The global transition to decarbonise is underway to achieve the target of net-zero carbon emissions, including across Asia. The use of carbon capture and storage is seen by many – including the Intergovernmental Panel on Climate Change and the International Energy Agency – as a key part of the solution to achieving net zero, particularly for hard-to-abate sectors such as steel, cement and petrochemicals. By Frederic Draps, Jean-Louis Neves Mandelli, Dan Trevanion and Damian Tan, at Ashurst LLP

This is also the case in South-East Asia, where there has been a significant increase in proposed carbon capture and storage (CCS) projects, leveraging the abundance of mature oil and gas reservoirs that are gradually approaching the end of their productive lives.

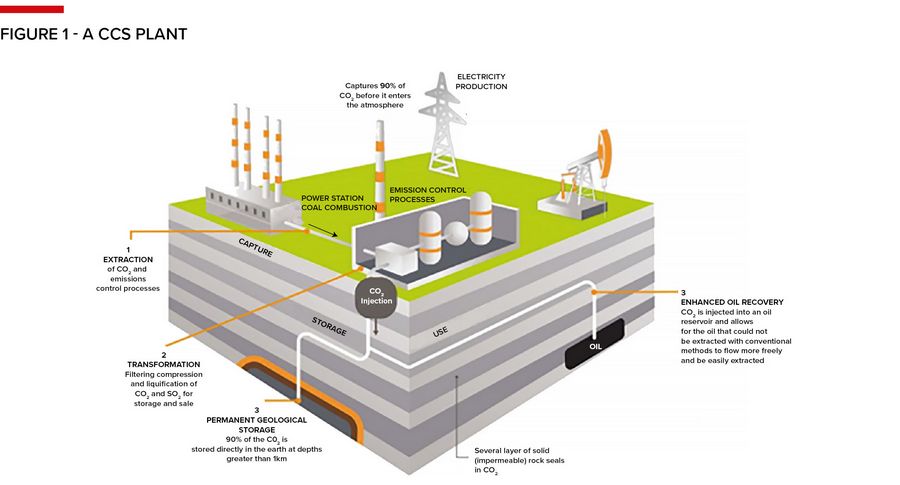

While CCS technology has been used for many years to enhance oil recovery, developing a viable economic model for the permanent capture and storage of CO2 has its challenges.

Most CCS projects for decarbonisation purposes involve capturing CO2 – usually from a facility that emits CO2, ie, point-source capture – which is subsequently compressed or liquefied and transported via pipeline or ship to the point of injection and storage, which typically consists of geological formations, including depleted reservoirs in the sea-bed or saline aquifers. The intention of these CCS projects is to ensure that the carbon emitted is permanently removed from the atmosphere and stored. If all the CO2 emitted from an emitter is stored, as opposed to released into the atmosphere, then that emitter should be able to achieve net-zero.

Location is key

Perhaps unsurprisingly, a key factor for the success of CCS projects is their location, specifically, having significant sources of CO2 emissions in the proximity of the point of storage, so as to minimise capture and transport costs.

Capture costs remain high across the industry. While it is expected that these will reduce as technological advances are made, for now, the projects that have tended to be most economic have been those that were able to benefit from higher CO2 volumes and concentration.

Some of the lowest cost CCS projects have been those that rely on transportation by pipeline over short distances and that can leverage existing infrastructure.

* How does this translate into South-East Asia? – The good news is that there are significant geological opportunities across the region. Countries like Malaysia, Indonesia, Thailand and the Philippines have an abundance of mature oil and gas reservoirs that could be repurposed for CCS projects. These existing oil and gas reservoirs also often have existing infrastructure from their oil and gas operations that could be repurposed for CCS, reducing the additional capital expenditure.

For example, Petronas, the Malaysian national oil company, identified more than 46tcf of potential storage in depleted gas reservoirs in offshore Peninsular Malaysia and Sarawak that could be used to store CO21.

In addition to depleted oil and gas reservoirs, there are a number of saline aquifers in the region that also present significant geological opportunities for CCS. For example, it is estimated that Indonesia’s saline aquifers can store up to 600 billion tonnes of carbon CO2. Saline aquifers can offer much larger CCS opportunities, increasing economies of scale (for this reason, they are the focus of CCS efforts in countries such as the UK), but will usually not have existing infrastructure which can be leveraged.

* So what about the CO2? This is where the South-East Asian situation is somewhat unique. Many of the storage sites for CCS projects are located far from major industrial areas from where CO2 could be captured. Also, most South-East Asian countries with significant geological potential for CCS are developing economies that are structurally less able to support some of the financial incentives that more developed economies such as the UK, the US and the European Union have implemented to support – directly or indirectly – the development of CCS projects.

This has meant that the focus for many CCS projects in South-East Asia has been to offer storage services for CO2 captured by emitters in more developed economies both within South-East Asia – such as Singapore – and regionally – such as Japan, South Korea and Taiwan. These countries, with combined annual CO2 emissions of 840m tonnes, comprise some of the largest industrial point emitters, but often do not have access to viable sites for carbon storage or do not have access to sufficient viable carbon storage sites.

The benefit of this approach is that it allows less developed economies to leverage their CCS potential, while minimising the additional cost for their governments.

However, this approach does not come without challenges.

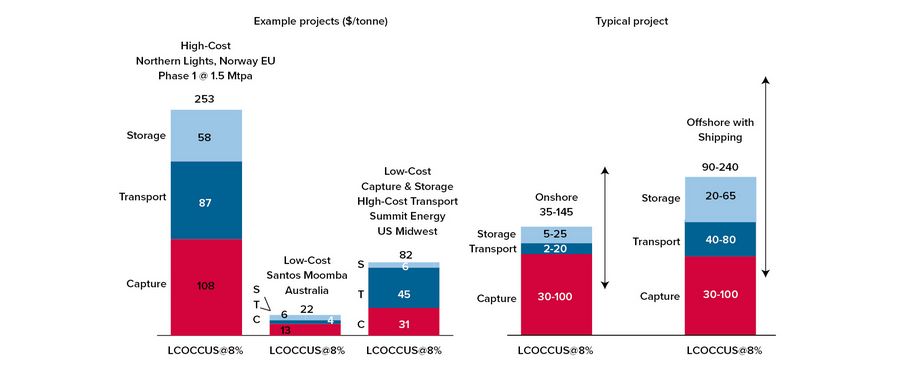

A key one is cost. Cross-border transportation of CO2 from countries such as Japan and South Korea to South-East Asia is expensive as, it would require liquefaction of the CO2, shipping (including loading/unloading) and treatment before re-injection, not to mention carbon-intensive. With respect to cost, Wood Mackenzie estimates that for the Northern Lights project in Norway, which involves the capture of CO2 in other European countries and transportation by ship to Norway for storage, the cost of capturing and storing CO2 is US$253 per tonne of CO2, of which US$87 relates to transport cost. By contrast, for the Santos Moomba project in South Australia, which involves onshore transportation and storage via pipeline, the cost of capturing and storing CO2 is US$25 per tonne of CO2, of which US$4 relates to transport cost.

Another challenge is regulation. Currently, there is little by way of regulation for the cross-border transportation and storage of CO2.

The Convention on the Prevention of Marine Pollution by Dumping of Wastes and Other Matter of 1972, an international treaty also known as the London Convention, regulates the disposal of waste at sea, including carbon dioxide. The parties to the London Convention have since developed the London Protocol, which now includes a legal basis in international environmental law to allow the export of CO2 by one country for geological storage in another, but not many states have ratified the London Protocol, including in South-East Asia.

There is also the question of what benefits, economic and otherwise, the host country receiving CO2 from another country should be receiving as consideration for allowing foreign-sourced CO2 to be stored in their geological formations. This is an issue that a number of countries in South-East Asia are grappling with as they look to implement these cross-border arrangements. While existing upstream oil and gas contracts could be seen as a starting point for consideration of these issues, the economic fundamentals of CCS are very different to those of upstream oil and gas contracts, which means that tailored solutions would need to be developed.

Of course, not all schemes in South-East Asia are focused on the storage of imported CO2. Projects such as the Arthit CCS project in the Gulf of Thailand, which is being implemented by Thailand's national oil company, PTTEP, together with INPEX Corporation of Japan, focuses on sequestering some of the emissions from the PTT group's own emissions.

Significant new regulatory efforts

To address the regulatory vacuum for CCS projects, a number of South-East Asian jurisdictions have over the past year introduced legislation to provide a framework for the development of CCS projects. For example:

* In Indonesia, three new regulations on the implementation of CCS/CCUS in Indonesia were issued in 2023 and early 2024 to provide a framework for CCS projects and operations both for upstream oil and gas companies as well as other industrial sectors. Importantly, the new Indonesian regulatory regime clearly opens the door to cross-border transport and storage of CO2 with up to 30% of the storage being available for injection of CO2 from other countries.

Also, the new regime allows for the transfer of the supervision and responsibility for the reservoir from the operator to the state upon closure and after a certain observation period, which gives clarity to CCS project operators over their liability for sequestered CO2, which is a key consideration for investors in these projects.

* Malaysia's tax incentives for investments on CCS include an Investment Tax Allowance of 100% of capital expenditure for a period of 10 years, which can be set-off against up to 100% of business statutory income and Import Duty and Sales Tax on equipment used specifically for CCS technology as well as Sarawak's Land (Carbon Storage) Rules issued in 2022, which provide a high level framework for the development of CCS in Sarawakian waters.

Thanks to these initiatives, there has been a significant increase in new projects proposed in these jurisdictions.

Regional NOCs and international energy companies have been particularly active in this space. For example, in Malaysia, the Kasawari CCS project is being developed off the coast of Sarawak, with investments from Petronas Carigali, a subsidiary of Petronas, as well as the Lang Lebah project also off the coast of Sarawak, operated by Thailand's PTTEP with Petronas Carigali and Kufpec as partners. In Indonesia, Pertamina has entered into a number of memoranda of understanding and is conducting feasibility studies for several potential CCS projects with a range of foreign partners, including leading international oil companies. All in all, there are at least 15 CCS projects in Indonesia that are in the study and preparatory stages.

Apart from CCS-specific legislation, some regional economies have also started to implement carbon-related taxation, so as to incentivise the reduction of CO2, emissions. For example, in 2024 Singapore has imposed a carbon tax for heavy emitters of S$25 per tonne of CO2 emitted, which is meant to progressively increase to up to S$80 per tonne by 2030.

Is this enough

One of the major issues currently facing CCS projects is their financial viability. This can vary significantly depending on the specific features of each project, as evidenced by the Northern Lights and Moomba examples given above.

Fundamentally, a CCS project will be economically viable if the cost of the CCS value chain, including capturing, transportation and storage, is less than the cost of emitting the CO2.

Regulators have a key role to play in creating clear and long-term incentives to support the development of the CCS value chain.

These can be CCS-specific incentives, such as the Malaysian Investment Tax Allowance or the 45Q CCS-focused tax credits in the US, which have proven very attractive to investors, but also government funding for pilot projects and government supported business models, such as the UK CCS business model, which provides a combination of funding and revenue streams backed by the UK government to support early stage projects, with the intention of phasing out support over time.

Broader sector-agnostic regulations that aim to penalise and disincentivise businesses from emitting CO2 – such as the carbon tax in Singapore or cap and trade schemes implemented in the UK and the EU – and provide an overarching incentive to decarbonise can also provide the economic basis to support CCS projects. Whether they can do so will depend on their amount compared with the cost of CCS projects.

Estimates suggest that for point-source capture each tonne of carbon dioxide captured, transported and stored costs between US$80 to US$250. This compares with a S$25/tonne carbon tax in Singapore, or US$3/tonne in Japan and a persistently low carbon price under South Korea's emissions trading scheme. Therefore, the current carbon pricing in the regional developed markets alone is unlikely to be able to support CCS projects without additional government intervention.

What is very positive is that regulators are taking measures to increase financial incentives for decarbonisation and/or CCS projects specifically across the region. In Japan, a bill on CCS business as well as subsidies and funding from Japan’s Ministry of Economy, Trade and Industry was recently submitted to the Diet. In South-East Asia, Vietnam, the Philippines and Thailand are also exploring legislation to impose carbon pricing and Indonesia has introduced regulations for carbon pricing and trading in certain sectors over the past few years.

The Southeast Asian advantage

A number of South-East Asian countries have some structural advantages that are likely to make them particularly well placed to capture and capitalise opportunities that may arise from the increasing interest in CCS from businesses and governments from large emitting countries.

For example, a number of countries in South-East Asia have a well-developed upstream oil and gas industry, including established oil and gas working areas and upstream operations, mature local supply chains, and strong state-owned and independent oil companies that are very keen to find ways to decarbonise their activities.

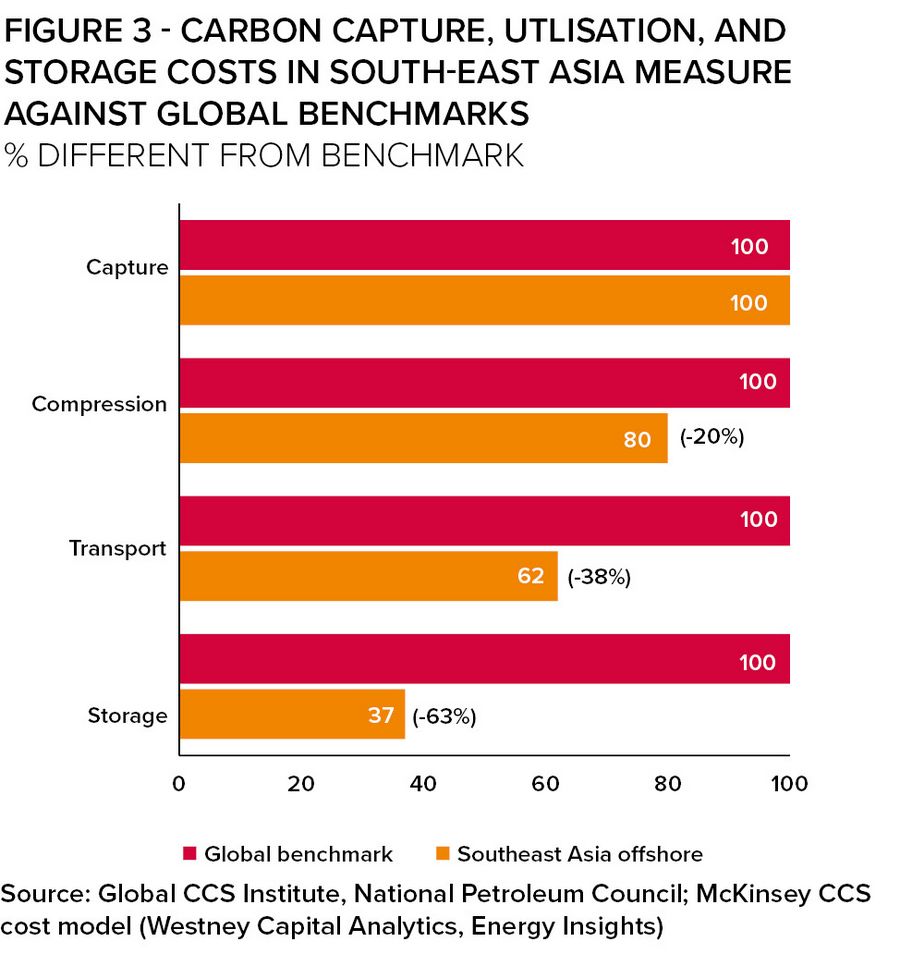

These characteristics and the general cost basis in South-East Asia generally drive down project costs compared with global benchmarks, as shown in Figure 2.

What is likely to work

Despite the industry and commercial utilisation being still in its infancy in South-East Asia, there are a number of structures and business models being considered by front-runner projects across the region.

These are generally a function of whether the CCS project will either: i) only be developed and operated by the emitter, eg used in support of existing oil and gas operations to mitigate emissions from oil and gas operations at or close to the depleted reservoir to be used for CCS – this is often referred to as the integrated model or; ii) if the CCS project will be providing CO2 storage as a service to a number of emitters, where the CCS project would generally charge a storage fee, which may be a tipping fee as used in waste management projects or a throughput fee as used in regasification/liquefaction terminals and certain power purchase agreements where the feedstock is supplied by the offtaker – the latter model being generally referred to as the midstream model.

Some projects can also be a hybrid of the upstream and midstream model where the depleted reservoir is used both for injection of the upstream operator's ongoing oil and gas operations (or those of other upstream oil and gas companies operating in the vicinity of the reservoir) as well as for injection of CO2 from other sources that can be other industrial emitters – such as thermal power generation, steel, cement and other emitting industrial facilities – in-country or also from other countries in the region.

It is generally agreed that the multiplicity of CO2 sources would improve the utilisation rate of the reservoir and enhance the financial viability of projects, unless the operator of the CCS project can contract out the entire storage capacity of the reservoir to a single emitter. This has also been the approach taken successfully in other geographies, such as the UK.

Of course, the other economic fundamentals for the CCS project, including their locational merits and regulatory support, and appropriate structuring of the contractual framework and risk allocation will also be critical to the success of these schemes.

Besides the various business models being contemplated by the industry for developing CCS projects, it is envisaged that most projects will involve partnerships either between the current holders of a participating interest in the oil and gas blocks that will be converted into CCS operations or between the relevant NOC and the existing operator of the block and possibly also other business entities that may be emitters and are looking for long term solutions to decarbonise.

Such partnerships can take the form of unincorporated joint ventures, which are common in the upstream oil and gas sector, or incorporated joint ventures depending on local regulatory requirements and the tax treatment of either structure for the respective sponsors.

Conclusion

Despite there being a number of remaining hurdles to large-scale commercial CCS developments in the current environment in South-East Asia, there is an increasing realisation that CCS will have to be part of the pathway to net-zero, together with governmental support for these.

This is particularly the case for countries and businesses across Asia that rely on CO2 intensive operations, which are hard to abate. For those, it is likely that CCS will be part of their decarbonisation journey.

For certain countries that have the benefit of longstanding upstream oil and gas operations that, in some cases are nearing their end of life, CCS may provide renewed opportunities to attract investment and revenues for the state by repurposing depleted reservoirs into world-class CCS operations.

It is expected that such CCS projects and nascent industry would have the potential of supporting not only the host countries' own international commitments, but possibly also that of export countries, thereby creating a nascent industry of regional strategic importance.

As shown in the countries that are widely seen as pioneers in the commercial development of CCS, such as the UK and the US, to be able to unlock the full potential of CCS, governments across Asia will also need to collaborate with industry stakeholders to reduce costs, implement government incentives and provide clear and stable regulatory frameworks to facilitate the development of CCS projects as well as the cross-border transportation and storage of CO2 across the region.

The development of multi-user CCS clusters in particular should help drive economic benefits to all stakeholders through shared transportation and storage infrastructure.

Footnote

1 – CO2 Storage Assessment in a Malaysian Depleted Carbonate Reservoir With 2-Way Fully Coupled Dynamic-Geomechanics Modeling for Safe Long-Term Storage, at the Offshore Technology Conference Asia, 2022.

To see the digital version of this report, please click here

To purchase printed copies or a PDF of this report, please email shahid.hamid@lseg.com in Asia Pacific & Middle East and leonie.welss@lseg.com for Europe & Americas.