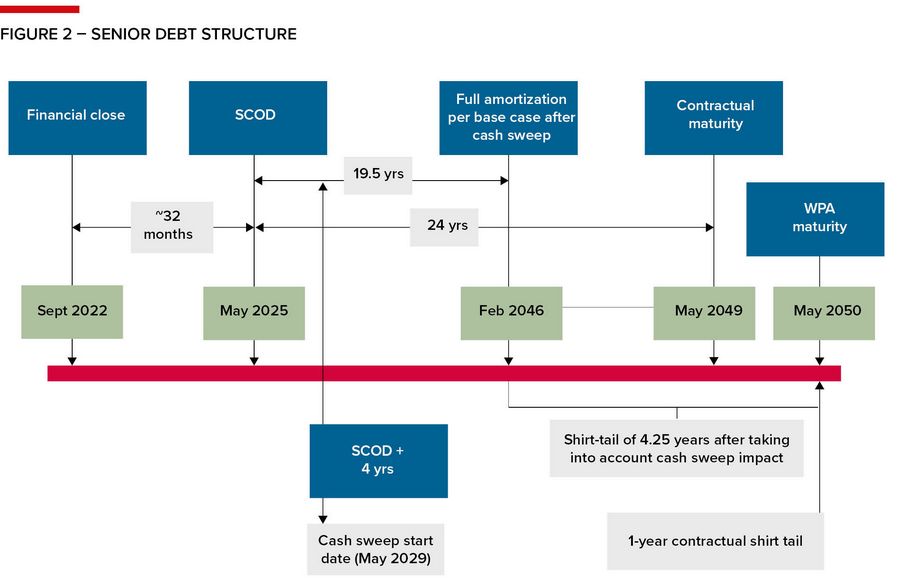

* Financing plan – The total project cost of US$821m is being financed by senior project finance debt and equity in a 77:23 ratio. The sponsors are to provide the entire base equity upfront prior to the drawdown of debt in the form of equity bridge loans (EBLs). The financing plan allows for the EBLs to be extended until two years post-commercial operation date.

Total senior debt amounting to approximately US$632m has been sized on the basis of a minimum DSCR of 1.2x and with a contractual door-to-door tenor of a little over 26.5 years. The facility has been structured on a soft mini-perm basis with a pricing step-up and a cash-sweep mechanism to incentivise refinancing once the construction risk falls away.

Under the proposed structure, on the failure by the project to refinance the debt by commercial operations date (COD) plus 4 years, a mandatory cash sweep will be triggered to ensure that the facilities are fully amortised within 21.5 years of the scheduled commercial operations date. Such a structure has become commonplace for similar financings in the region.

The senior debt was fully underwritten by Standard Chartered and MUFG Bank, the bookrunners, at the proposal stage to provide certainty of financing to the sponsors during the negotiation stage. The transaction was formally launched by the bookrunners into the wider lending market after the execution of WPA. The financing was eventually signed in September 2022 by a group of nine banks including Bank of China, ICBC, MUFG Bank, Saudi Investment Bank, Saudi National Bank, Standard Chartered, and the Korea Development Bank providing the commercial facility, with Abu Dhabi Investment Bank and Werba Bank being Islamic lenders. Standard Chartered acted as lead documentation bank for the financing while MUFG is acting as intercreditor agent.

* Contractors – The project will be constructed by Doosan Enerbility, previously known as Doosan Heavy Industries and Construction Co Ltd, under a date-certain, fixed-price, lump-sum turnkey contract. O&M Services will be provided by a subsidiary of Nomac Holding, which itself is fully owned by ACWA Power, under a long-term O&M contract.

SWEC refinancing

ACWA Power and SWPC agreed in June 2022 to amend and restructure the PWPA of Shuaibah Water & Electricity Company (SWEC) in a way to replace it with the new IWP – Shuaibah 3 IWP. Upon achieving COD of Shuaibah 3 IWP, the SWEC power and desalination facilities will be decommissioned; however, SWEC, the project company, will continue to receive the capacity payments until the expiry of the original PWPA term, in Q1 2030. SWEC will continue to exist until the decommissioning is complete and will continue to be owned by the existing shareholders, ACWA Power (30%), PIF (32%), Saudi Electricity Company (8%), Tenaga Nasional Berhad (6%), and Malakoff Corporation (24%).

The restructuring, however, necessitated a refinancing of the existing US dollar and Saudi riyal denominated senior debt facilities. Accordingly, in October 2022, SWEC successfully replaced US dollar and Saudi riyal tranches of existing outstanding senior debt, US$415m and, SR285m, respectively with US$420m and SR285m facilities respectively, repayable semi-annually with the final instalment to be paid in January 2026. Financial close for the US$497m senior debt facility arranged on a non-recourse project finance basis was from a consortium of financiers comprising Societe Generale, Al Rajhi Bank, Bank Saudi Fransi, and ADCB.

Furthermore, owing to the removal of operational risk, as SWEC will continue to get payments without incurring operational risks, the company has successfully replaced the existing subordinated debt facility, US$111.6m, with a US$230m subordinated debt facility from Al Rajhi Bank on competitive terms, repayable semi-annually, with the final instalment to be paid in July 2028.

In addition to above, a special facility of US$69m, repayable semi-annually with its first payment due in January 2025 with the final repayment in July 2029, is being taken to meet a one-time tax liability in 2023. The special facility has been secured from group of three banks, including Societe Generale, Al Rajhi Bank, and ADCB.

Altogether, the new financing facilities have been structured to optimise the capital structure of SWEC in view of the unique operational plan for the project company.

Challenges

The Saudi PPP and project finance market is currently one of the most active anywhere in the world, and while the project follows an extremely well-established framework, it too had to face certain challenges:

* Award process – Given the nature of the project and its linkage to the existing SWEC project, the existing shareholders of SWEC were given the first right to develop Shuaibah-3. ACWA Power was the only shareholder to agree to develop the new project. The tariff of the project was negotiated with SWPC through a detailed price discovery mechanism.

* Insurance markets – The insurance market has been witnessing a significant hardening of terms owing to various natural calamities, including flooding and wildfires in many parts of the world. Covid-19 further compounded these challenges, with estimates suggesting incremental costs of circa US$220bn added to the insurance market due to the global pandemic. Insurers have been increasing premiums, reducing coverage and increasing deductibles to recoup their losses. The project was nevertheless able to procure a bankable insurance programme on the back of the track record in KSA and appropriate overall risk allocation.

* Localisation requirements – The water purchase agreement included significant requirements for local content and Saudisation obligations, and liquidated damages for failure to meet such targets.

* Regulatory regime – The Saudi PPP market has undergone several regulatory reforms and other general legal developments. The implementation of the project had to account for the changing environment in respect of updates to the environmental and social processes, VAT rates, and the customs duties regime.

* Refinancing of the existing project – The current senior loan tenor of SWEC is until 2026 and decommissioning activity would take place within the loan period. For the restructuring of the existing project, the company had to obtain existing lender approval to stay in the project. A number of the existing lenders showed a reluctance to continue as lenders post-decommissioning, as typically decommissioning takes place after the debt maturity.

While the underlying structure is not particularly complicated, the underlying nature and the risk allocation of the financing is fundamentally different post-decommissioning, and the lenders had to be comfortable with this. As a result, some of the key banks to the existing project exited, which almost collapsed the financing for the existing project. After considerable effort, ACWA Power was, however able to form a completely new set of lenders willing to refinance the existing debt with the same tenor and at lower rates.

* Tax and accounting impact of restructuring – On review of the restructuring impact on tax and accounting, it was noted that the restructuring of SWEC will result in a tax liability that is greater in the earlier years of the termination due to the requirement under the local GAPP (IFRS). While the overall impact of tax is neutral, the timing impact on foreign shareholders’ return was significant due to the large tax liability to be paid upfront on income that will not be paid to shareholders in full for many years. This risk was mitigated by raising an additional tax facility, a “special facility”, which will advance the funds to foreign shareholders for the payment of their corporate income tax.

SWPC’s future plans

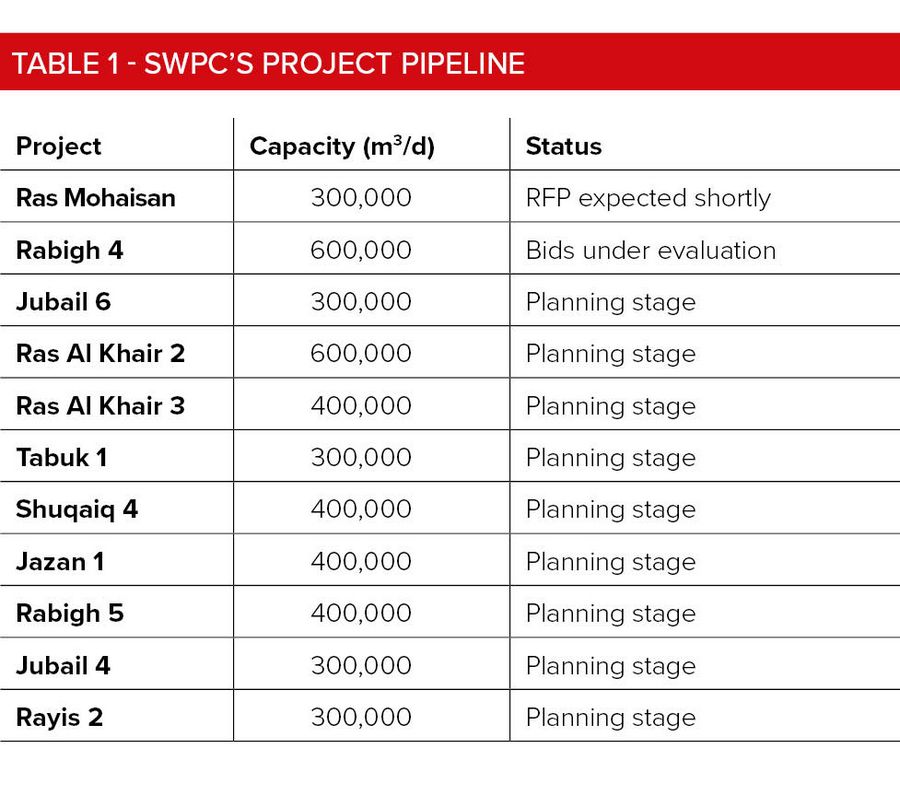

SWPC has set itself ambitious targets for boosting its current desalination capacity to meet increasing demand. It will therefore continue to focus on procuring new RO based desalination plants and has accordingly announced a number of desalination projects to be constructed in order to bridge the estimated demand/supply gap, see Table 1 below.

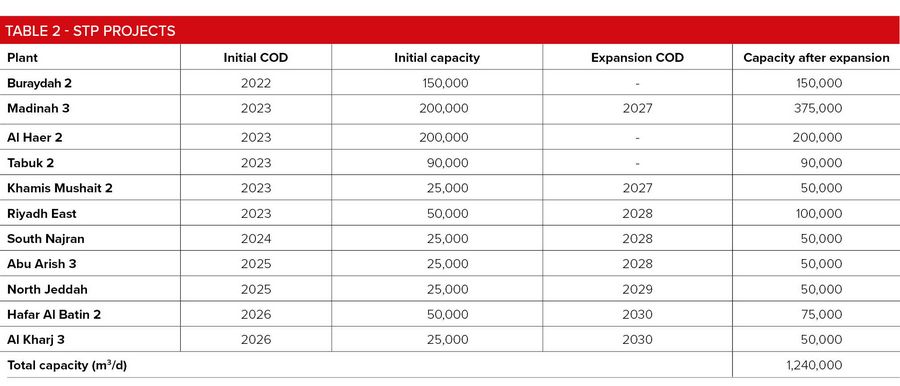

SWPC is committed to KSA’s waste-water treatment and re-use objectives under its vision 2030 plan. The goal is therefore to not only increase network coverage in the Kingdom but also to boost the waste-water collected and treated using sewage treatment plants (STPs) throughout the Kingdom. While SWPC’s primary focus is on large STP plants that would not only benefit from economies of scale but also be attractive to the private sector and feasible for project financing, a large number of small-scale projects, 1,000 m3/d up to m3/d, will also be set up.

In addition to water production facilities, SWPC also aims to develop water transmission and strategic storage facilities to strengthen the resilience of the sector against demand spikes or supply shortfalls. To that end, sector policies set a strategic storage target for 2022 equivalent to 3 days of municipal water demand. In addition to their emergency role, strategic water storages will also be used for peak load management of Hajj water demand, which takes places in a span of approximately 20 days in Makkah and 40 days in Madinah, resulting in a considerable short-term peak demand water.

Footnote

1 - Source: MENA Desalination Market report by Ventures Onsite.

To see the digital version of this report, please click here

To purchase printed copies or a PDF of this report, please email leonie.welss@lseg.com