To understand the challenges and opportunities of investing in Romania and Bulgaria, it is important first to understand how the renewable energy sector has developed in each country. By Alastair Hammond, CEO, Rezolv Energy*.

In Bulgaria, electricity production is still heavily dependent on fossil fuels – particularly brown coal, or lignite, which makes up more than 85% of the fossil fuel total. This is a major problem because while lignite is the cheapest source of electricity from fossil fuels, it causes the highest CO2 emissions per tonne when burned, one-third more than hard coal and three times as much as natural gas.

The main reason for this dependence on lignite is that, at least up to 2022, Bulgaria made limited progress in developing wind and solar capacity. Bulgaria was a relatively slow-starter on renewables: wind power was introduced, in small quantities, in 2006; solar production only got going in 2010. Both industries experienced a "boom" between 2010 and 2013, but after that, new renewables capacity was effectively halted for a decade.

The good news is that the wheels are now turning and the energy transition is well underway in Bulgaria – particularly on solar, where capacity increased by more than 80% last year.

The context in Romania is different. Last year, the percentage of electricity generated from fossil fuels dropped below 30% for the first time. That was primarily explained by the growth of renewable energy, with overall renewables capacity increasing from 43.1% in 2022 to 50.4% in 2023, comfortably the highest level it has ever been. Of that renewable capacity, 65% was hydropower but, as in Bulgaria, 2023 was the year when Romanian solar turned the corner, with more than 1GW of new capacity installed. This was a 300%+ increase on 2022 – making solar PV the fastest-growing power source in the country.

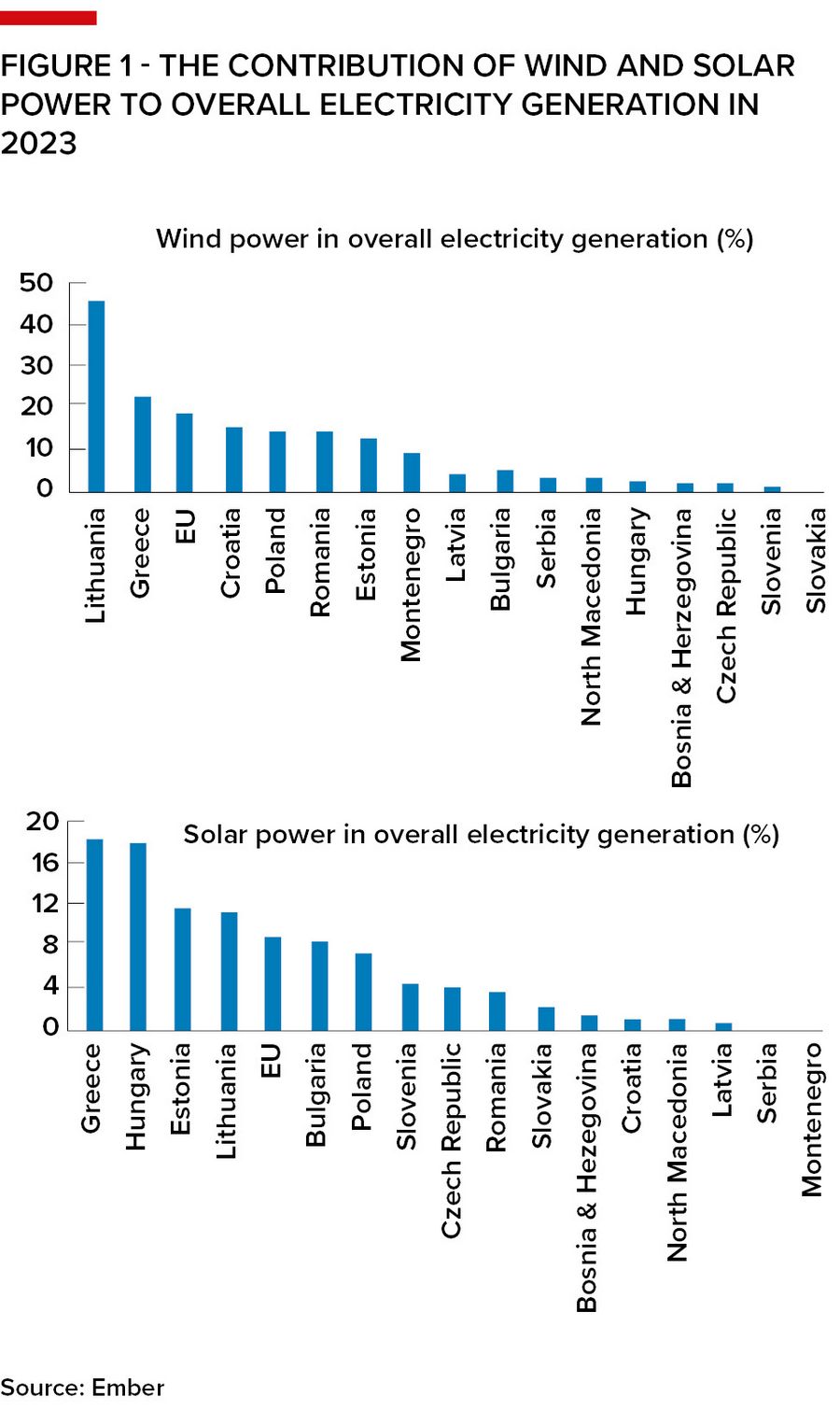

To put all of that into a regional context, here is how Romania and Bulgaria stacked up against other countries in Central and South-Eastern Europe last year in terms of wind and solar capacity, see Figure 1

Financing challenges

The renewable capacity increases in 2023 were obviously good news, but it does not mean that every piece of the jigsaw is in place. Specifically, there are several elements of the evolving financing environment that have taken time to catch up:

* The PPA market is slower than everyone in the industry would like, although attitudes are changing fast – The power from Rezolv’s wind and solar plants will be sold to commercial and industrial users through power purchase agreements (PPAs), and the truth is that the PPA market in South-Eastern Europe does not yet match the political support that we are now seeing behind the energy transition. Why?

It is primarily because PPAs are still a relatively new concept in this region. The first PPA in Romania was only signed in 2021; it was one year later in Bulgaria. We need to accept that it is a significant change in buying habits. You are asking a company that has always bought electricity annually through an energy trader to sign a contract for a 10 year plus period directly with an energy producer. It is a big step, in terms of financial commitment but also confidence and risk appetite, and it is therefore understandable that buyers are cautious.

a significant change in buying habits. You are asking a company that has always bought electricity annually through an energy trader to sign a contract for a 10 year plus period directly with an energy producer. It is a big step, in terms of financial commitment but also confidence and risk appetite, and it is therefore understandable that buyers are cautious.

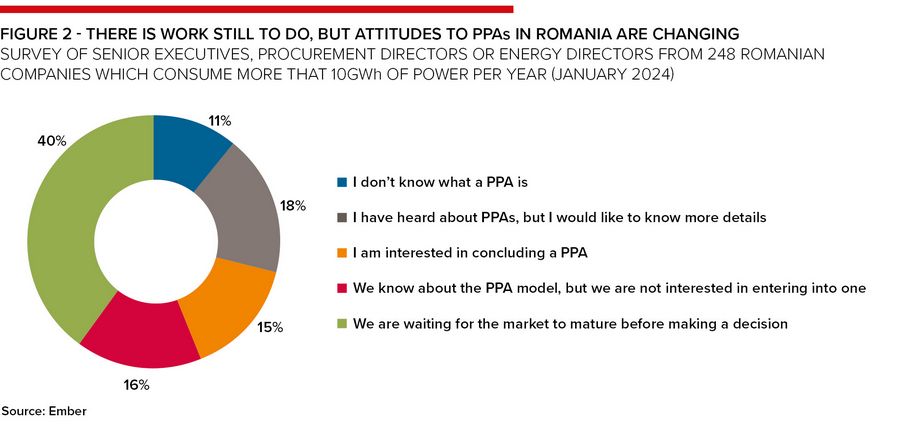

However, things are changing quickly. Creative Communication recently ran a survey of 428 Romanian companies that consume more than 10GWh of power per year, asking them for their views on buying renewable energy through PPAs. At first sight, the results might not look overwhelmingly positive, but they are actually very encouraging, see Figure 2.

Why is this encouraging? Because if that same survey had been run 12 months ago, there would have been far higher numbers in the “I don’t know what a PPA is” and “We know about the PPA model, but we are not interested in entering into one” categories.

It is also heartening because some of the concerns that exist – specifically in the 40% of businesses that said they were waiting for the market to mature before making a decision – will dissolve away as more PPAs are signed, which will happen this year.

Also, based on our experience, the connection between PPAs and project financing is starting to become more broadly understood in South-Eastern Europe. Increasingly, companies are realising that the opportunity in a PPA is not just to ensure their long-term supply of clean power at a stable price. It will also help build the project that will supply them. A PPA is therefore not just a way for them to benefit from the energy transition, it is a way for them to contribute. On top of that, they can claim additionality because they are supporting renewable energy generation that is new rather than already available.

This is particularly attractive if the offtaker knows that the project will be constructed and operated to the highest ESG standards: that the developer is fully committed to protecting nature at the project sites, and to leaving a lasting, positive legacy in the local communities. This is one of many reasons why Rezolv has developed such a robust sustainability strategy and intends to set the standard for the responsible development of renewable energy projects in this region.

* The Romanian government has not yet joined the AIB so that guarantees of origin can be transferred cross-border, but is planning to do so – There is also one remaining regulatory barrier holding the PPA market back in Romania. This concerns guarantees of origin. GOs prove to a final customer that the energy they are buying was produced from renewable sources. They are a critical component of corporate PPAs. Without them, PPA buyers cannot verify the type of electricity they are using and are unable to meet strict carbon accounting requirements, or prove compliance with RE100 and SBTi rules. Crucially, for the multinational firms that are currently driving most of the demand for PPAs in South-Eastern Europe, GOs also need to be transferrable between EU member states.

It is this ability to transfer GOs across borders that is the problem in Romania because, within the EU, it is only possible if the GOs are certified by the Association of Issuing Bodies (AIB). Bulgaria is applying to join the AIB; Romania is one of only two member states that are neither members nor yet in the process of joining. The Romanian government is working on this, and we are hopeful that it will be remedied very soon because it is the policy change that would have the biggest impact on the financing of renewable energy projects.

* Romania’s contracts for difference scheme is yet to emerge – In March 2024, the Romanian Ministry of Energy published a draft government decision that laid down the general legal framework governing the implementation and operation of a contracts for difference (CfD) scheme. The eligibility criteria will be laid out in due course through a CfD ministerial order.

We will only be able to pass judgement on the scheme once the ministerial order is published and we have all the details, but we certainly support and appreciate the efforts of the government to launch the CfD scheme. It should, we hope, have a hugely important role in helping accelerate the energy transition.

Challenges outweighed by opportunities

All three of these challenges, then, are in the process of being resolved – and they are anyway comfortably outweighed by the opportunities open to renewable energy investors in this region. These opportunities are not just commercial. We also have the chance to make a tangibly positive impact on people’s lives in this region.

I would highlight two areas in particular:

* Improving the air people breathe – Primarily as a result of the burning of fossil fuels, air quality remains a significant problem across South-Eastern Europe. There are many different air pollutants, but one of the most significant for human health is fine particulate matter (PM2.5), because exposure to PM2.5 at above recommended levels is a leading cause of premature death and disease, particularly stroke, cancer and respiratory disease.

While average air quality is worse in Bulgaria than it is in Romania, Romania is still fourth on the EU list when it comes to premature deaths attributable to exposure to PM2.5 – behind only Bulgaria, Poland and Hungary. A rapid reduction in energy sector emissions will therefore have more than a significant climate impact: it will also have a direct, tangible impact on public health.

* Safeguarding the long-term economic health of the region – Accelerating the energy transition has become an economic imperative as well as an environmental one in South-Eastern Europe. Several of the countries in the region – including Romania and Bulgaria – are among the most heavily industrialised economies anywhere in Europe. Much of this industry is integrated into the supply chains of major multinational companies, many of which have committed to comprehensive net-zero and renewable energy targets.

Take the automotive industry as an example. It is probably the sector most closely associated with Central and South-Eastern Europe, and continues to play an outsized role economically. For example, Slovakia, Romania, the Czech Republic and Hungary are all in the top five countries in the EU when it comes to the proportion of jobs created directly by the automotive sector.

The list of automotive companies that manufacture in the region is dominated by the biggest names worldwide. It includes all of the top five automotive companies globally: Volkswagen, which has manufacturing plants in the Czech Republic, Hungary, Poland and Slovakia; in Toyota, the Czech Republic and Poland; Stellantis in Hungary, Poland, Serbia and Slovakia; the Mercedes-Benz Group, in Hungary and Poland; and Ford (Romania). Crucially, all of these companies have committed to firm decarbonisation deadlines that affect Scope 3 emissions, ie emissions from the supply chain, as well as Scopes 1 and 2.

The issue is that, in most cases, these multinational companies have moved faster than their local suppliers – which, if they are to hold on to those important contracts, will need to catch up quickly and meet their major customers’ renewable energy consumption requirements. Enabling local companies to procure clean power will therefore be vital to their long-term viability, and to economic competitiveness at a national level.

A once-in-a-lifetime opportunity

After a decade when the "pause" button was pressed on the development of renewable energy in South-Eastern Europe, the era we are living in now is a genuine period of transformation. While there remain financing challenges, they are being addressed and the energy transition is now in full swing. Clean energy capacity is coming onstream in volume and the largest-scale projects – including Rezolv’s – will start to become operational from next year.

The benefits will go far beyond the obvious emissions reduction priority. They will also safeguard energy security, reduce energy bills and enhance the competitiveness of local businesses. People like me who have worked in renewable energy in Central and South-Eastern Europe for a large part of our careers recognise this as a once-in-a-lifetime opportunity, and I am very proud that Rezolv is out in front, driving the transition forward.

* Rezolv was launched almost two years ago to accelerate the energy transition in Central and South-Eastern Europe. Backed by €500m from Actis, we already have well over 2GW of clean energy being prepared for construction. This includes two very large solar PV projects: St George, which will become one of Bulgaria’s largest solar plants, and Dama Solar, a 1,044MW plant in western Romania that will be the largest solar project anywhere in Europe once it is operational. We also have more than 1GW of wind power under construction in Romania through two projects that we are developing in partnership with Low Carbon.

To see the digital version of this report, please click here

To purchase printed copies or a PDF of this report, please email shahid.hamid@lseg.com in Asia Pacific & Middle East and leonie.welss@lseg.com for Europe & Americas.